|

|

|

|

|||||

|

|

|

Alibaba's BABA aggressive bet on quick commerce is emerging as one of its most ambitious initiatives. In the first quarter of fiscal 2026, the segment delivered 12% year-over-year revenue growth, fueled by the success of Taobao Instant Commerce, which is rapidly reshaping the company’s e-commerce ecosystem. The platform has boosted user engagement, with average daily orders surpassing 80 million and monthly active consumers nearing 300 million, helping lift Taobao’s MAUs by 25%. These gains highlight Alibaba’s success in capturing demand within China’s fast-growing instant retail market.

This expansion, however, has strained profitability. Adjusted EBITDA declined 14% year over year, while free cash flow turned negative, reflecting the heavy capital demands of scaling instant delivery, fulfillment networks and merchant subsidies amid price wars with Meituan and JD.com.

Looking ahead, Alibaba views this spending as a strategic land grab designed to secure early market dominance. By integrating Ele.me’s on-demand delivery network and leveraging its vast supply chain, the company aims to build operational density that can reduce per-order logistics costs over time. With China’s high population density and strong consumer appetite for convenience, Alibaba is well-positioned to transform quick commerce into a profitable, high-frequency consumption model integrated across its platforms.

A 30 trillion RMB addressable market and the consensus estimate of 5% revenue growth in fiscal 2026 and 12% in fiscal 2027 support a strategic path toward long-term profitability and retail dominance.

JD.com JD is Alibaba’s closest rival in China’s instant retail race. JD.com is rapidly scaling its JD NOW service, partnering with local stores to deliver goods in as little as nine minutes. Leveraging its tightly controlled supply chain and advanced logistics network, JD.com ensures faster, more reliable fulfillment than competitors. However, its heavy investment in instant delivery and subsidies to match Alibaba’s spending spree could pressure margins, intensifying the competition for dominance in China’s quick commerce market.

PDD Holdings PDD is emerging as a formidable challenger to Alibaba through its ultra-low-cost, asset-light model. PDD Holdings leverages Pinduoduo and Temu to drive massive user engagement and rapid scalability without heavy logistics investment. By prioritizing affordability, social commerce and efficiency, PDD Holdings challenges Alibaba’s capital-heavy model, giving it a strategic edge in global quick commerce and positioning it as a powerful rival in value-driven e-commerce markets.

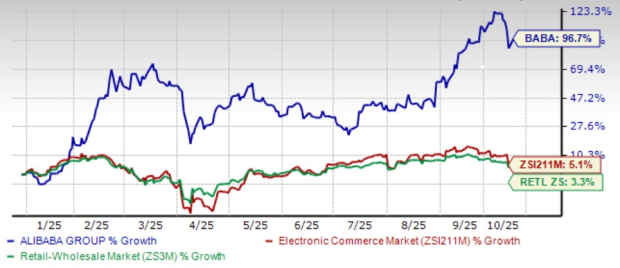

BABA shares have surged 96.7% in the year-to-date period, outperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 5.1% and 3.3%, respectively.

From a valuation standpoint, BABA stock is currently trading at a forward 12-month Price/Earnings ratio of 18.11X compared with the industry’s 23.14X. BABA has a Value Score of C.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.97 per share, down 9.7% over the past 30 days, implying a 22.64% year-over-year decline.

Alibaba currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite