|

|

|

|

|||||

|

|

|

Altria Group Inc. (MO) posted third-quarter 2025 results, wherein the top line missed the Zacks Consensus Estimate and declined year over year. On the contrary, the bottom line beat the consensus mark and improved from the year-ago period.

Altria reported strong third-quarter momentum, highlighting the resilience of its core tobacco business, continued progress in its smoke-free portfolio and new opportunities for long-term growth in international modern oral and U.S. non-nicotine products.

Altria’s third-quarter adjusted earnings were $1.45 per share, which advanced 3.6% year over year and beat the Zacks Consensus Estimate of $1.44. This upside was driven by reduced shares outstanding and increased adjusted operating companies' income (“OCI”).

Altria Group, Inc. price-consensus-eps-surprise-chart | Altria Group, Inc. Quote

The company posted net revenues of $6,072 million, which declined 3% year over year. This was due to a decrease in net revenues in the smokeable products segment and the oral tobacco products segment. Revenues, net of excise taxes, decreased 1.7% to $5,251 million. The top line missed the consensus mark, which was pegged at $5,321 million.

Smokeable Products: Net revenues in the category fell 2.8% year over year to $5,387 million due to reduced shipment volume and elevated promotional investments. These were somewhat offset by higher pricing. Revenues, net of excise taxes, fell 1.3%.

Domestic cigarette shipment volumes tumbled 8.2% due to the industry’s decline rate and retail share losses, partially offset by trade inventory movements. The industry’s decline was a result of the continued growth of flavored disposable e-vapor products and persistent discretionary income challenges for Adult Tobacco Consumers (“ATC”). Altria’s reported cigar shipment volumes increased 2%.

Adjusted OCI in the segment jumped 0.7% to $2,956 million due to improved pricing and reduced per-unit settlement charges. This was somewhat negated by reduced shipment volume, elevated promotional investments and higher costs. The adjusted OCI margins grew 1.3 percentage points to 64.4%.

Oral Tobacco Products: Net revenues of the segment fell 4.6% to $689 million. The downside was due to the reduced shipment volume and the increased percentage of on! shipment volume compared with the MST year over year (mix change), this was partially offset by increased pricing. Revenues excluding excise taxes fell 4.3%.

Domestic shipment volumes fell 9.6%, due to retail share losses, calendar timing differences, trade inventory movements and other factors. This was partly negated by the industry’s growth rate.

Adjusted OCI in the segment decreased 0.9%, due to a decline in shipment volumes and a change in mix, partially offset by increased pricing and lower costs. The adjusted OCI margin grew 2.4 percentage points to 69.2%.

This Zacks Rank #2 (Buy) company ended the quarter with cash and cash equivalents of $3,472 million, long-term debt of $24,132 million and a total stockholders’ deficit of $2,646 million.

In the third quarter of 2025, the company bought back 1.9 million shares, totaling $112 million. Through the first nine months of the year, the company repurchased 12.3 million shares for a total cost of $712 million. Management approved an increase in the existing share repurchase program authorization from $1 billion to $2 billion and extended the program’s expiration to Dec. 31, 2026.

Altria paid dividends worth $1.7 billion in the third quarter.

The company now expects 2025 adjusted earnings per share (EPS) in the range of $5.37 to $5.45, indicating year-over-year growth of 3.5% to 5% from a base of $5.19 in 2024. Earlier, the metric was expected in the $5.35 to $5.45 per share range, implying 3% to 5% growth.

The company’s 2025 guidance implies the currently estimated cost impact of increased tariffs, based on the most recent available information. It also assumes minimal disruption to combustible and e-vapor product volumes from ongoing enforcement actions targeting the illicit e-vapor market. In addition, the guided range factors in the reinvestment of expected cost savings from the Optimize & Accelerate initiative, along with lower forecasted net periodic benefit income.

As the external landscape remains dynamic, Altria continues assessing economic factors like inflation and tariffs, ATC dynamics (such as purchasing patterns and the adoption of smoke-free products), illegal e-vapor enforcement and regulatory developments.

The bottom-line view also considers planned investments associated with enhanced smoke-free product research, development and marketplace activities to support MO’s smoke-free products.

Altria continues to expect a 2025 adjusted effective tax rate of 23-24%, capital expenditures of $175-$225 million, and depreciation and amortization expenses of approximately $290 million.

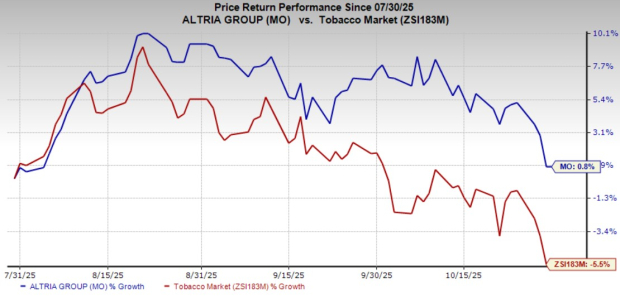

Shares of MO have gained 0.8% in the past three months against the industry’s 5.5% decline.

United Natural Foods, Inc. (UNFI) distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. At present, United Natural sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for United Natural’s current fiscal-year sales and earnings implies growth of 2.5% and 167.6%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 416.2%, on average.

Lamb Weston Holdings, Inc. (LW) engages in the production, distribution and marketing of frozen potato products in the United States, Canada, Mexico and internationally. It sports a Zacks Rank #1 at present. LW delivered a trailing four-quarter earnings surprise of 16%, on average.

The Zacks Consensus Estimate for Lamb Weston's current fiscal-year sales indicates growth of 1.3% from the prior-year levels.

Vital Farms (VITL) packages, markets and distributes shell eggs, butter and other products in the United States. It flaunts a Zacks Rank #1 at present. Vital Farms delivered a trailing four-quarter earnings surprise of 35.8%, on average.

The Zacks Consensus Estimate for Vital Farms’ current fiscal-year sales and earnings implies an increase of 27.2% and 16.1%, respectively, from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-16 | |

| Jul-16 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-03 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite