|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

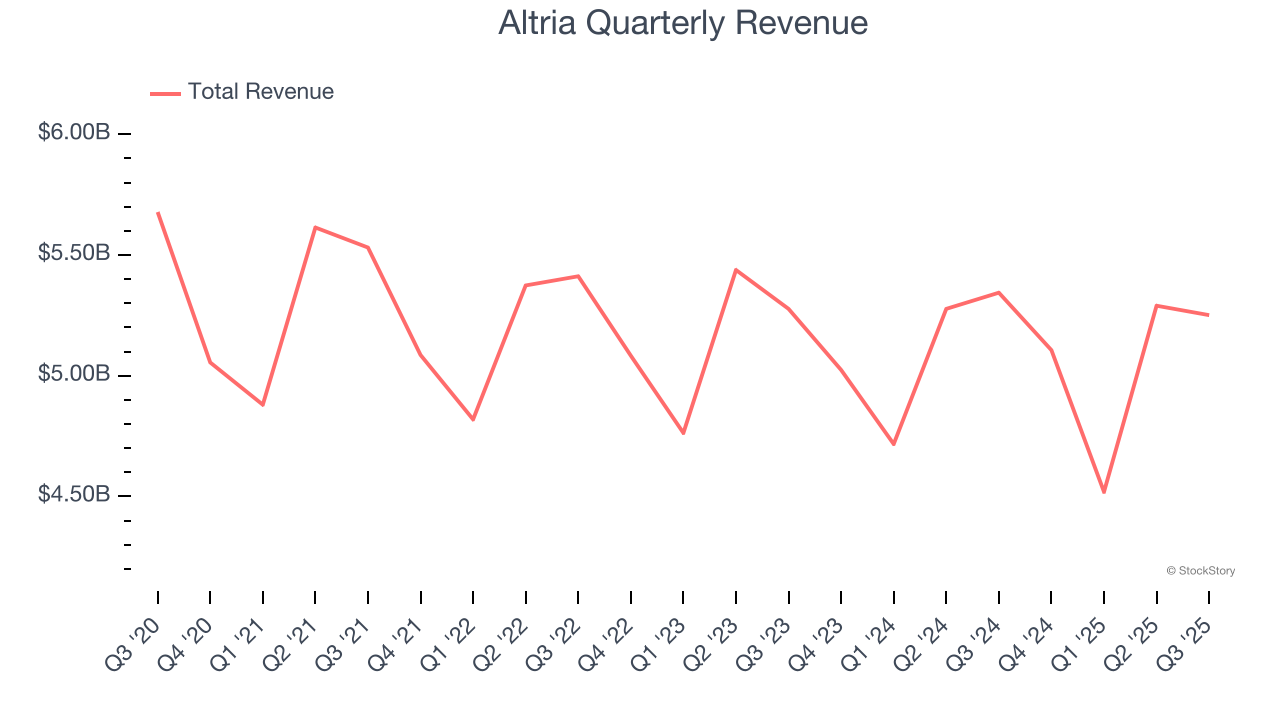

Tobacco company Altria (NYSE:MO) fell short of the market’s revenue expectations in Q3 CY2025, with sales falling 1.7% year on year to $5.25 billion. Its non-GAAP profit of $1.45 per share was in line with analysts’ consensus estimates.

Is now the time to buy Altria? Find out by accessing our full research report, it’s free for active Edge members.

Best known for its Marlboro brand of cigarettes, Altria (NYSE:MO) offers tobacco and nicotine products.

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $20.17 billion in revenue over the past 12 months, Altria is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To accelerate sales, Altria likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Altria struggled to increase demand as its $20.17 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a tough starting point for our analysis.

This quarter, Altria missed Wall Street’s estimates and reported a rather uninspiring 1.7% year-on-year revenue decline, generating $5.25 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products will spur better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

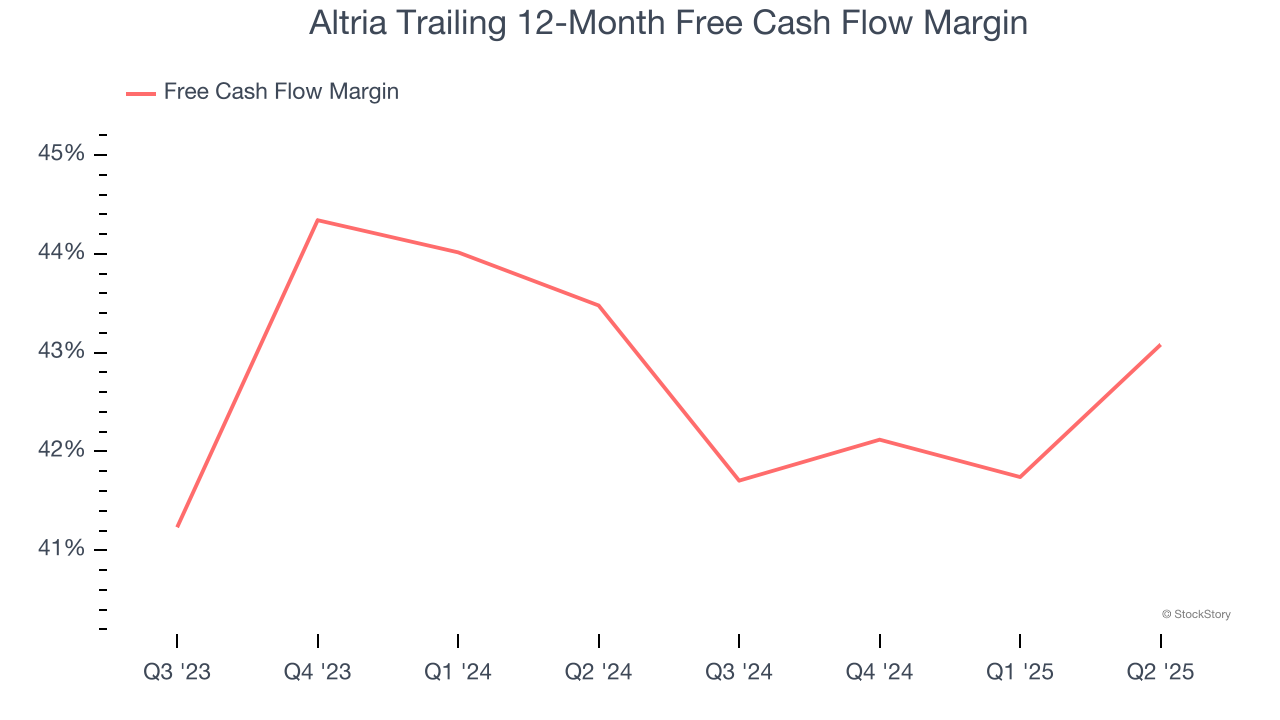

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Altria has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging an eye-popping 41.5% over the last two years.

We struggled to find many positives in these results. Its revenue missed and its gross margin fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.9% to $58.29 immediately after reporting.

The latest quarter from Altria’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite