|

|

|

|

|||||

|

|

|

Cable, internet, and telephone services provider Charter (NASDAQ:CHTR) met Wall Streets revenue expectations in Q3 CY2025, but sales were flat year on year at $13.67 billion. Its GAAP profit of $8.34 per share was 11.2% below analysts’ consensus estimates.

Is now the time to buy Charter? Find out by accessing our full research report, it’s free for active Edge members.

"We are operating well in a competitive environment, where consumer products and applications haven't yet caught up with our uniquely differentiated network capabilities," said Chris Winfrey, President and CEO of Charter.

Operating as Spectrum, Charter (NASDAQ:CHTR) is a leading telecommunications company offering cable television, high-speed internet, and voice services across the United States.

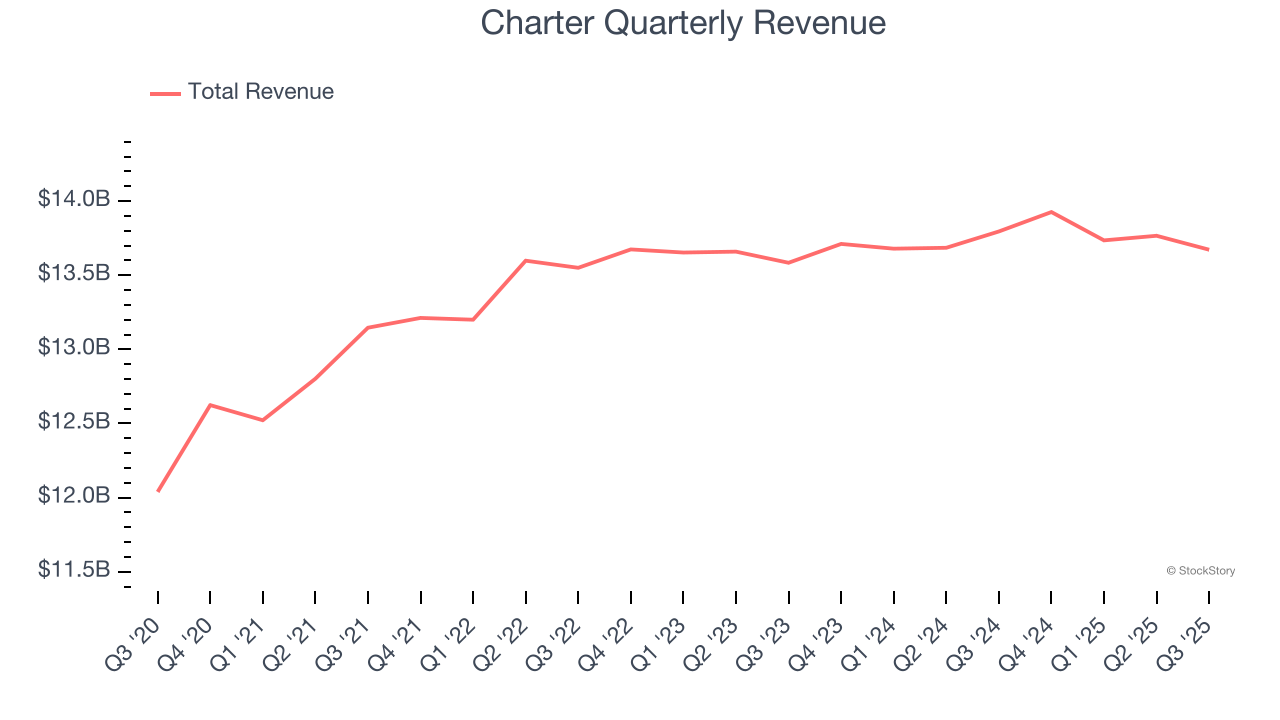

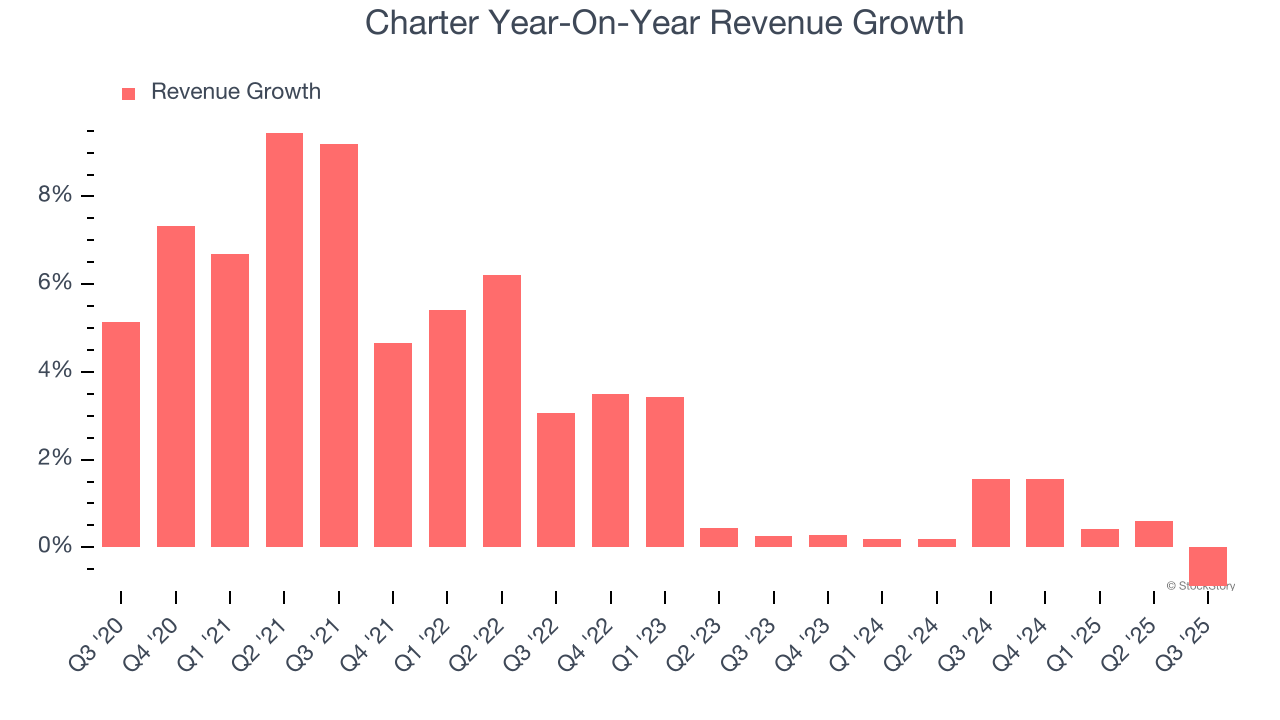

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Charter’s sales grew at a sluggish 3.1% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Charter’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

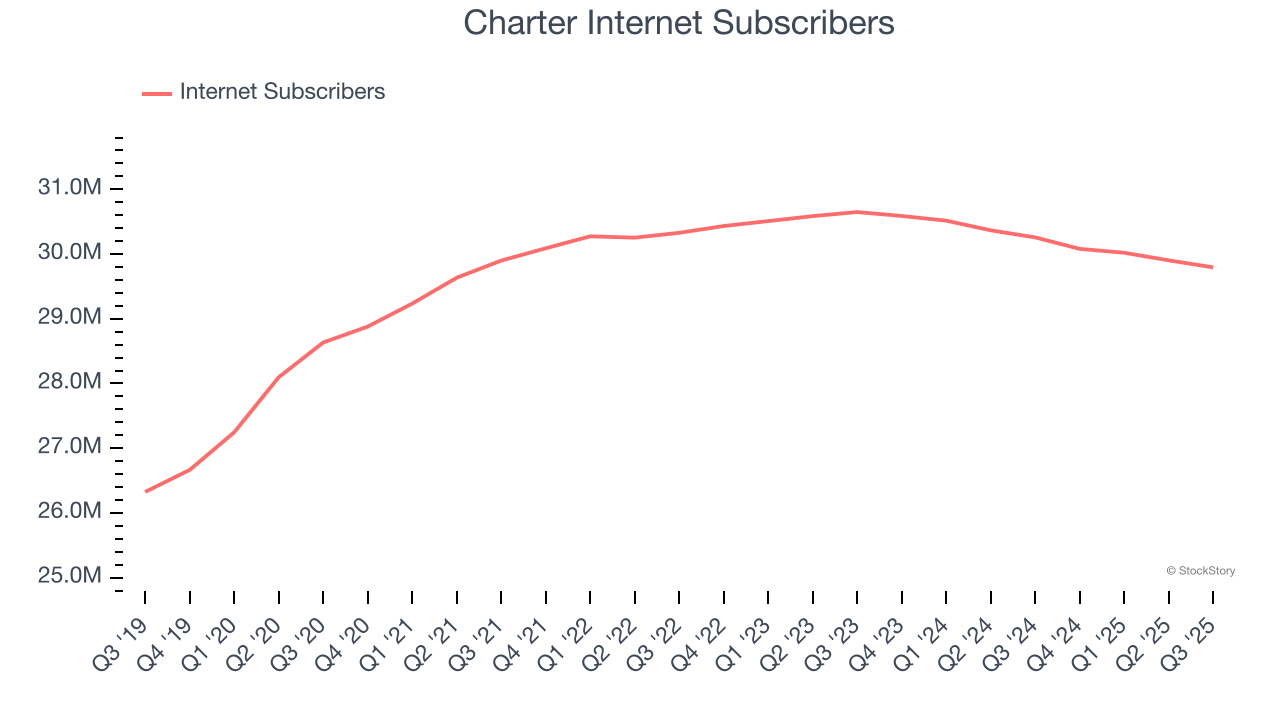

We can dig further into the company’s revenue dynamics by analyzing its number of internet subscribers and video subscribers, which clocked in at 29.79 million and 12.56 million in the latest quarter. Over the last two years, Charter’s internet subscribers were flat while its video subscribers averaged 7.3% year-on-year declines.

This quarter, Charter’s $13.67 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

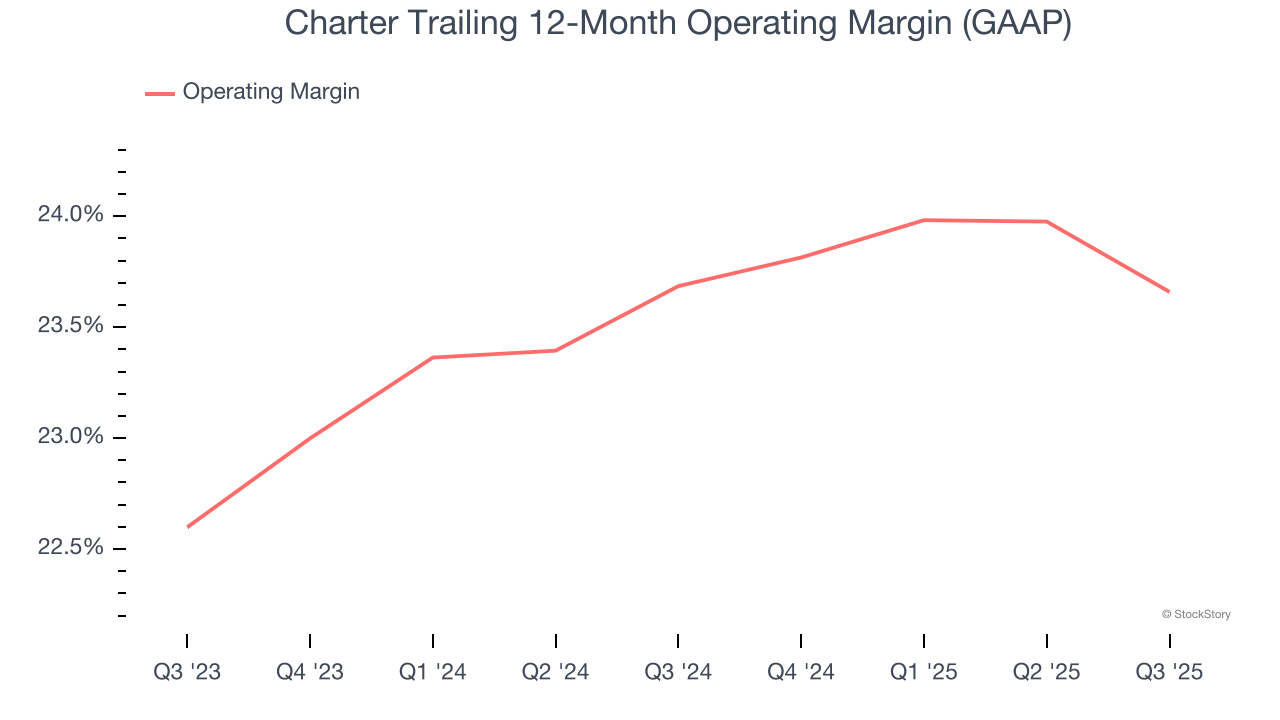

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Charter’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 23.7% over the last two years. This profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

This quarter, Charter generated an operating margin profit margin of 22.9%, down 1.3 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

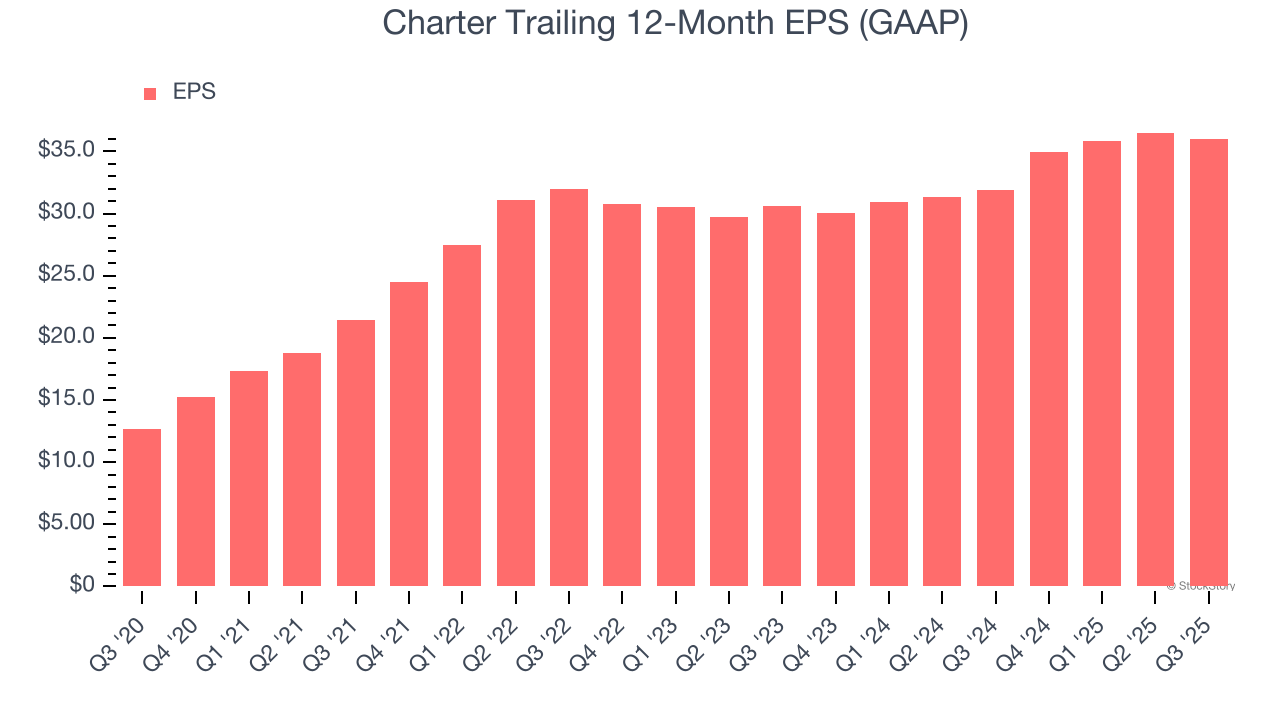

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Charter’s EPS grew at a spectacular 23.2% compounded annual growth rate over the last five years, higher than its 3.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q3, Charter reported EPS of $8.34, down from $8.82 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Charter’s full-year EPS of $36.03 to grow 18.3%.

We struggled to find many positives in these results. Its EPS missed Wall Street’s estimates and its internet subscriber count declined. Overall, this was a softer quarter. The stock traded down 4.3% to $221.03 immediately after reporting.

The latest quarter from Charter’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Mar-31 | |

| Mar-24 | |

| Mar-23 | |

| Mar-16 | |

| Mar-16 | |

| Mar-13 | |

| Mar-11 | |

| Mar-11 | |

| Mar-09 | |

| Mar-09 | |

| Mar-08 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 | |

| Feb-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite