|

|

|

|

|||||

|

|

|

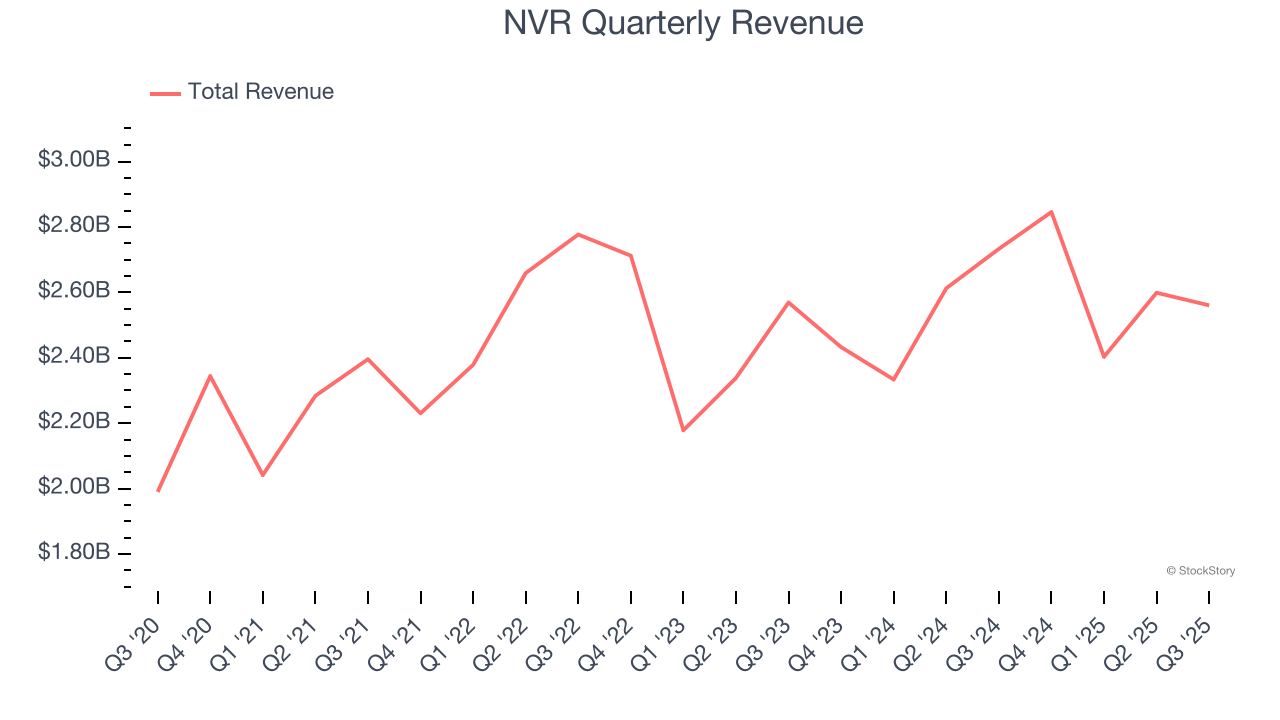

Homebuilder NVR (NYSE:NVR) met Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 6.3% year on year to $2.56 billion. Its GAAP profit of $112.33 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy NVR? Find out by accessing our full research report, it’s free for active Edge members.

Known for its unique land acquisition strategy, NVR (NYSE:NVR) is a respected homebuilder and mortgage company in the United States.

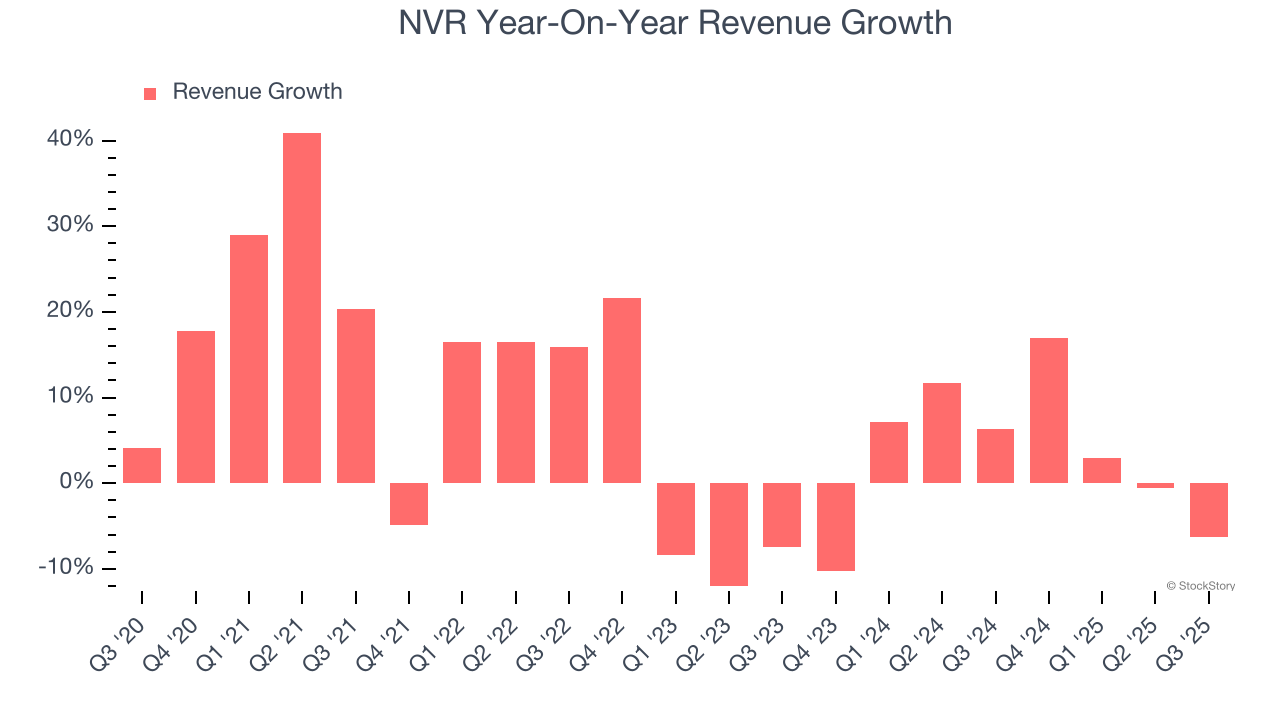

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, NVR’s sales grew at a decent 7.7% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. NVR’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend.

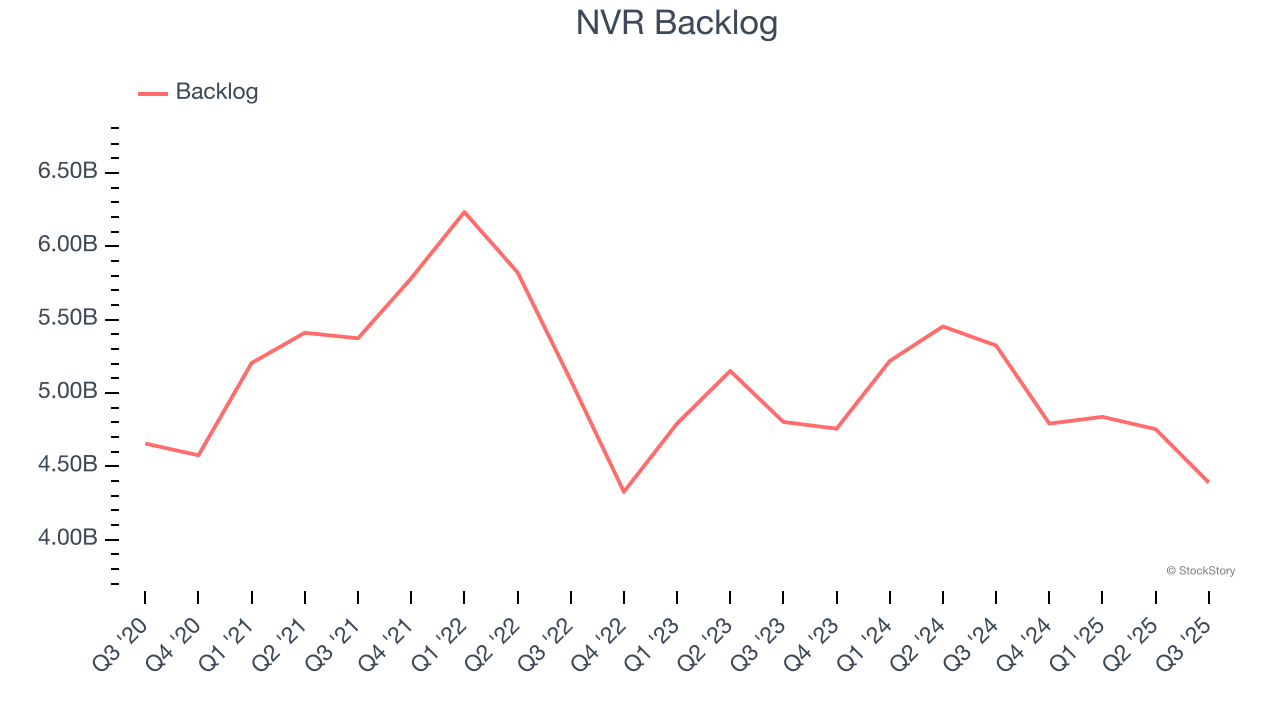

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. NVR’s backlog reached $4.39 billion in the latest quarter and was flat over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, NVR reported a rather uninspiring 6.3% year-on-year revenue decline to $2.56 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 5.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

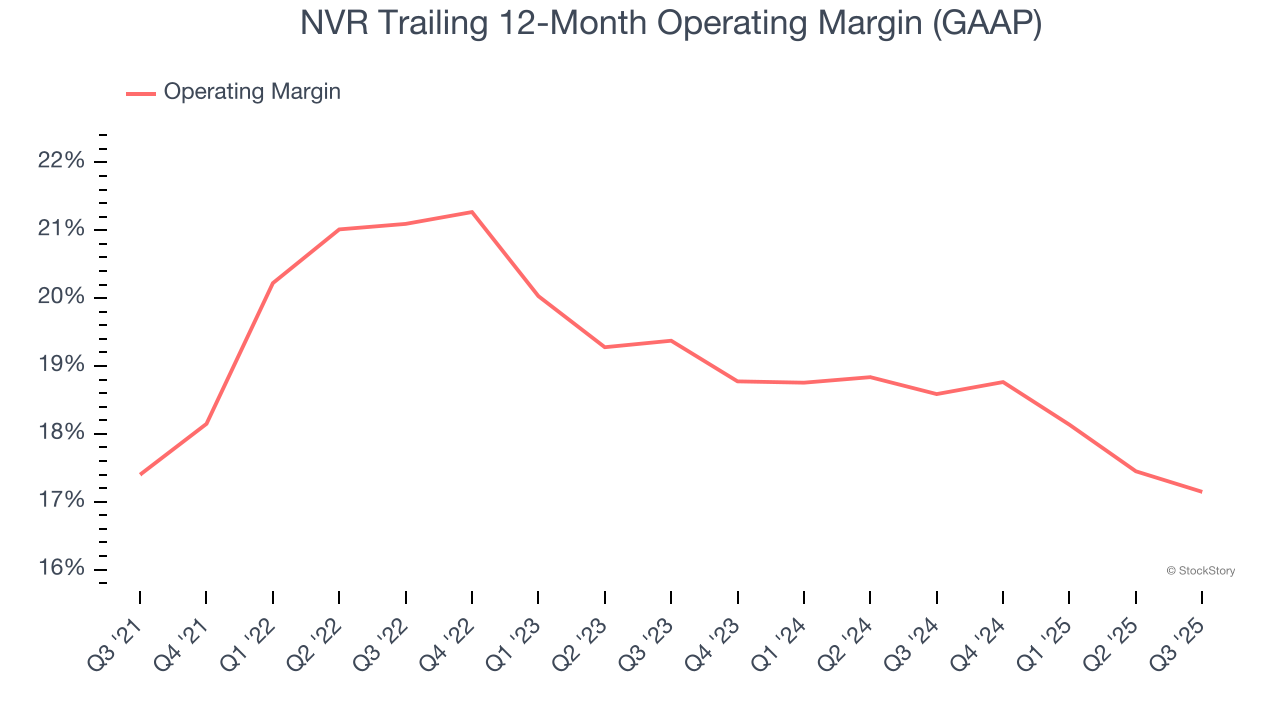

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

NVR’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 18.7% over the last five years. This profitability was elite for an industrials business thanks to its efficient cost structure and economies of scale. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, NVR’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but we’re still happy with NVR’s performance considering most Home Builders companies saw their margins plummet.

In Q3, NVR generated an operating margin profit margin of 17.3%, down 1.2 percentage points year on year. Since NVR’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

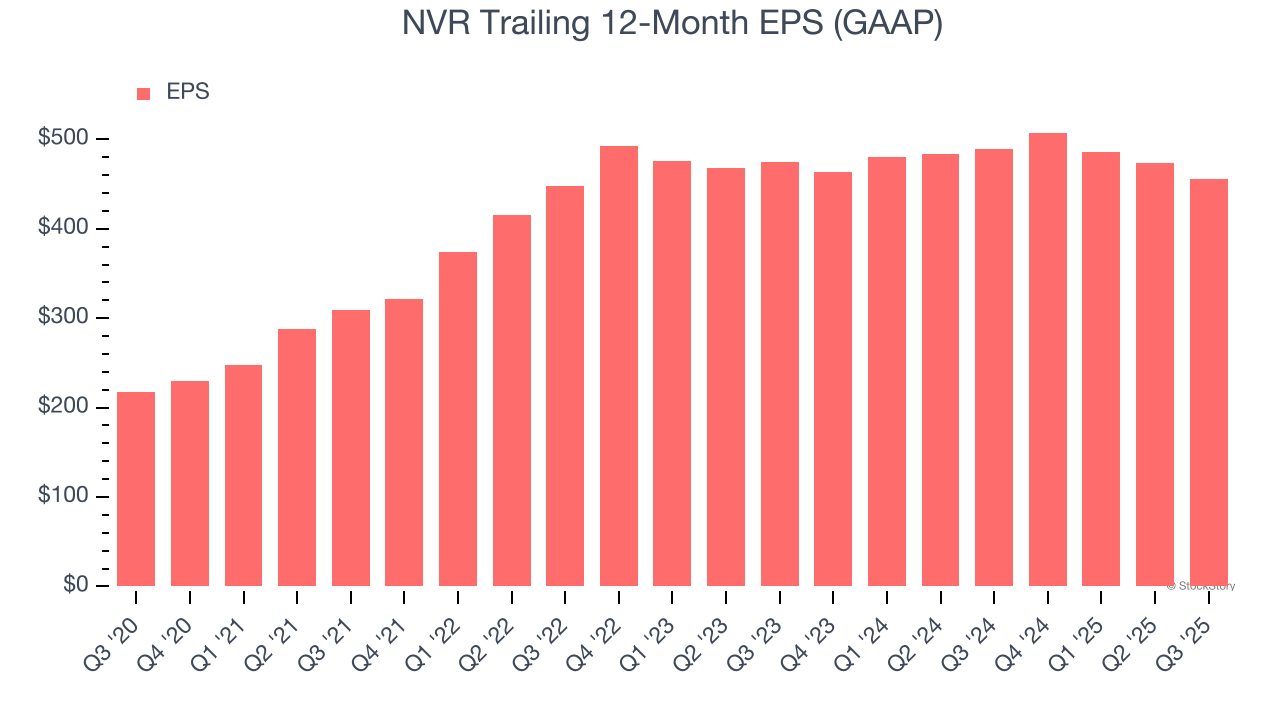

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

NVR’s EPS grew at a spectacular 16% compounded annual growth rate over the last five years, higher than its 7.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

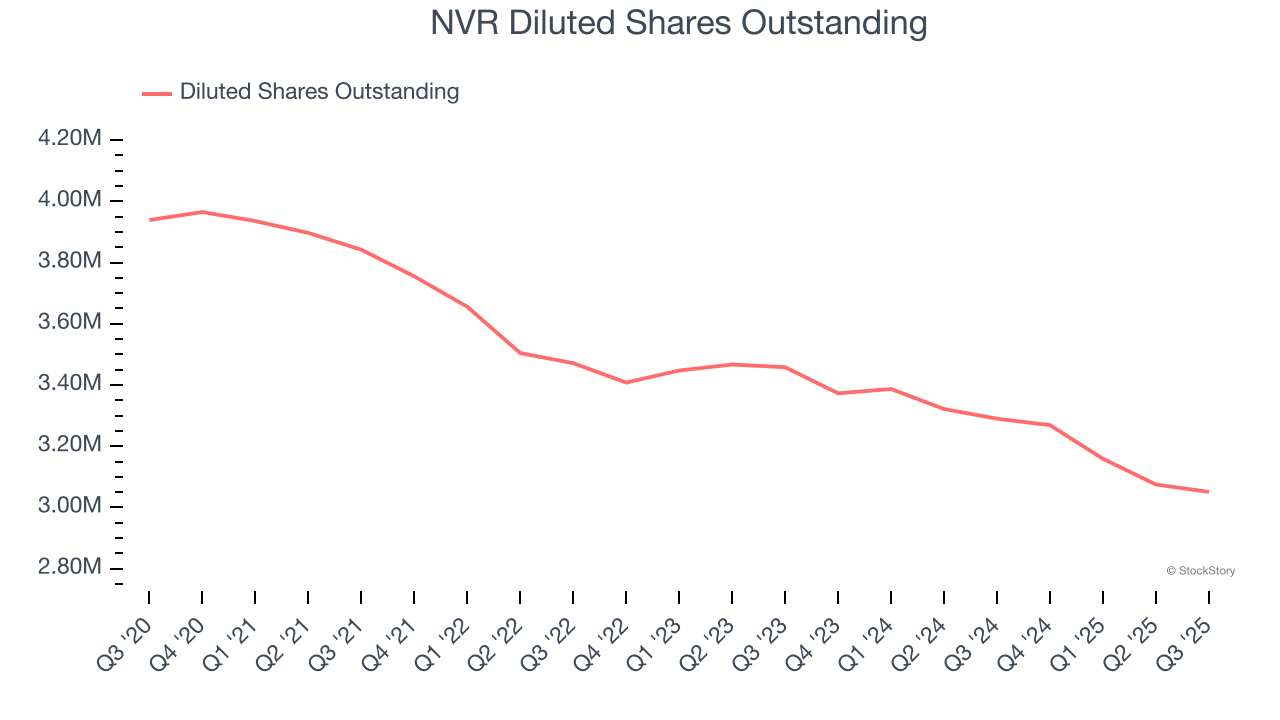

Diving into the nuances of NVR’s earnings can give us a better understanding of its performance. A five-year view shows that NVR has repurchased its stock, shrinking its share count by 22.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For NVR, its two-year annual EPS declines of 2.1% mark a reversal from its (seemingly) healthy five-year trend. We hope NVR can return to earnings growth in the future.

In Q3, NVR reported EPS of $112.33, down from $130.49 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects NVR’s full-year EPS of $455.63 to shrink by 1.2%.

It was good to see NVR beat analysts’ EPS expectations this quarter. On the other hand, its backlog slightly missed and its revenue was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.3% to $7,700 immediately following the results.

NVR’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-23 | |

| Jul-23 | |

| Jun-01 | |

| May-08 | |

| Apr-22 | |

| Apr-15 | |

| Apr-07 | |

| Apr-06 | |

| Apr-03 | |

| Mar-17 | |

| Mar-13 | |

| Mar-05 | |

| Feb-27 | |

| Feb-23 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite