|

|

|

|

|||||

|

|

|

Vertiv VRT is set to report its third-quarter 2025 results on Oct. 22.

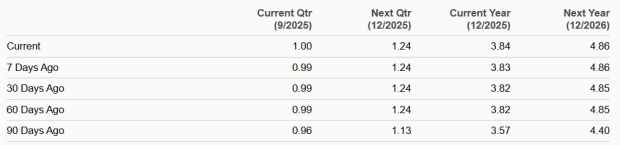

For the third quarter of 2025, revenues are expected to be between $2.51 billion and $2.59 billion. Organic net sales are expected to increase in the 20% to 24% range. VRT expects third-quarter 2025 non-GAAP earnings between 94 cents per share and $1 per share.

The Zacks Consensus Estimate for third-quarter 2025 revenues is pegged at $2.58 billion, indicating year-over-year growth of 24.6%. The consensus mark for earnings is pegged at $1 per share, which has increased by a penny over the past 30 days, indicating 31.6% year-over-year growth.

Vertiv’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, delivering an earnings surprise of 10.65%, on average.

Vertiv Holdings Co. price-consensus-chart | Vertiv Holdings Co. Quote

Let’s see how things have shaped up prior to this announcement.

Vertiv’s third-quarter 2025 results are expected to have benefited from an extensive product portfolio, which spans thermal systems, liquid cooling, UPS, switchgear, busbar and modular solutions. Vertiv predominantly serves data center providers and has been capitalizing on robust AI-driven order growth. The growing focus on thermal management by data center operators aligns well with Vertiv’s strengths, and the company is expected to meet the increasing demand with advanced, efficient solutions in the to-be-reported quarter.

VRT’s expanding portfolio has been a major positive. In June, Vertiv announced its energy-efficient 142KW cooling and power reference architecture for the NVIDIA NVDA GB300 NVL72 platform. Vertiv solutions are available as SimReady 3D assets in the NVIDIA Omniverse Blueprint for AI factory design and operations.

Moreover, acquisitions have played an important role in expanding Vertiv’s footprint. In August, Vertiv acquired Waylay NV, a Belgium-based company known for its hyperautomation and generative AI software. This move aims to improve its AI-driven monitoring and control technologies for power and cooling systems. VRT also completed its $200 million acquisition of Great Lakes Data Racks & Cabinets, broadening its rack, cabinet and integrated infrastructure offerings for critical digital infrastructure. These acquisitions are expected to have driven Vertiv’s top-line growth in the to-be-reported quarter.

However, execution challenges and tariff-related transition costs related supply chain and manufacturing are expected to have hurt third-quarter 2025 results.

Vertiv shares have gained 53.2% year to date (YTD), outperforming the Zacks Computer & Technology sector’s growth of 23.1% and the Zacks Computer IT Services industry’s decline of 16.4%. Vertiv shares have outperformed its closest peers, including Schneider Electric SBGSY and Eaton ETN. Over the same time frame, shares of Schneider Electric and Eaton have returned 16.3% and 12.5%, respectively.

Technically, Vertiv shares are displaying a bullish trend as they trade above the 50-day and 200-day moving averages.

Vertiv stock is not so cheap, as the Value Score of D suggests a stretched valuation at this moment. In terms of the 12-month price/book ratio, VRT is trading at 21.26, higher than the sector’s 11.29, Schneider Electric’s 4.92 and Eaton’s 7.79.

Vertiv’s expanding portfolio has been a major growth driver for its success. In August, Vertiv announced the global launch of Vertiv OneCore. This is a scalable, prefabricated data center solution that combines power, thermal and IT infrastructure into one factory-assembled system. OneCore is designed to speed up high-density deployments. It simplifies installation, reduces on-site complexity, and supports flexible, energy-efficient setups for AI and enterprise applications.

VRT’s rich partner base, which includes the likes of Ballard Power Systems, Compass Datacenters, NVIDIA, Oklo, Intel and ZincFive, has been a key catalyst.

However, the company is suffering from sluggishness in Europe, Middle East & Africa (EMEA). 2025 EMEA sales is expected to be flat compared with 2024. Rising expenses related to engineering and R&D, capacity and go-to-market initiatives is a concern.

Although VRT is experiencing rapid growth in the liquid cooling market, a critical area for AI and high-density computing, it is also facing fierce competition in this domain. Concerns over tariff headwinds, and stretched valuation are headwinds that make VRT stock a risky bet.

VRT currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable entry point to accumulate the stock.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 min | |

| 7 min |

NVent Electric's Growth Story Heats Up On Liquid Cooling, Data Center Transformation

NVDA

Investor's Business Daily

|

| 29 min | |

| 30 min | |

| 38 min | |

| 39 min | |

| 57 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite