|

|

|

|

|||||

|

|

|

Despite record deliveries, profits fell sharply.

Tesla continues to lose market share.

The valuation is inflated by future promises.

Coming into Tesla's (NASDAQ: TSLA) third-quarter earnings report, the leading producer of electric vehicles (EVs) reported a record number of deliveries. With the help of the pull-forward effect from the expiring EV tax credit, unit sales rose in Q3 to 497,099, up 7% from the quarter a year ago and increased 29% from Q3.

However, investors had to wait until Wednesday to get a full snapshot of Tesla's financial performance, and they were generally underwhelmed.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

The stock edged down in after-hours trading, but considering its monster gains over the last year, the modest sell-off of just 3.1% isn't a bad outcome for investors.

Overall revenue rose 12% to $28.1 billion, which beat the consensus at $26.7 billion. Automotive revenue rose 6% to $21.2 billion, while energy generation and services delivered stronger growth.

However, profitability continued to suffer, a sign that vehicle prices are being pressured as costs are going up. Despite the 12% increase in revenue, gross profit rose just 1% to $5.1 billion, meaning gross margin fell from 19.8% to 18%.

Operating income fell 40% to $1.6 billion, which included a $238 million restructuring charge. Adjusted earnings per share (EPS) fell from $0.72 to $0.50, which missed estimates at $0.56.

A Tesla Model 3. Image source: Tesla.

CEO Elon Musk has been a master at redirecting investor attention, which is why the stock has been able to soar and achieve a price-to-earnings (P/E) ratio over 200 even when revenue is growing just 12% and earnings are falling sharply.

Musk has spent the last few years touting the company's transition to autonomy, including self-driving vehicles and its Optimus robot. In June, it launched Robotaxi service in Austin, Texas in a small pilot program, and it then expanded it to the San Francisco Bay Area in Q3. The program still has human drivers in order to be safe, though Musk wants to get rid of them.

Looking ahead to 2026, Tesla said the fully autonomous Cybercab was on schedule for volume production in 2026, along with the Tesla Semi and Megapack 3 for energy storage. It also said first-generation production lines for Optimus robots are being installed. And management continues to tout the potential of AI across its product portfolio.

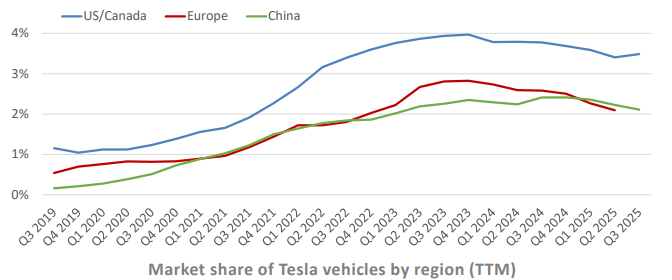

Despite Musk's continuing to talk up Tesla's future, the current picture, especially in its core EV segment, is not good. As you can see from the chart, its EV market share has been on a general decline for the last two years.

Data source: Tesla; TTM = trailing 12 months.

That chart shows its market share of all vehicle sales, and the uptick in the U.S. is likely due to the approaching end of the $7,500 EV credit, which gave its sales a one-time bump in Q3. It wouldn't be surprising to see the decline resume in Q4.

The company has lost nearly a percentage point of market share in Europe over the last two years, and intense competition in China seems to be eating away at its market share, which has also declined in recent quarters.

Looking at this next chart, you can see that Tesla's EV sales also appear to have peaked. Even as it just reported its best quarter of deliveries, it peaked in 2023 on a trailing-12-month basis.

Data source: Tesla.

As you can see, vehicle sales have plateaued over the last two years and even declined in recent quarters.

Whatever technological breakthrough might be around the corner for the company, it seems unlikely to turn around the general slide in vehicle sales, especially now that the tax credit is gone. And rising auto loan delinquencies could spell trouble for vehicle sales across the broader EV market.

Tesla's valuation has defied reality for several quarters, but sustained weakness in the EV business should eventually catch up with the stock. Next year will be a big test for the company, considering the product lineup it has set for release, including the Cybercab. But the automaker needs some kind of breakthrough to justify its current valuation.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 20, 2025

Jeremy Bowman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours |

Stock Market Today: Dow, Nasdaq Eke Out Gains; Gold, Silver Names Slide (Live Coverage)

TSLA

Investor's Business Daily

|

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours |

Stock Market Today: Nasdaq, Dow Climb; Airline Name Flies Higher (Live Coverage)

TSLA

Investor's Business Daily

|

| 5 hours |

No Need For Range Anxiety. This Option On Tesla Stock Uses Range As Advantage.

TSLA

Investor's Business Daily

|

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours |

Stock Market Today: Dow Weakens As Nasdaq Lags; Biotech Name Hits Record (Live Coverage)

TSLA

Investor's Business Daily

|

| 7 hours | |

| 7 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite