|

|

|

|

|||||

|

|

|

Even though Hilton (currently trading at $260 per share) has gained 14.8% over the last six months, it has lagged the S&P 500’s 23.9% return during that period. This may have investors wondering how to approach the situation.

Is HLT a buy right now? Or is its underperformance reflective of its business quality?

Founded in 1919, Hilton Worldwide (NYSE:HLT) is a global hospitality company with a portfolio of hotel brands.

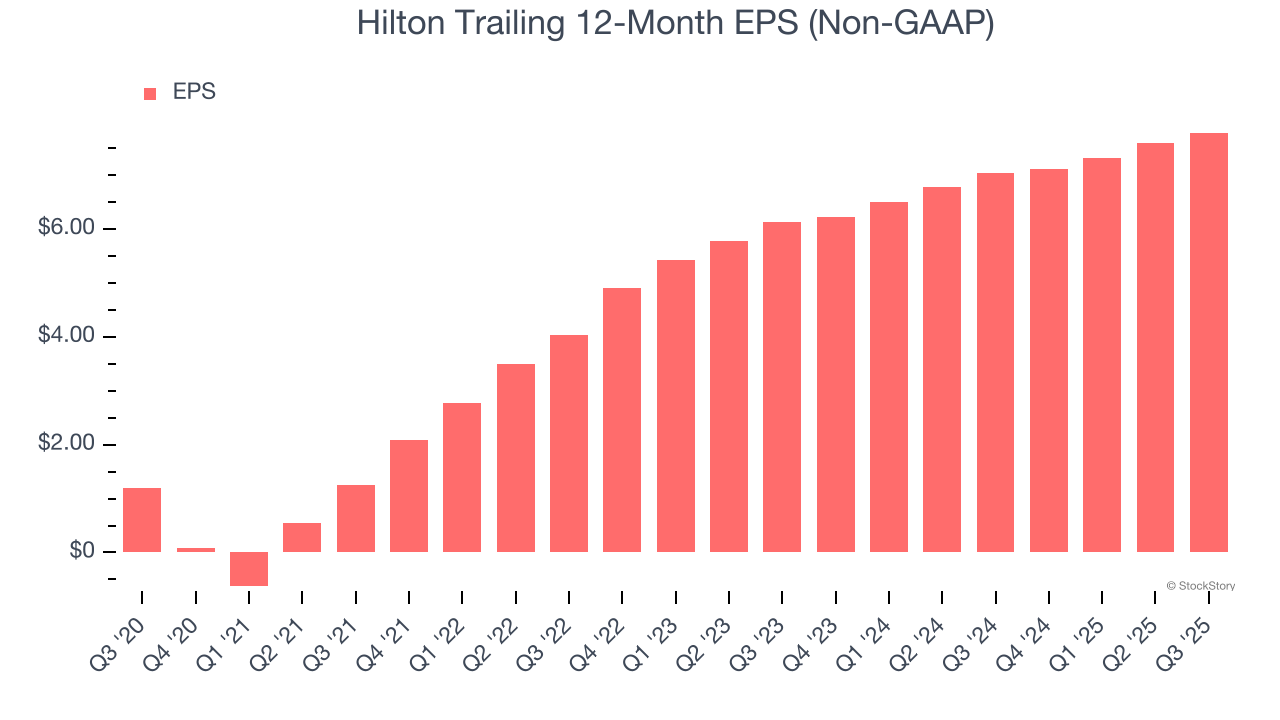

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Hilton’s EPS grew at an astounding 45.6% compounded annual growth rate over the last five years, higher than its 15.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Hilton’s ROIC has increased significantly. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

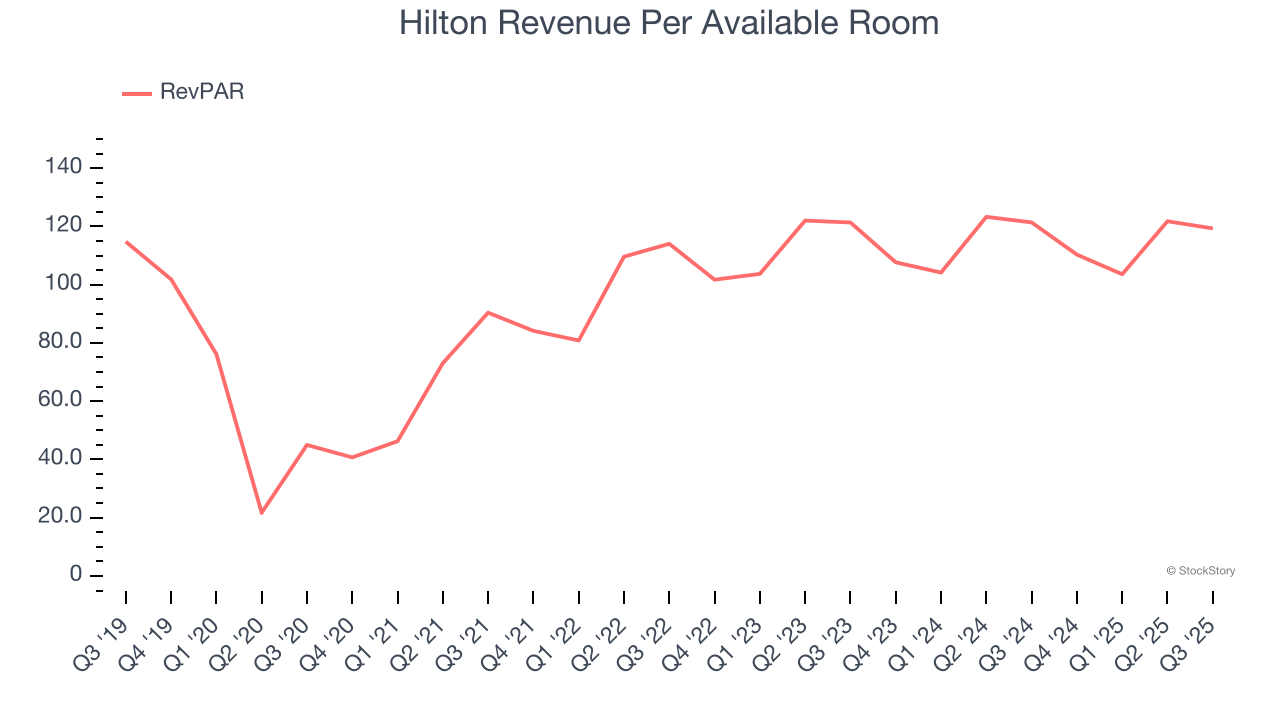

Investors interested in Travel and Vacation Providers companies should track RevPAR (revenue per available room) in addition to reported revenue. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Hilton’s demand characteristics.

Over the last two years, Hilton failed to grow its RevPAR, which came in at $119.33 in the latest quarter. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Hilton might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

Hilton has huge potential even though it has some open questions. With its shares lagging the market recently, the stock trades at 29.5× forward P/E (or $260 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-31 | |

| Mar-21 | |

| Mar-19 | |

| Mar-17 | |

| Mar-17 | |

| Mar-13 | |

| Mar-11 | |

| Mar-10 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-02 | |

| Mar-01 | |

| Feb-27 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite