|

|

|

|

|||||

|

|

|

Under Armour, Inc. UAA reported first-quarter fiscal 2026 results, marked by persistent regional weakness amid a challenging macroeconomic and trade environment. North America, the company’s largest revenue contributor, declined 5.5% year over year, led by lower wholesale orders, softer retail traffic and weaker e-commerce performance.

Management anticipates this pressure to intensify in the second quarter, forecasting a low double-digit decline as challenges in the spring/summer 2025 order book persist. Despite near-term softness, initiatives to rebuild brand strength and enforce pricing discipline remain a priority.

Internationally, total revenues fell 1.4% year over year, or 2% on a currency-neutral basis, to $466.6 million. Performance varied across regions, with growth in EMEA offset by declines in the Asia-Pacific (APAC) and Latin America. EMEA sustained steady growth, with revenue rising 9.6%, driven by stronger execution and targeted, localized brand storytelling. In contrast, APAC and Latin America’s underperformance highlights the volatility within Under Armour’s international portfolio.

In APAC, revenues fell 10% on both reported and currency-neutral bases, reflecting weaker consumer confidence and heightened promotional activity. A highly competitive retail environment eroded pricing power and limited full-price sell-through, pressuring margins. Under Armour’s strategy in the region now emphasizes rebuilding premium positioning through tighter distribution, disciplined pricing, and stronger local partnerships. Fiscal 2026 is expected to be a stabilizing year focused on restoring sustainable growth momentum.

In Latin America, revenues fell 15.3%, partly driven by foreign currency headwinds. On a currency-neutral basis, revenues declined 8% for the quarter, as decreases in full-price wholesale and direct-to-consumer sales were partially offset by growth in the distributor channel. Broader economic uncertainty continues to limit consumer spending and brand visibility across key markets.

Collectively, these regional challenges emphasize execution risks in Under Armour’s diversification strategy. North America faces tariff-related cost pressures, while APAC and Latin America battle weak demand and pricing headwinds. Only EMEA has shown steady momentum, supporting overall brand stability. As management guides for a 6-7% revenue decline in the second quarter, focus remains on strengthening regional operations and improving long-term revenue quality.

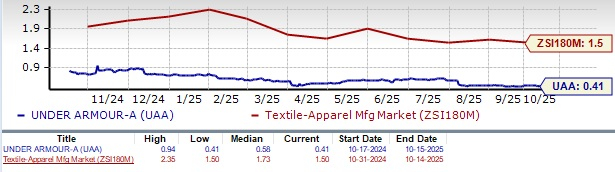

Shares of the company have lost 29.8% in the past three months compared with the industry’s 5.5% decline.

From a valuation standpoint, Under Armour is trading at a forward 12-month price-to-sales ratio of 0.41X, down from the industry average of 1.50X. UAA has a Value Score of B.

The Zacks Consensus Estimate for Under Armour’s fiscal 2026 earnings implies a year-over-year decline of 83.9%, whereas the same for fiscal 2027 indicates an uptick of 310.9%. Estimates for fiscal 2026 and 2027 have been southbound by 3 cents and 1 cent, respectively, in the past 30 days.

Under Armour currently has a Zacks Rank #4 (Sell).

Some better-ranked stocks are Genesco Inc. GCO, Urban Outfitters Inc. URBN and Tilly's, Inc. TLYS.

Genesco is a Nashville-based specialty retail and branded company that sells footwear and accessories in retail stores. It currently flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for GCO’s fiscal 2026 earnings and sales implies growth of 71.3% and 3.7%, respectively, from the year-ago actuals. Genesco delivered a trailing four-quarter average earnings surprise of 28.1%.

Urban Outfitters is a lifestyle specialty retailer that offers fashion apparel and accessories, footwear, home decor and gift items. It sports a Zacks Rank #1 at present.

The Zacks Consensus Estimate for Urban Outfitters’ current fiscal-year earnings and sales indicates growth of 29.1% and 9.7%, respectively, from the year-ago actuals. URBN delivered a trailing four-quarter average earnings surprise of 24.8%.

Tilly's is a specialty retailer in the action sports industry, selling clothing, shoes and accessories. It has a Zacks Rank of 2 (Buy) at present.

The Zacks Consensus Estimate for Tilly's current fiscal-year earnings indicates growth of 8.8% from the year-ago actual. TLYS delivered a trailing four-quarter average earnings surprise of 60.7%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| 7 hours | |

| 8 hours | |

| Jul-29 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-21 | |

| Jul-21 | |

| Jul-17 | |

| Jul-16 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite