|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

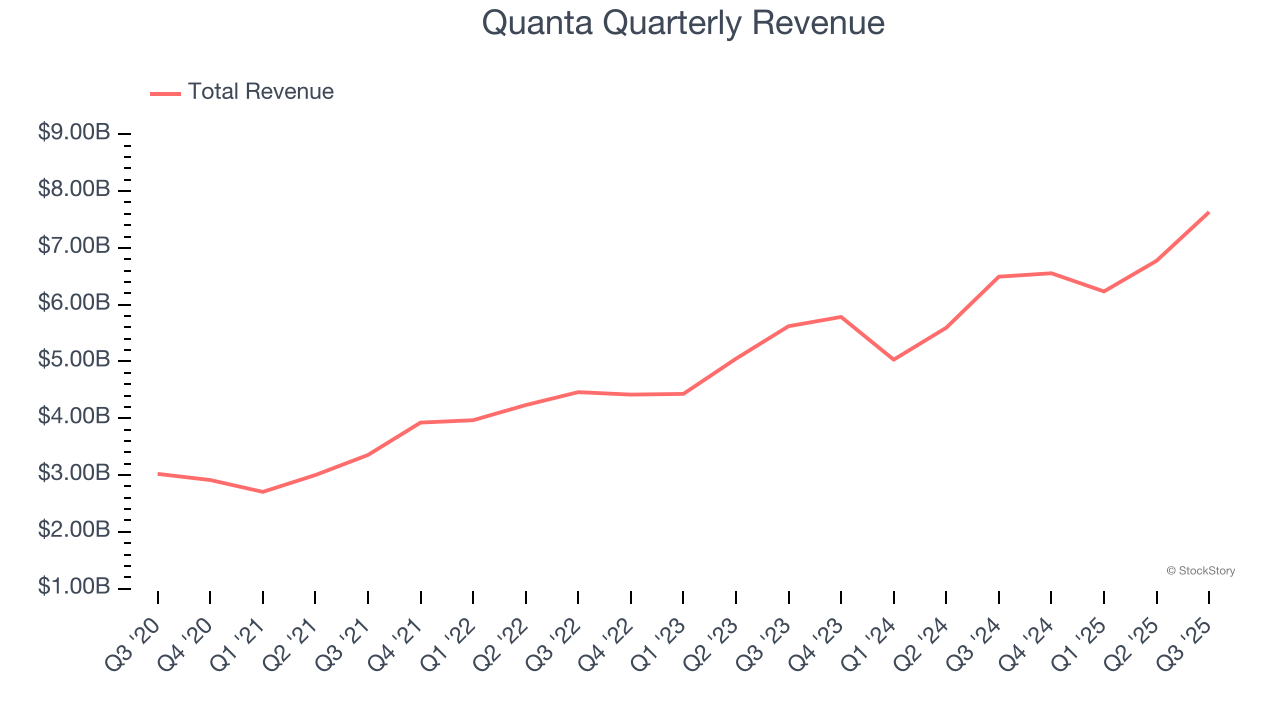

Infrastructure solutions provider Quanta (NYSE:PWR) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 17.5% year on year to $7.63 billion. The company’s full-year revenue guidance of $28 billion at the midpoint came in 0.9% above analysts’ estimates. Its non-GAAP profit of $3.33 per share was 2.2% above analysts’ consensus estimates.

Is now the time to buy Quanta? Find out by accessing our full research report, it’s free for active Edge members.

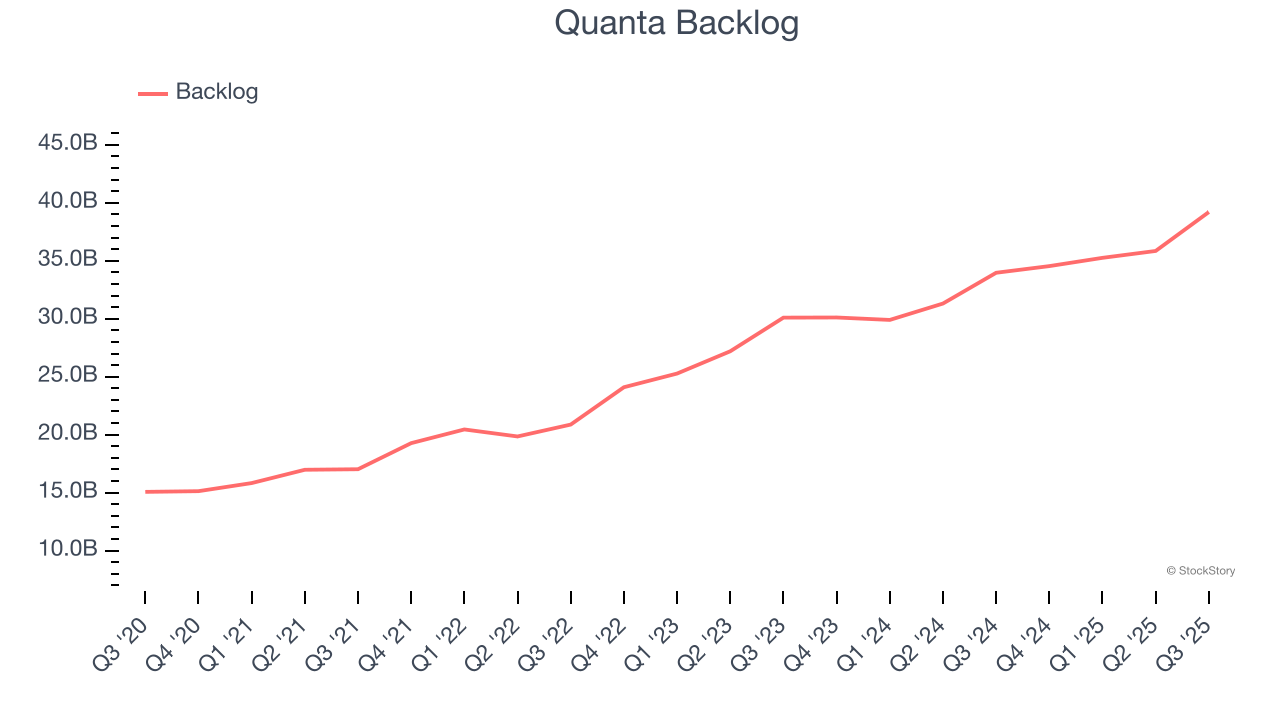

"Quanta delivered another quarter of strong results, achieving double-digit growth in revenue, adjusted EBITDA and adjusted EPS compared to the prior year, alongside record backlog of $39.2 billion, which reflects accelerating demand in our Electric segment, robust activity across our end markets and momentum for 2026. These results demonstrate the power of our portfolio, the strength of our craft-skilled workforce and our ability to provide certainty through world-class execution for our customers as they modernize and expand critical infrastructure," said Duke Austin, President and Chief Executive Officer of Quanta Services.

A construction engineering services company, Quanta (NYSE:PWR) provides infrastructure solutions to a variety of sectors, including energy and communications.

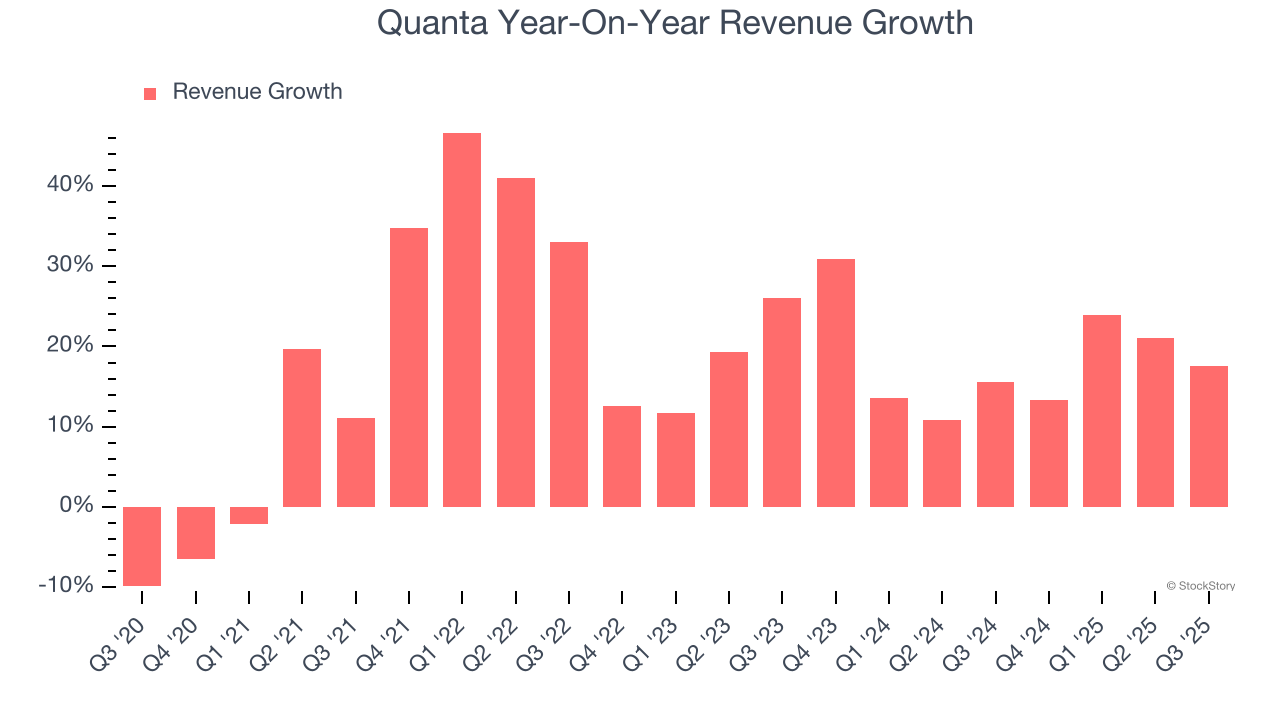

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Quanta’s 19% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Quanta’s annualized revenue growth of 18% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Quanta’s backlog reached $39.2 billion in the latest quarter and averaged 16.7% year-on-year growth over the last two years. Because this number is in line with its revenue growth, we can see the company effectively balanced its new order intake and fulfillment processes.

This quarter, Quanta reported year-on-year revenue growth of 17.5%, and its $7.63 billion of revenue exceeded Wall Street’s estimates by 2.8%.

Looking ahead, sell-side analysts expect revenue to grow 11.6% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and suggests the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

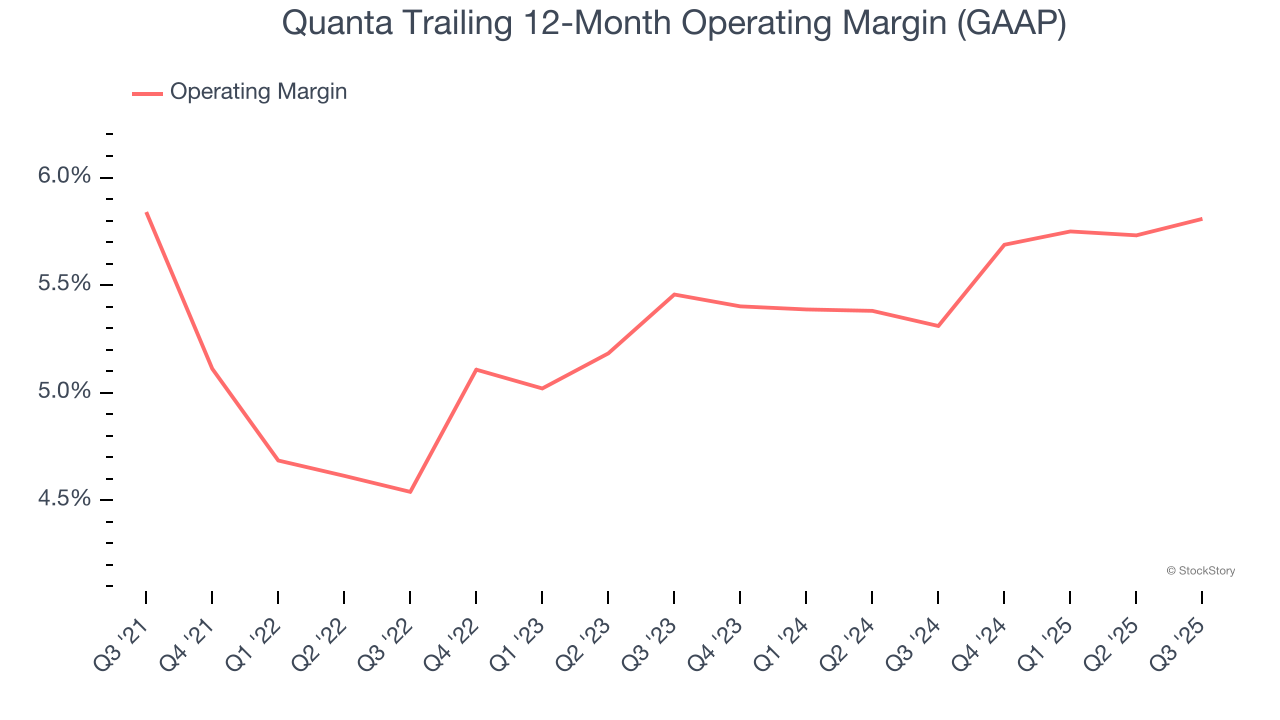

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Quanta’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 5.4% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Quanta’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, Quanta generated an operating margin profit margin of 6.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

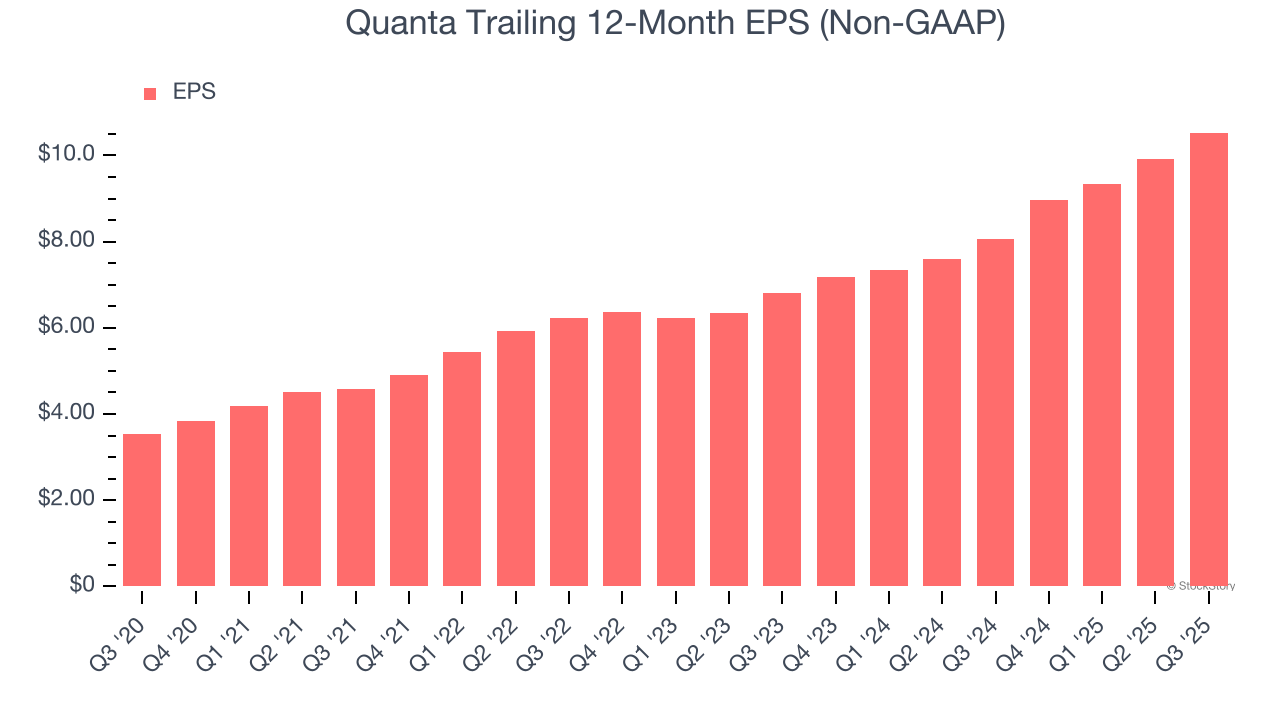

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Quanta’s EPS grew at an astounding 24.4% compounded annual growth rate over the last five years, higher than its 19% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Quanta, its two-year annual EPS growth of 24.3% is similar to its five-year trend, implying strong and stable earnings power.

In Q3, Quanta reported adjusted EPS of $3.33, up from $2.72 in the same quarter last year. This print beat analysts’ estimates by 2.2%. Over the next 12 months, Wall Street expects Quanta’s full-year EPS of $10.53 to grow 14.6%.

We were impressed by how significantly Quanta blew past analysts’ backlog expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 1.3% to $443 immediately following the results.

So should you invest in Quanta right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| 11 hours | |

| 14 hours | |

| 22 hours | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Stock Market Today: Dow Sinks Amid U.S.-Iran Jitters; This Retail Stock Tumbles (Live Coverage)

PWR +6.68%

Investor's Business Daily

|

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Stock Market Today: Dow Slides After Surprise Jobless Claims; AI Stock Jumps (Live Coverage)

PWR +6.68%

Investor's Business Daily

|

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite