|

|

|

|

|||||

|

|

|

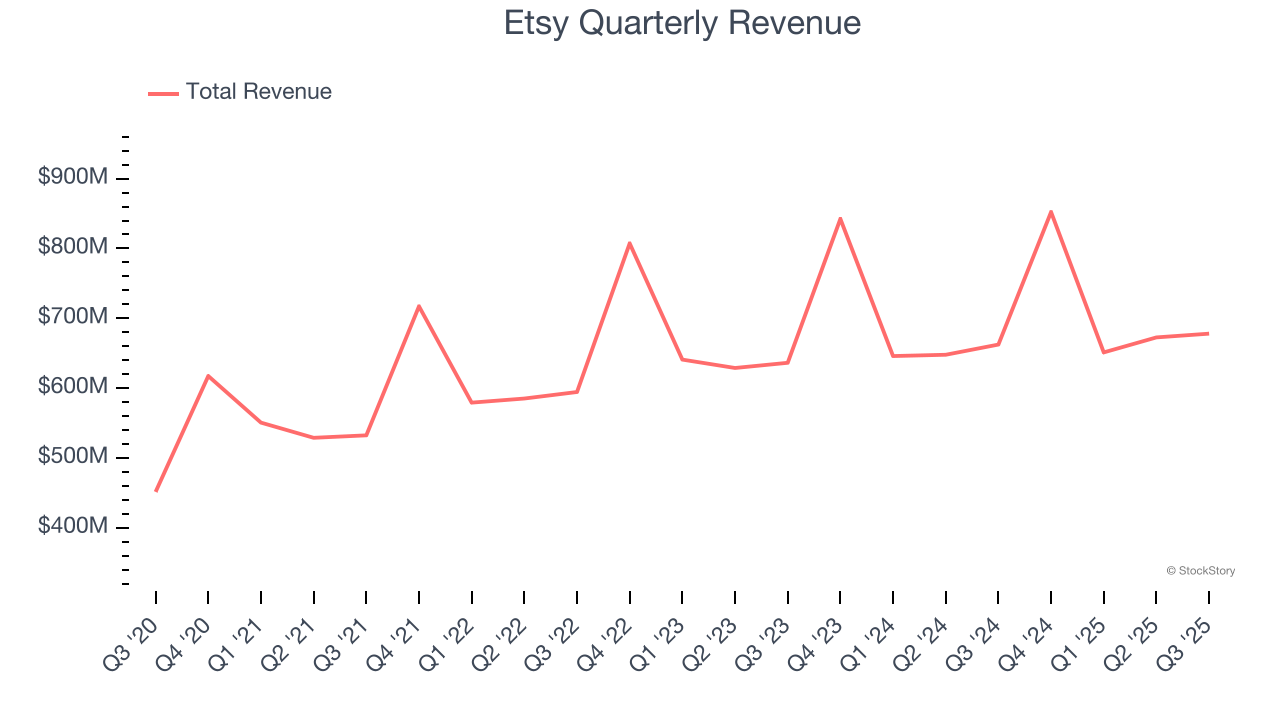

Online marketplace Etsy (NASDAQ:ETSY) announced better-than-expected revenue in Q3 CY2025, with sales up 2.4% year on year to $678 million. Its GAAP profit of $0.63 per share was 21.1% above analysts’ consensus estimates.

Is now the time to buy Etsy? Find out by accessing our full research report, it’s free for active Edge members.

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Etsy grew its sales at a sluggish 4.9% compounded annual growth rate. This was below our standard for the consumer internet sector and is a rough starting point for our analysis.

This quarter, Etsy reported modest year-on-year revenue growth of 2.4% but beat Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

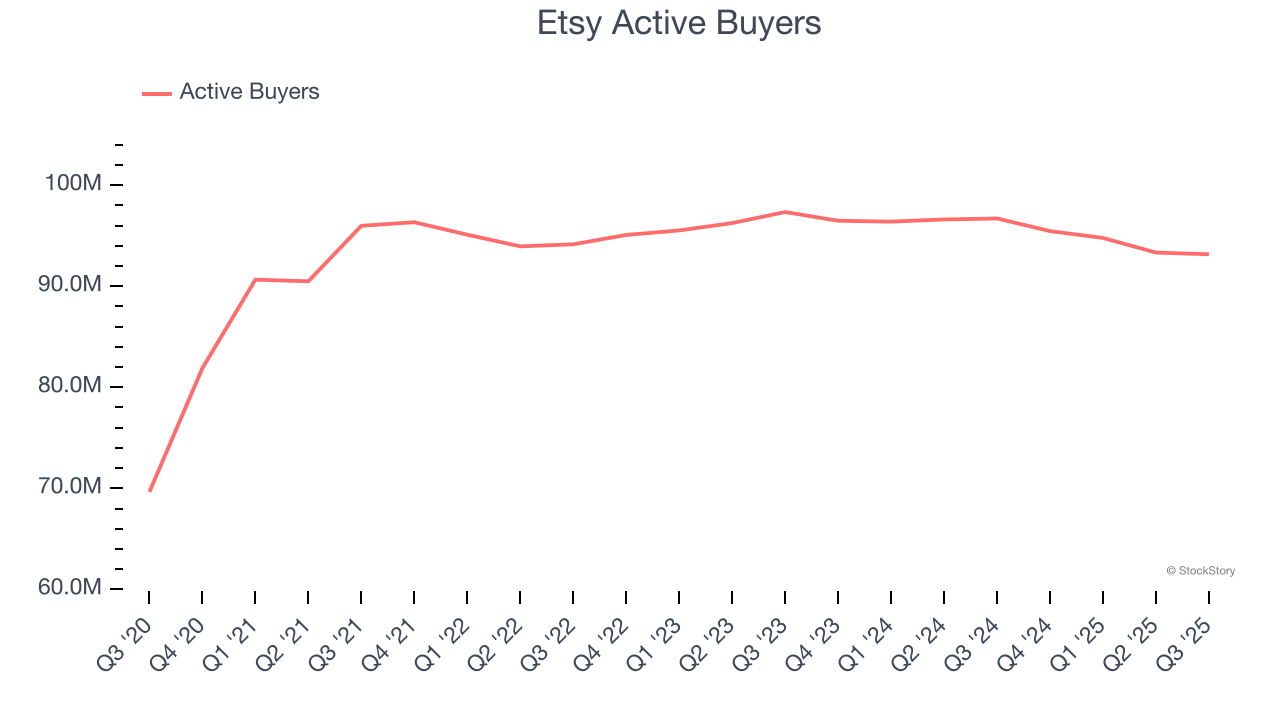

As an online marketplace, Etsy generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Etsy struggled with new customer acquisition over the last two years as its active buyers were flat at 93.16 million. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Etsy wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q3, Etsy’s active buyers decreased by 3.55 million, a 3.7% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

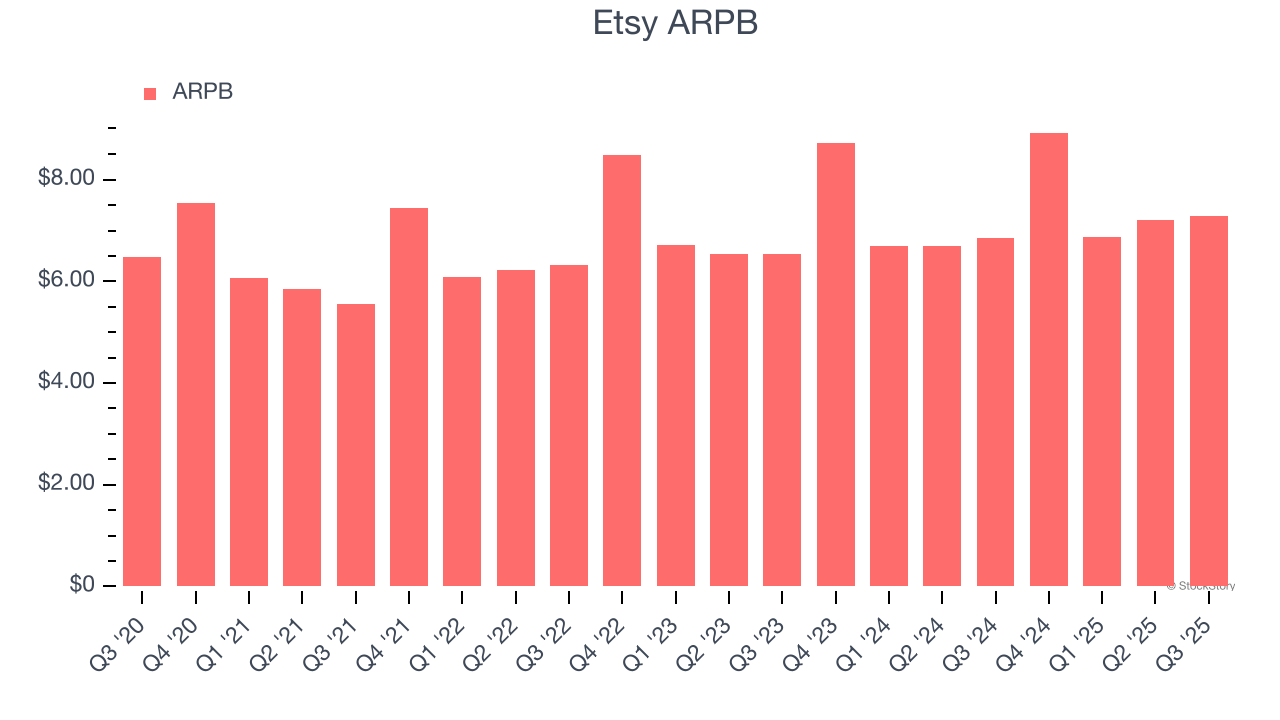

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the company earns in transaction fees from each buyer. ARPB also gives us unique insights into a user’s average order size and Etsy’s take rate, or "cut", on each order.

Etsy’s ARPB growth has been mediocre over the last two years, averaging 3.6%. This raises questions about its platform’s health when paired with its flat active buyers. If Etsy wants to grow its buyers, it must either develop new features or lower its monetization of existing ones.

This quarter, Etsy’s ARPB clocked in at $7.28. It grew by 6.3% year on year, faster than its active buyers.

We enjoyed seeing Etsy beat analysts’ revenue and EBITDA expectations this quarter. On the other hand, its number of buyers declined and the company guided to EBITDA margin of 24% next quarter, well below expectations of 27%. This margin outlook is weighing on shares, and the stock traded down 8% to $68.85 immediately following the results.

So do we think Etsy is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Mar-10 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 |

Booking Stock, Expedia, DoorDash Jump. Here's What's Behind A 'Relief Rally.'

ETSY

Investor's Business Daily

|

| Mar-03 | |

| Mar-03 | |

| Mar-02 | |

| Mar-02 | |

| Mar-01 | |

| Feb-28 | |

| Feb-27 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite