|

|

|

|

|||||

|

|

|

Johnson & Johnson JNJ and Merck MRK are leading U.S. healthcare giants, making them natural peers for a head-to-head comparison.

Both companies have a strong presence in oncology, immunology and neuroscience areas. Other than that, J&J also has drugs for cardiovascular and metabolic diseases, pulmonary hypertension and infectious diseases, along with a strong presence in the medical devices segment.

On the other hand, Merck boasts a strong presence in vaccines, virology and hospital acute care.

Both firms face looming patent expirations and headwinds from Medicare Part D redesign. But which one is a better investment option today? Let’s take a closer look at their fundamentals, growth prospects and challenges to make an informed choice.

J&J’s biggest strength is its diversified business model, as it has not just pharmaceuticals, but also medical devices, which helps it to withstand economic cycles more effectively. It operates through more than 275 subsidiaries.

J&J’s Innovative Medicine unit is showing a growth trend. The segment’s sales rose 3.4% in the first nine months of 2025 on an organic basis despite the loss of exclusivity (“LOE”) of its multi-billion-dollar product, Stelara, and the negative impact of the Part D redesign. The third quarter was the segment’s second consecutive quarter of sales of more than $15 billion despite Stelara’s LOE. Growth is being driven by J&J’s key drugs like Darzalex, Erleada and Tremfya. New drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato also contributed significantly to growth.

J&J’s MedTech business has improved in the past two quarters, driven by the acquired cardiovascular businesses, Abiomed and Shockwave, as well as Surgical Vision and wound closure in Surgery. Improvements in J&J’s electrophysiology business also drove the growth.

Along with its third-quarter earnings release, J&J announced its intention to separate its Orthopaedics franchise in the MedTech segment into a standalone orthopedics-focused company, called DePuy Synthes.

The decision aligns with J&J’s efforts to shift its MedTech portfolio to high-innovation, high-growth markets like cardiovascular and robotic surgery. J&J expects that the separation will improve its MedTech unit’s growth and margins, as the Orthopaedics franchise has been a slow-growth business for J&J.

In 2026, J&J expects accelerated growth in both the Innovative Medicine and MedTech segments.

J&J has rapidly advanced its pipeline this year, attaining significant clinical and regulatory milestones that will help drive growth through the back half of the decade. This year, it gained approval for new products like Inlexzoh/TAR-200, a first-of-its-kind drug-releasing system, for treating high-risk non-muscle invasive bladder cancer and Imaavy (nipocalimab) for treating generalized myasthenia gravis. J&J believes that nipocalimab has a pipeline-in-a-product potential. Regulatory applications were recently filed for another key candidate, icotrokinra, for moderate-to-severe plaque psoriasis. J&J believes that icotrokinra has the potential to revolutionize the treatment of plaque psoriasis with a once-a-day pill.

J&J believes 10 of its new products/pipeline candidates in the Innovative Medicine segment have the potential to deliver peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, newly acquired Caplyta, Inlexzo, Rybrevant, plus Lazcluze and icotrokinra.

However, the Stelara patent cliff, the impact of Part D redesign and slowing sales in China in the MedTech segment and the pending talc lawsuits are significant headwinds.

Merck boasts more than six blockbuster drugs in its portfolio, with Keytruda being the key top-line driver. Keytruda has played an instrumental role in driving Merck’s steady revenue growth in the past few years. Keytruda’s sales are gaining from rapid uptake across earlier-stage indications, mainly early-stage non-small cell lung cancer.

Last month, the FDA approved a subcutaneous formulation of Keytruda, known as Keytruda Qlex, which can enhance patient convenience. With Keytruda’s intravenous or IV formulation set to lose exclusivity in 2028, the newly approved SC version comes with its own set of patents that extend protection well beyond that date.

MRK’s phase III pipeline has almost tripled since 2021, supported by in-house pipeline progress as well as the addition of candidates through M&A deals. This has positioned Merck to launch around 20 new vaccines and drugs over the next few years, with many having blockbuster potential. These include Merck’s new 21-valent pneumococcal conjugate vaccine, Capvaxive, and pulmonary arterial hypertension drug, Winrevair, which have the potential to generate significant revenues over the long term. Both products are off to strong starts.

Merck acquired Verona Pharma this year, which has added the latter’s chronic obstructive pulmonary disease or COPD drug, Ohtuvayre, to its portfolio. This addition strengthens Merck’s cardio-pulmonary pipeline and portfolio as the drug’s differentiated profile provides a significant edge over its competitors. Ohtuvayre's commercial launch is off to a solid start.

Merck’s Animal Health business is a key contributor to its top-line growth, as the company is recording above-market growth.

However, sales of Gardasil, which is Merck’s second-largest product, are declining due to weak performance in China, which resulted from sluggish demand trends amid an economic slowdown. Merck is also seeing weakness in the diabetes franchise and the generic erosion of some drugs.

Merck is heavily reliant on Keytruda. Though Keytruda may be Merck’s biggest strength and a solid reason to own the stock, it can also be argued that the company is excessively dependent on the drug, and it should look for ways to diversify its product lineup.

There are rising concerns about the firm’s ability to grow its non-oncology business ahead of the upcoming loss of exclusivity of Keytruda in 2028.

Also, competitive pressure might increase for Keytruda in the near future from dual PD-1/VEGF inhibitors like Summit Therapeutics’ (SMMT) ivonescimab that inhibit both the PD-1 pathway and the VEGF pathway at once. They are designed to overcome the limitations of single-target therapies like Keytruda. Pfizerrecently acquiredexclusive global ex-China rights to develop, manufacture and commercialize SSGJ-707, a dual PD-1 and VEGF inhibitor, from China’s 3SBio.

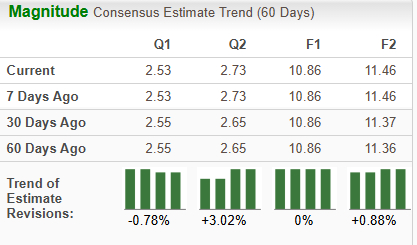

The Zacks Consensus Estimate for J&J’s 2025 sales and EPS implies a year-over-year increase of 5.4% and 8.8%, respectively. The Zacks Consensus Estimate for 2025 earnings has remained unchanged at $10.86 per share, while that for 2026 has risen from $11.37 to $11.46 over the past 30 days.

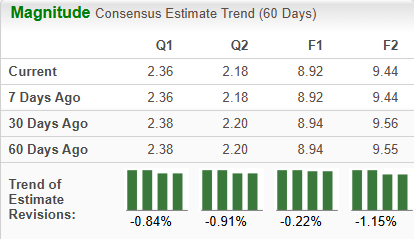

The Zacks Consensus Estimate for MRK’s 2025 sales and EPS implies a year-over-year increase of 0.9% and 16.6%, respectively. EPS estimates for both 2025 and 2026 have declined over the past 30 days.

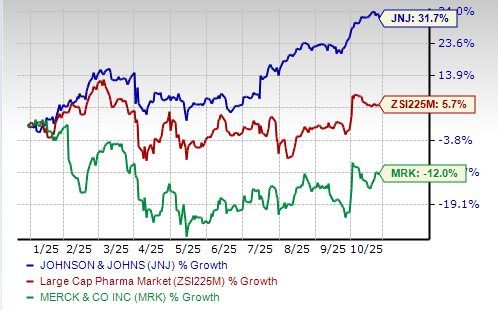

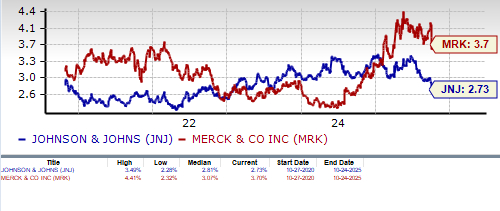

Year to date, J&J’s stock has risen 31.7% compared with theindustry’s increase of 5.7%. Merck’s stock has declined 12.0%.

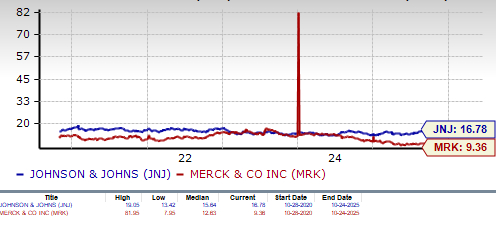

MRK looks more attractive than J&J from a valuation standpoint. Going by the price/earnings ratio, J&J’s shares currently trade at 16.78 forward earnings, higher than 15.59 for the industry and its 5-year mean of 15.64. Merck’s shares currently trade at 9.36 forward earnings, significantly lower than the industry as well as the stock’s 5-year mean of 12.63.

J&J’s dividend yield is 2.73% while Merck’s is slightly higher at 3.7%.

Merck & J&J have a Zacks Rank #3 (Hold) each, which makes choosing one stock a difficult task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merck has one of the world’s best-selling drugs in its portfolio, generating billions of dollars in revenues. Though Keytruda will lose patent exclusivity in 2028, its sales are expected to remain strong until then. After a weak sales performance in the first half, Merck expects to return to growth in the second half. It expects growth to be driven by oncology drugs, Animal Health, as well as new products, which will be partially offset by lower sales of Gardasil in China and Japan.

However, Merck’s problems are numerous at present, including persistent challenges for Gardasil in China, potential competition for Keytruda and rising competitive and generic pressure on some of its drugs. All these factors have raised doubts about Merck’s ability to navigate the Keytruda LOE period successfully. Consistently declining estimates also reflect analysts’ pessimistic outlook for the stock.

On the other hand, J&J has shown steady revenue and EPS growth for years. J&J looks quite optimistic that growth will accelerate in 2026. It believes the consensus estimates for 2026, for both the top and bottom lines, are too low. In 2026, J&J expects top-line growth of more than 5% while the consensus estimate is around 4.6%. EPS growth is expected to be similar to revenue growth. Adjusted earnings per share are expected to be around 5 cents more than the consensus of $11.39 per share. It expects sales growth in both segments to be higher in 2026. J&J also boasts strong cash flows and has consistently increased its dividends for 63 consecutive years.

Despite headwinds like softness in the MedTech unit, the legal battle surrounding its talc lawsuits, the Stelara patent cliff and the impact of Part D redesign, J&J's operating margin and financial position are stronger, which makes it a better pick over Merck. A large portion of Merck’s revenues comes from Keytruda, which faces LOE, a factor that tilts us in favor of J&J.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 16 min | |

| 46 min | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite