|

|

|

|

|||||

|

|

|

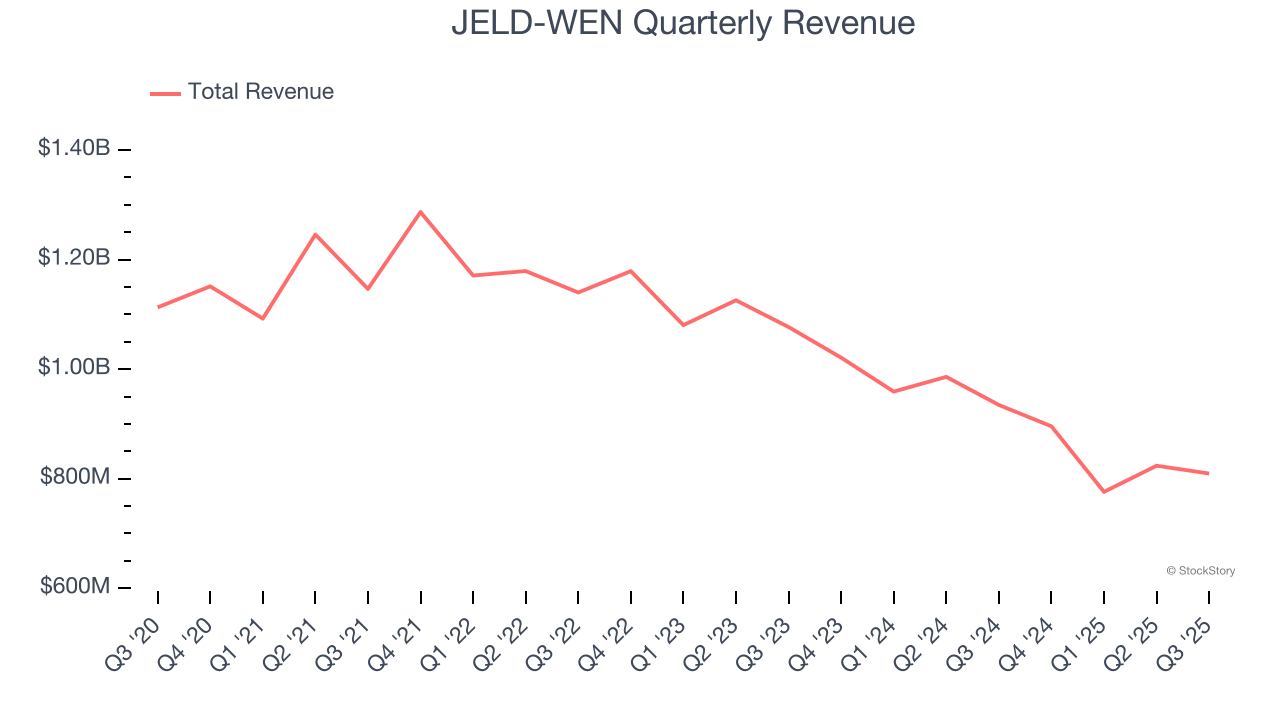

Building products manufacturer JELD-WEN (NYSE:JELD) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 13.4% year on year to $809.5 million. The company’s full-year revenue guidance of $3.15 billion at the midpoint came in 2.9% below analysts’ estimates. Its non-GAAP loss of $0.20 per share was significantly below analysts’ consensus estimates.

Is now the time to buy JELD-WEN? Find out by accessing our full research report, it’s free for active Edge members.

"Third-quarter results fell short of our expectations due to persistent market headwinds and price-cost pressures," said Chief Executive Officer William J. Christensen.

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE:JELD) manufactures doors, windows, and other related building products.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. JELD-WEN struggled to consistently generate demand over the last five years as its sales dropped at a 4.5% annual rate. This was below our standards and is a sign of poor business quality.

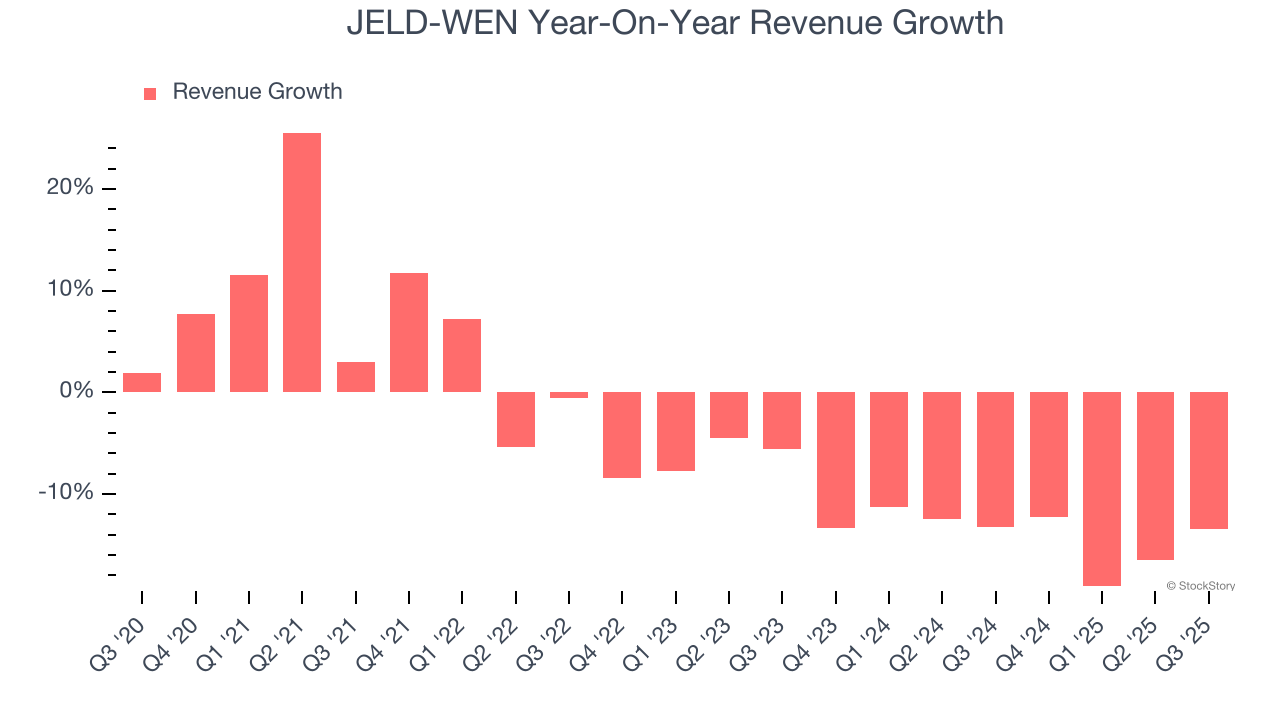

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. JELD-WEN’s recent performance shows its demand remained suppressed as its revenue has declined by 13.9% annually over the last two years.

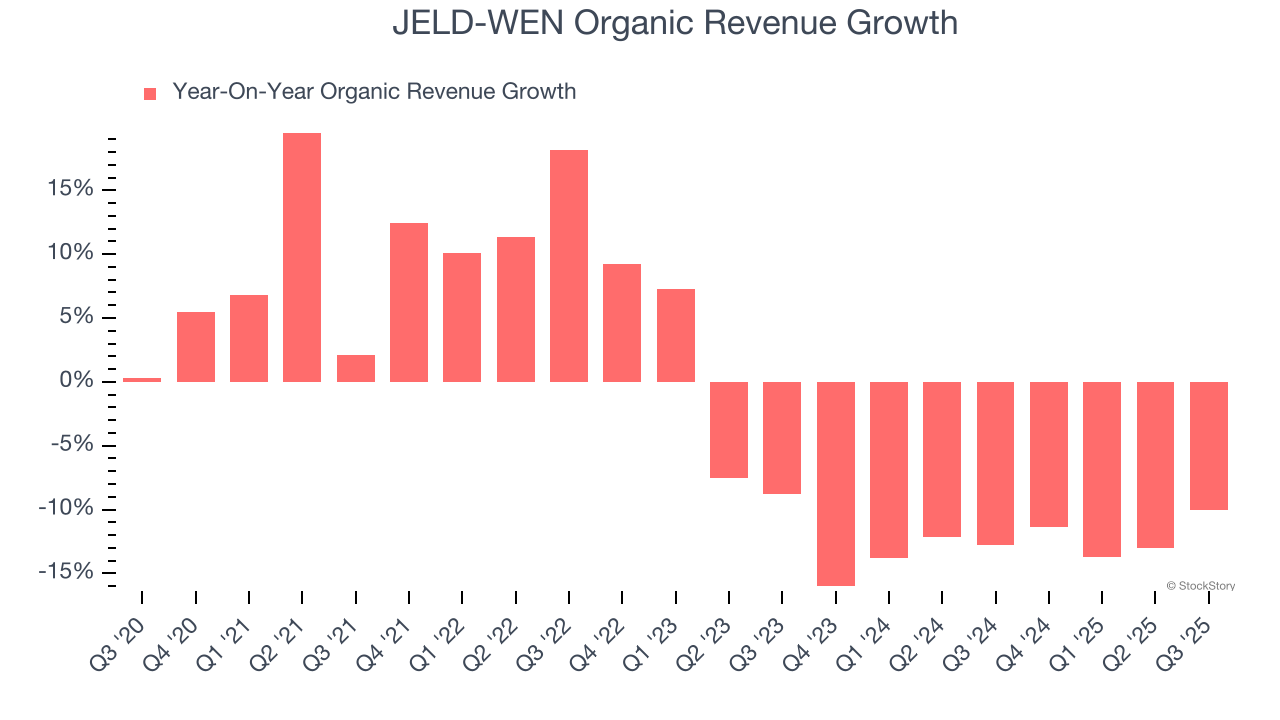

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, JELD-WEN’s organic revenue averaged 12.9% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, JELD-WEN missed Wall Street’s estimates and reported a rather uninspiring 13.4% year-on-year revenue decline, generating $809.5 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

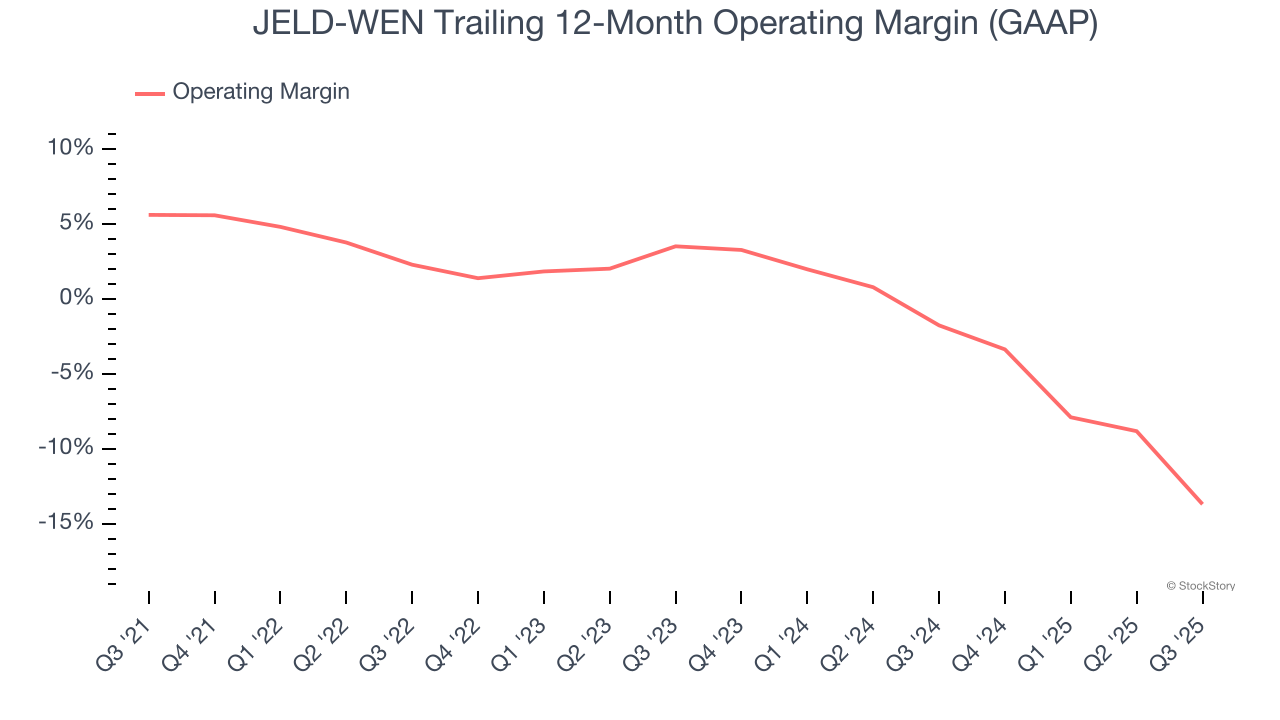

JELD-WEN was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, JELD-WEN’s operating margin decreased by 19.3 percentage points over the last five years. JELD-WEN’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q3, JELD-WEN generated an operating margin profit margin of negative 25%, down 19.4 percentage points year on year. Since JELD-WEN’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for JELD-WEN, its EPS declined by 18.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of JELD-WEN’s earnings can give us a better understanding of its performance. As we mentioned earlier, JELD-WEN’s operating margin declined by 19.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For JELD-WEN, its two-year annual EPS declines of 51.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, JELD-WEN reported adjusted EPS of negative $0.20, down from $0.32 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast JELD-WEN’s full-year EPS of negative $0.51 will flip to positive $0.34.

This was a bad quarter, with revenue and EBITDA missing expectations. Full-year revenue guidance was lowered and EBITDA guidance came in below Wall Street's estimates. Overall, this was a very weak quarter. The stock traded down 12.7% to $3.65 immediately following the results.

JELD-WEN’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| 9 min | |

| Aug-03 | |

| Aug-03 | |

| Jul-28 | |

| Jul-07 | |

| Jun-23 | |

| Jun-08 | |

| Jun-02 | |

| May-05 | |

| May-04 | |

| May-04 | |

| Apr-15 | |

| Apr-02 | |

| Feb-24 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite