|

|

|

|

|||||

|

|

|

This AI infrastructure stock has receded from all-time highs it achieved a few months ago.

However, this company will likely grow at a faster pace thanks to the recent contracts that it landed.

Though it is expensive right now, this stock can justify its valuation by sustaining outstanding growth levels over the long run.

Artificial intelligence (AI) stocks have played a central role in the broader market's rally in the past three years. That's not surprising, given that the rapidly growing adoption of this technology led to a sharp increase in the revenue and earnings for several companies.

Nvidia (NASDAQ: NVDA) is one of the biggest winners of this AI boom. Its share prices shot up 1,400% during this period, far outpacing the 81% gains clocked by the S&P 500 index. But this rapid rise in the past three years has made Nvidia stock tremendously expensive.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

It is now trading at 28 times sales, a significant premium to the Nasdaq Composite index's average sales multiple of 5.2. Given that Nvidia's terrific growth is likely to taper off in the next couple of years, it may not be a good idea to buy this AI stock right now, given its expensive valuation.

However, there's another solid alternative to Nvidia in the AI infrastructure market. This stock went public earlier this year, and it has receded nearly 27% from the highs it hit on June 20. Let's take a closer look at this name and see why this AI stock is a screaming buy right now.

Image source: Getty Images.

Nvidia's graphics processing units (GPUs) provide the building blocks of the AI revolution. The massive parallel computing power that its GPUs provide is key to the training of large language models (LLMs) such as OpenAI's ChatGPT. However, these chips need to be deployed in large clusters in data centers. This is where a company such as CoreWeave (NASDAQ: CRWV) steps in.

CoreWeave is a neocloud company that specializes in offering AI-focused data centers. The company has 33 data centers powered by Nvidia's GPUs in the U.S. and Europe. It rents out its data center capacity to customers who want to train and deploy AI models. The GPU-as-a-service business model that CoreWeave operates has been a massive success. It gives customers the ability to run AI workloads without having to buy expensive hardware and also helps save on costs associated with managing that infrastructure.

The demand for CoreWeave's AI data centers is so strong that it gets more business than it can fulfill. The company generated $1.2 billion worth of revenue in the second quarter of 2025, an increase of 207% from the year-ago period. However, it added nearly $14 billion to its revenue backlog as compared to the year-ago period.

CoreWeave's backlog doubled in the first six months of 2025. That's not surprising, as companies need to get their hands on whatever AI cloud computing capacity is available. Importantly, there are no signs of a slowdown in the growth of CoreWeave's backlog. The company recently landed multibillion-dollar contracts with OpenAI, Meta Platforms, and Nvidia.

Meta gave CoreWeave a $14.2 billion five-year contract, while OpenAI signed a contract expansion worth $6.5 billion. OpenAI signed $22.4 billion worth of contracts with CoreWeave this year. Meanwhile, Nvidia struck a $6.3 billion deal with CoreWeave, which allows Nvidia to purchase any remaining AI computing capacity through 2032.

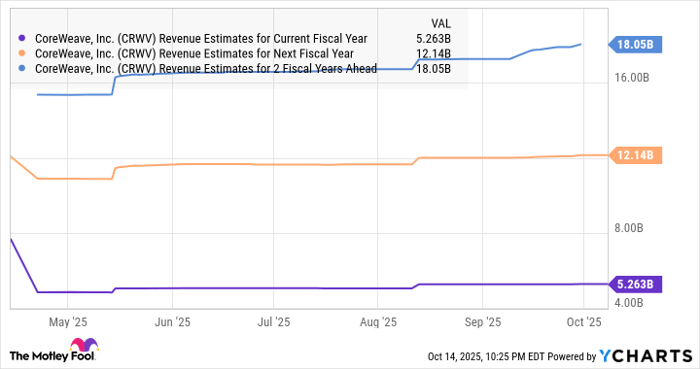

These new deals suggest that its revenue backlog could now top the $50 billion mark. That's pretty sizable for a company that has just over $3.5 billion in trailing-12-month revenue. CoreWeave will be able to convert all that backlog into revenue once it starts building up more capacity.

The good part is that CoreWeave is working on bringing more data center capacity online. The company had 470 megawatts (MW) of active data center power capacity at the end of Q2. However, its contracted power capacity, which refers to the amount of capacity it has already secured for future data center deployments, stands at an impressive 2.2 gigawatts (GW).

So, don't be surprised to see CoreWeave turn its massive backlog into revenue as it brings more data center capacity online. More importantly, the anticipated shortage in AI data center capacity should ensure that whatever capacity expansion CoreWeave plans should be adopted quickly by customers.

As a result, it won't be surprising to see CoreWeave's growth outpacing consensus expectations going forward.

Data by YCharts.

In fact, CoreWeave's backlog is larger than the combined revenue that analysts expect from the company in the current and the next couple of fiscal years. So, there is a solid chance that it will be able to do better than consensus expectations, and that could pave the way for healthy long-term upside in the stock.

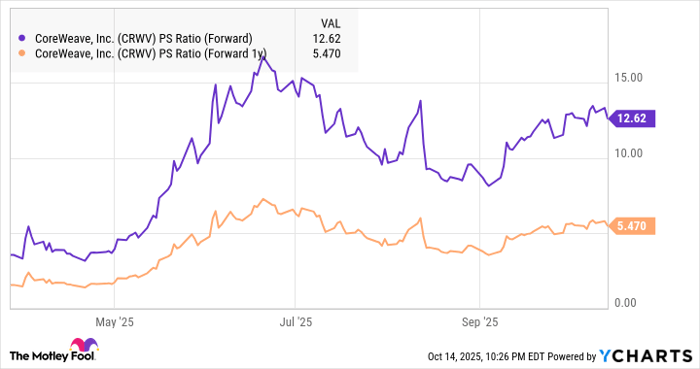

CoreWeave has a price-to-sales ratio of 19. While that's on the expensive side, investors should note that the stock is significantly cheaper than Nvidia. What's more, CoreWeave is growing at a faster pace than Nvidia, and it has the potential to sustain elevated levels of growth for a long time to come thanks to its huge backlog, capacity expansion, and the robust demand for AI computing capacity.

Not surprisingly, CoreWeave's forward sales multiples are much lower.

Data by YCharts.

So, investors looking to buy a top growth stock that's capitalizing on the booming demand for AI infrastructure can consider taking advantage of the dip in CoreWeave stock as it seems on track to deliver big gains in the next five years.

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $648,924!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,102,333!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 190% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 13, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and Nvidia. The Motley Fool has a disclosure policy.

| 15 min | |

| 16 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite