|

|

|

|

|||||

|

|

|

Taiwan Semiconductor Manufacturing is gaining market share in the AI era.

The company's pick-and-shovel position in AI chips could drive outsized growth as data center spending continues to surge.

The current stock price doesn't fully reflect TSMC's upside.

Taiwan Semiconductor Manufacturing (NYSE: TSM) or TSMC for short, has been a clear winner in the early innings of the artificial intelligence (AI) era. The world's largest foundry, a semiconductor manufacturer, has been the go-to manufacturing partner for leading AI chip companies. These chips end up in data centers, where they work in clusters to train and run artificial intelligence models.

Companies have already invested hundreds of billions of dollars in data centers, and it seems likely this trend will continue for at least the next several years. This positions TSMC for potentially explosive growth, as evidenced by market data.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Here is what you need to know.

Image source: Getty Images.

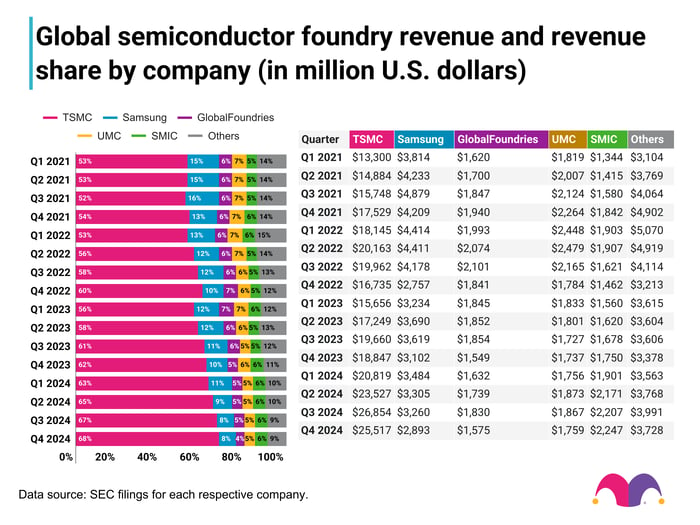

The Motley Fool compiled quarterly data from the world's leading foundries to illustrate market share trends. Here, you can see that TSMC is not only the market leader by a significant margin but has also increased its share, especially over the past three years.

Image source: The Motley Fool.

That timeline coincides with the AI data center boom. TSMC's quarterly revenue has nearly doubled to $25.5 billion over that time. It's no coincidence, either. Nvidia has dominated the AI data center chip space with market share estimates as high as 92%. Which company builds Nvidia's AI chips? That would be TSMC, which manufactures Nvidia's initial flagship Hopper AI chip and its successor, Blackwell.

TSMC also builds for several of Nvidia's potential competitors, including Broadcom, Qualcomm, and Advanced Micro Devices. Therefore, TSMC is likely to continue to thrive, even if Nvidia loses some market share to these competitors.

Simply put, TSMC boasts a clear competitive advantage over other foundries, thanks to its combination of production capacity, equipment, and expertise that enables it to produce high volumes of very complex chips efficiently.

Even if another foundry undercuts TSMC's pricing, the stakes are so high with AI that a chip company may pay a premium for the manufacturing certainty TSMC offers.

Admittedly, it can be hard to wrap one's mind around the idea of spending hundreds of billions of dollars on a seemingly endless array of data centers. It might be best to view data centers as the foundation on which AI will enable new technologies and industries -- much as has already happened in cloud computing.

Think about the possibilities in new AI software applications, self-driving vehicles, and humanoid robotics. These require immense computing power, and AI hyperscalers -- companies such as Amazon, Microsoft, Alphabet, and Meta Platforms -- have already put their financial chips on the table.

Experts don't see this trend backtracking, either. Researchers at McKinsey & Company estimate that global data center expenditures will approach $6.7 trillion over the next five years alone. Most of that will go toward AI data centers, with roughly $1.5 trillion in spending for traditional IT applications.

Investors have already enjoyed a stellar year from TSMC, with shares up over 55% over the past 12 months. However, there seems to be more room to run.

The continued investments in data centers and AI chip clusters filling them bode well for Taiwan Semiconductor. Wall Street analysts currently estimate the company will grow its earnings by an average of 29% annually over the next three to five years. Consider that the stock currently trades at a price-to-earnings ratio of 31.

Using the PEG ratio to weigh Taiwan Semiconductor's valuation against its anticipated earnings growth, its current ratio of just under 1.1 indicates that the stock is a bargain -- assuming it meets those growth estimates.

Based on the market share data above, Taiwan Semiconductor's competitive position appears to be as strong as ever. Therefore, it's hard to envision the company and stock flopping for investors unless broader data center investments unexpectedly dry up.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $603,392!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,241,236!*

Now, it’s worth noting Stock Advisor’s total average return is 1,072% — a market-crushing outperformance compared to 194% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 27, 2025

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 3 hours | |

| 6 hours | |

| 9 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite