|

|

|

|

|||||

|

|

|

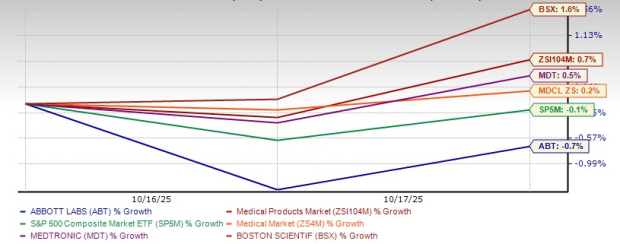

Shares of Abbott ABT have edged up 0.7% since the company’s third-quarter 2025 earnings release on Oct. 15, 2025. The company reported a strong year-over-year increase in adjusted earnings and revenues. Earnings came in line with the Zacks Consensus Estimate, while revenues missed the same. Global Core Laboratory Diagnostics sales were impacted by challenging market conditions in China, including the impact of volume-based procurement programs. External pressure, particularly the ongoing tariff war, has dampened investors' enthusiasm and capped further market gains.

Let’s delve deeper.

Since its earnings release, shares of Abbott have underperformed the industry and the sector’s gain of 0.7% and 0.2%, respectively. The S&P 500 index, which dipped 0.1% during the period, also stayed ahead of ABT stock. The company’s archrivals like Boston Scientific BSX and Medtronic MDT registered share price improvements of 1.6% and 0.5%, respectively, during the said period.

Abbott’s third-quarter 2025 results showed broad-based growth across most segments. Established Pharmaceuticals rose 7.5% (up 7.1% organically) with emerging markets up 11.1%. Medical Devices grew 14.8% (up 12.5% organically), led by Diabetes Care (up 16.2%), Structural Heart (up 11.3%), Heart Failure (up 12.1%) and strong Electrophysiology, Rhythm Management, and Neuromodulation sales. Nutrition sales increased 4.2% (up 4% organically), driven by Ensure and Glucerna.

Diagnostics declined 6.6% (down 7.8% organically) though ex-COVID organic sales were flat. Core and Molecular Diagnostics saw modest growth, while Rapid Diagnostics fell 27.7%, partially offset by Point of Care ( up 7.8%).

Abbott Laboratories' growth trajectory in 2025 faces challenges due to escalating tariffs, particularly from U.S. trade policies. In the third quarter, gross profit rose 6% year over year. However, gross margin contracted 46 basis points (bps) to 55.4% due to tariff impacts. These tariffs are particularly consequential given that Abbott’s product portfolio, ranging from infant nutrition to advanced medical devices, relies heavily on global production and distribution networks.

Meanwhile, selling, general and administration expenses rose 5.4% year over year. Research and development expenses rose 7.4% year over year. The company reported adjusted operating profit growth of 6.4% year over year. The adjusted operating margin contracted 11 bps to 21.8%.

While the trade policy environment introduces complexity, Abbott’s management remains confident about the company’s ability to weather the storm. The company is leveraging its diversified portfolio, strong brand recognition and robust pipeline of new products, including nearly $0.5 billion in sales from recent launches, to sustain growth despite tariff pressure.

Investments in U.S. manufacturing and R&D facilities aim to strengthen supply chain resilience, while broad-based demand across Medical Devices, Nutrition and Established Pharmaceuticals provides a buffer against geopolitical and market uncertainties. Management continues to guide high single-digit organic sales growth and double-digit EPS growth, reflecting disciplined execution and innovation-driven resilience.

For the full year, Abbott expects adjusted diluted EPS to be in the range of $5.12 -$5.18 (earlier $5.10-$5.20). Full-year organic sales growth, excluding COVID-19 testing-related sales, is expected to be in the range of 7.5-8.0% (same as earlier). When including COVID-19 testing-related sales, organic sales growth is forecasted to be 6-7% (unchanged).

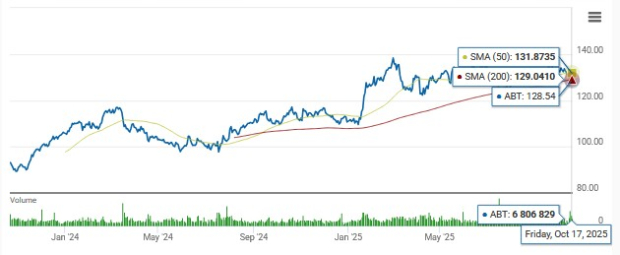

Abbott is currently trading below its 50-day and 200-day simple moving averages (SMA), indicating short-term bearishness, while long-term trends remain under pressure amid ongoing macroeconomic complexities.

From a valuation standpoint, Abbott’s forward 12-month price-to-earnings (P/E) is 23.10X, a premium to the industry average of 20.75X.

The company is also trading at a significant premium to industry players like Medtronic, with its current P/E being 16.46. However, Boston Scientific, with a current P/E of 30.02X, appears more stretched.

Despite its adaptive strategies, Abbott's stock price does not reflect the company’s underlying strength. The subdued market reaction to its third-quarter earnings and revenue growth suggests that investors remain cautious amid geopolitical uncertainty, mainly in the form of retaliating tariffs.

The current stretched valuation suggests that investors may be paying a higher price relative to the company's expected earnings growth. While the impressive top-line performance in the third quarter boosted investor sentiment, barring Diagnostics, this might not be the ideal time to invest in Abbott. The short-term hiccups in the form of international trade challenges are limiting the stock’s near-term gains.

Accordingly, while current shareholders should hold their positions, new investors should wait for a better entry point.

Abbott currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Abbott Bounds Higher After Hiking 2026 Profit View On Second-Quarter Beat

ABT +10.71%

Investor's Business Daily

|

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite