|

|

|

|

|||||

|

|

|

Western Digital Corporation (WDC) is slated to release first-quarter fiscal 2026 results on Oct. 30, after the closing bell.

The Zacks Consensus Estimate for earnings is pegged at $1.59, suggesting a decline of 10.7% from the prior-year quarter. Management projects non-GAAP earnings of $1.54 (+/- 15 cents).

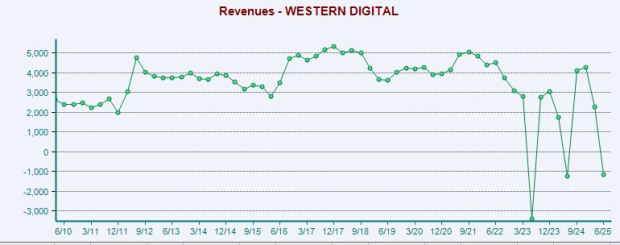

The consensus estimate for revenues is currently pegged at $2.72 billion, suggesting a 33.5% decline from the prior-year quarter’s figure. Western Digital anticipates non-GAAP revenues of $2.7 billion (+/- $100 million), up 22% year over year at the mid-point of its guidance.

The company's earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 6.8%.

Our proven model predicts an earnings beat for Western Digital this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Western Digital presently has an Earnings ESP of +1.89% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Rising AI-driven demand for high-capacity nearline HDDs and increased cloud spending for large, cost-effective storage are likely to have driven Western Digital’s fiscal first-quarter performance. In the fiscal fourth quarter of 2025, cloud services accounted for 90% of total revenues, reaching $2.6 billion, marking a 36% year-over-year increase.

The expansion of Agentic AI across various industries is fueling increased demand for unstructured data storage, while Western Digital is also using Agentic AI to accelerate product innovation. Although still in its early stages, this trend is gaining momentum globally. As AI continues to generate huge amounts of data, the need for scalable storage solutions is rapidly rising.

The reliability, scalability and total cost of ownership (TCO) benefits of its ePMR and UltraSMR technologies continue to be key drivers of its success in the data center market. Management expects robust revenue growth in the to-be-reported quarter, supported by strong demand for data centers and improved profitability due to higher adoption of high-capacity drives. WDC remains ahead of schedule on aero density advancements and stays focused on enhancing HAMR reliability and manufacturing yield. Its next-generation ePMR drives are on track to complete qualification by early 2026, ensuring a smooth and cost-effective transition to HAMR.

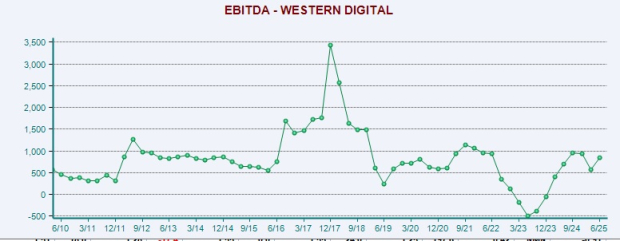

WDC’s margin performance is likely to have benefited from a shift toward higher-capacity drives. For the fiscal first quarter, it expects non-GAAP gross margin in the range of 41-42%, up from 38.5% reported in the prior year quarter. It reported a non-GAAP gross margin of 41.3%, up 610 basis points year over year and above its guidance (40-41%) in the fiscal fourth quarter 2025. Also, its dividend and buyback program signal strong capital allocation strategies.

However, higher-than-anticipated operational costs are likely to have pressured margins. For the fiscal first quarter, WDC expects operating expenses to rise sequentially to $370–$380 million from $345 million reported in the previous quarter. In addition, a leveraged balance sheet, macroeconomic swings due to changing global trade and tariff policies and intense competition from other leading storage providers remain headwinds for the company.

Nonetheless, WDC strengthened its balance sheet by cutting debt by $2.6 billion in the June quarter, achieving its leverage target and ending fiscal 2025 with $4.7 billion in gross debt.

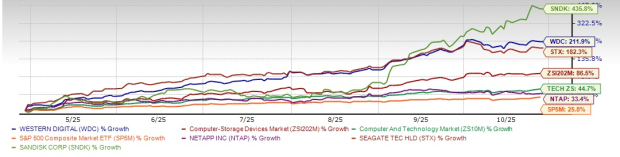

WDC shares have rallied 211.9% in the past six months, outperforming the Zacks Computer-Storage Devices industry’s rise of 86.5%. The stock has also outpaced the Zacks Computer & Technology sector and the S&P 500’s growth of 44.7% and 25.8%, respectively.

The company has outperformed its competitor in the storage space, like NetApp, Inc. (NTAP) and its fierce rival in the HDD business, Seagate Technology Holdings plc (STX). NTAP and STX have gained 33.4% and 182.3%, respectively, in the same time frame. WDC has, however, underperformed the newly separated Flash business from its own, Sandisk Corporation (SNDK). SNDK has soared 435.8%.

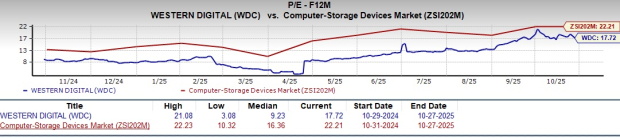

From a valuation standpoint, WDC appears to be trading relatively cheaper compared with the industry but trading above its mean. Going by the price/earnings ratio, the company’s shares currently trade at 17.72 forward earnings, lower than 22.21 for the industry but above the stock’s mean of 9.23.

NTAP, STX and SNDK are trading at multiples of 14.26X, 19.87X and 23.08X, respectively, compared with the Zacks Computer Storage Devices, Zacks Computer-Integrated Systems industry and Zacks Technology Services industry’s ratio of 22.21, 26.17 and 27.1, respectively.

Despite tariff uncertainties, Western Digital is benefiting from strong AI-driven demand, rapid adoption of high-capacity drives and solid customer ties. The company is improving margins, generating strong cash flow, cutting debt and returning capital to shareholders. Management expects continued revenue and margin gains in the first-quarter fiscal 2026, supported by customer commitments and operational strength.

Investors should consider buying WDC stock now, as strong AI-driven demand and related industry tailwinds are fueling growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite