|

|

|

|

|||||

|

|

|

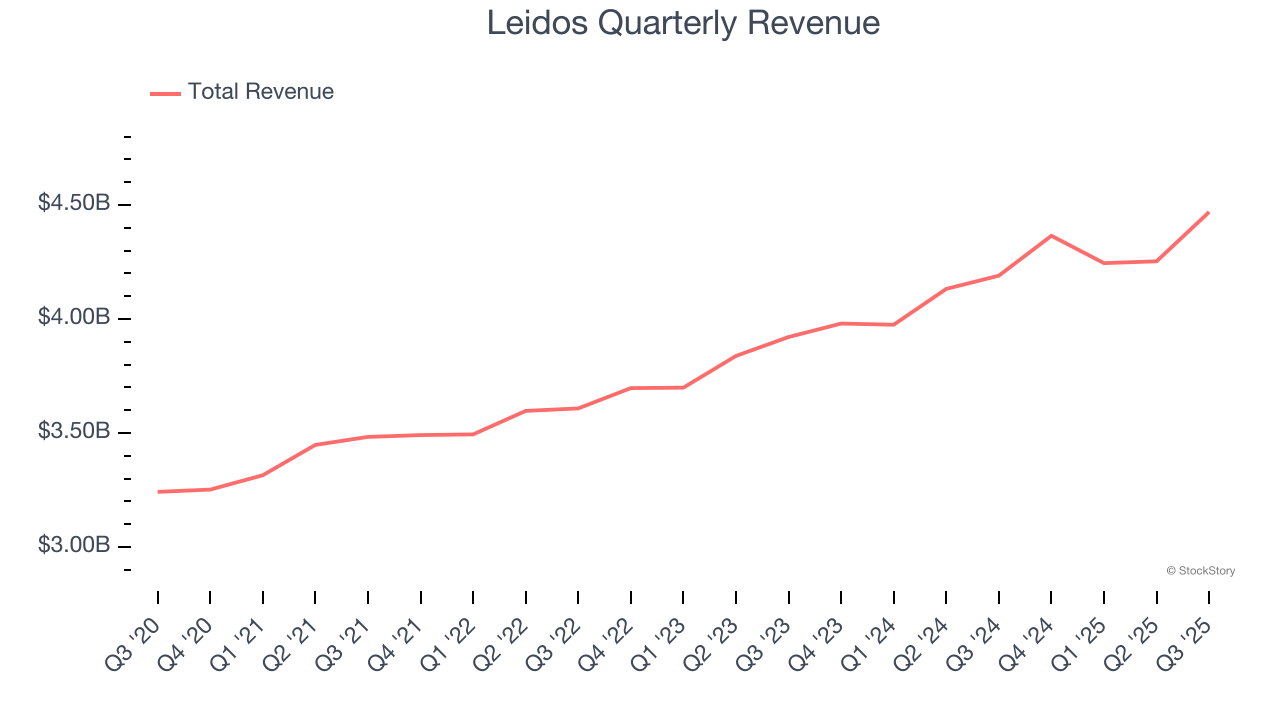

Defense contractor Leidos (NYSE:LDOS) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 6.7% year on year to $4.47 billion. The company expects the full year’s revenue to be around $17.13 billion, close to analysts’ estimates. Its non-GAAP profit of $3.05 per share was 12.3% above analysts’ consensus estimates.

Is now the time to buy Leidos? Find out by accessing our full research report, it’s free for active Edge members.

"Leidos continues to deliver exceptional results through the strength of our portfolio of mission-critical work as well as the innovation, agility, and discipline of our talented workforce," said Leidos Chief Executive Officer Tom Bell.

Formed through the split of IT services company SAIC, Leidos (NYSE:LDOS) offers technology and engineering solutions such as military training systems for the defense, civil, and health markets.

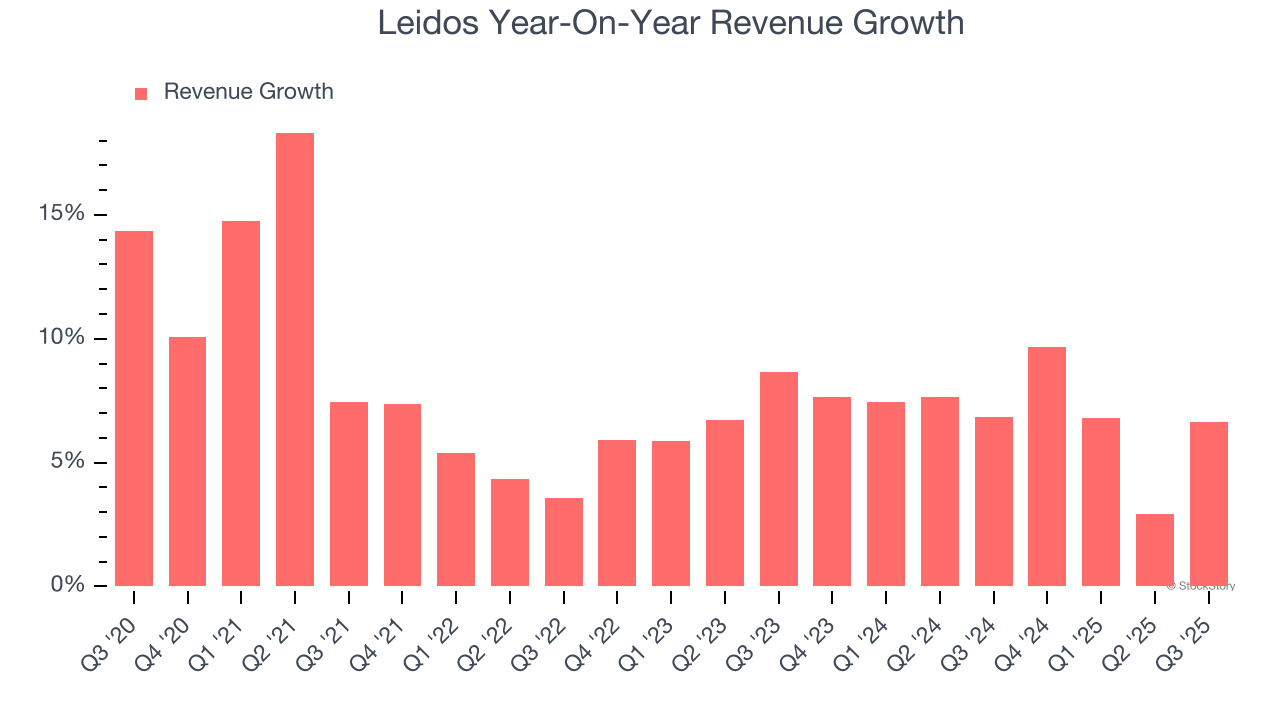

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Leidos grew its sales at a decent 7.6% compounded annual growth rate. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Leidos’s annualized revenue growth of 6.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

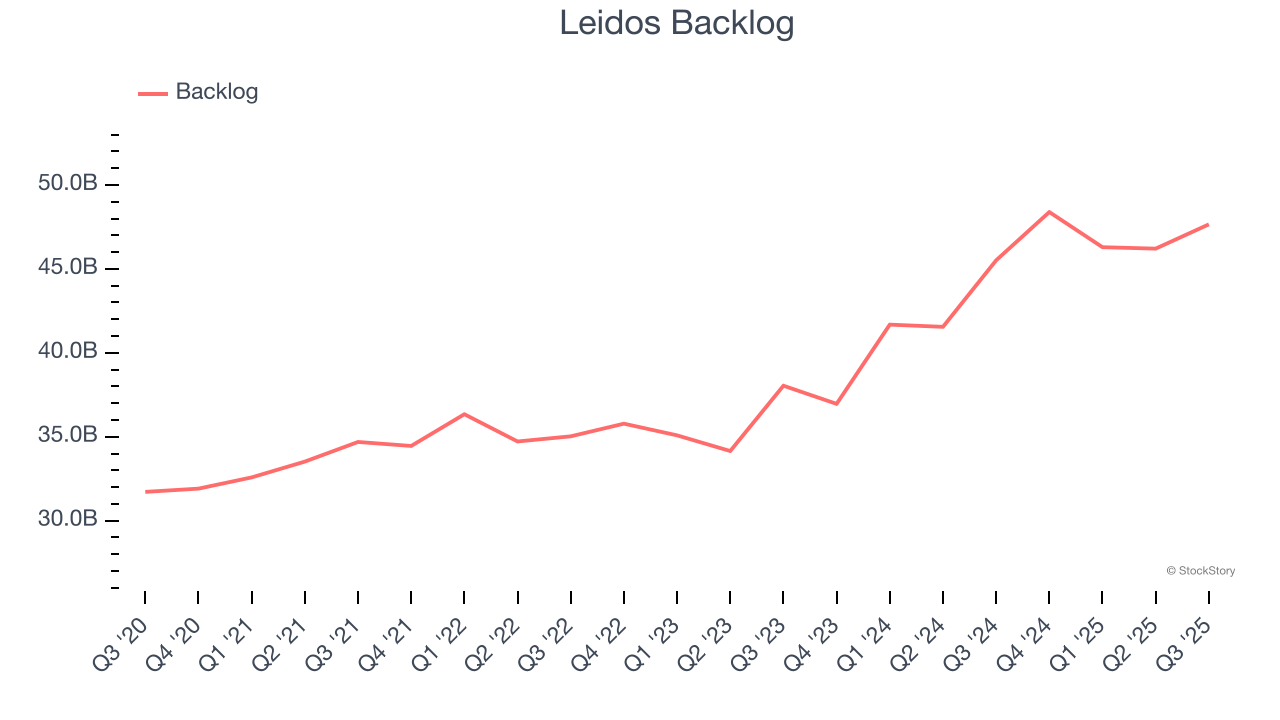

Leidos also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Leidos’s backlog reached $47.66 billion in the latest quarter and averaged 15.2% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Leidos’s products and services but raises concerns about capacity constraints.

This quarter, Leidos reported year-on-year revenue growth of 6.7%, and its $4.47 billion of revenue exceeded Wall Street’s estimates by 4.1%.

Looking ahead, sell-side analysts expect revenue to grow 2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Leidos has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.7%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Leidos’s operating margin rose by 3.1 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Leidos generated an operating margin profit margin of 12%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

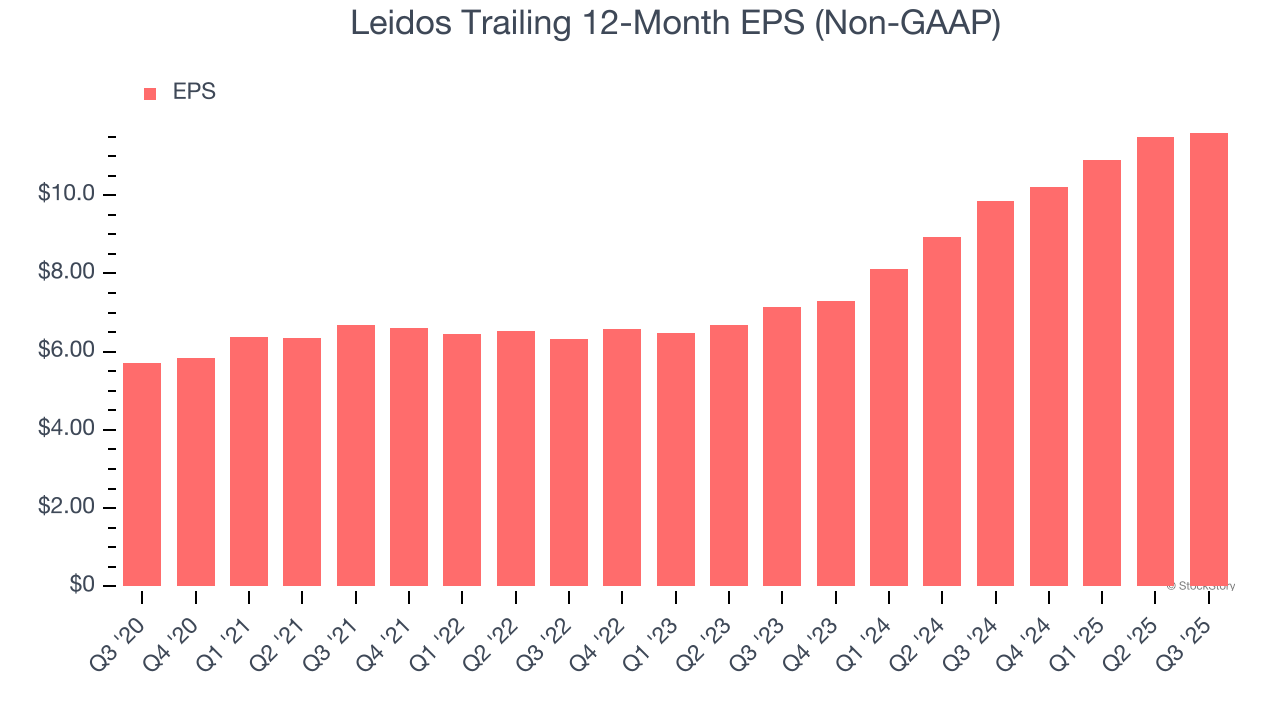

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Leidos’s EPS grew at a spectacular 15.2% compounded annual growth rate over the last five years, higher than its 7.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

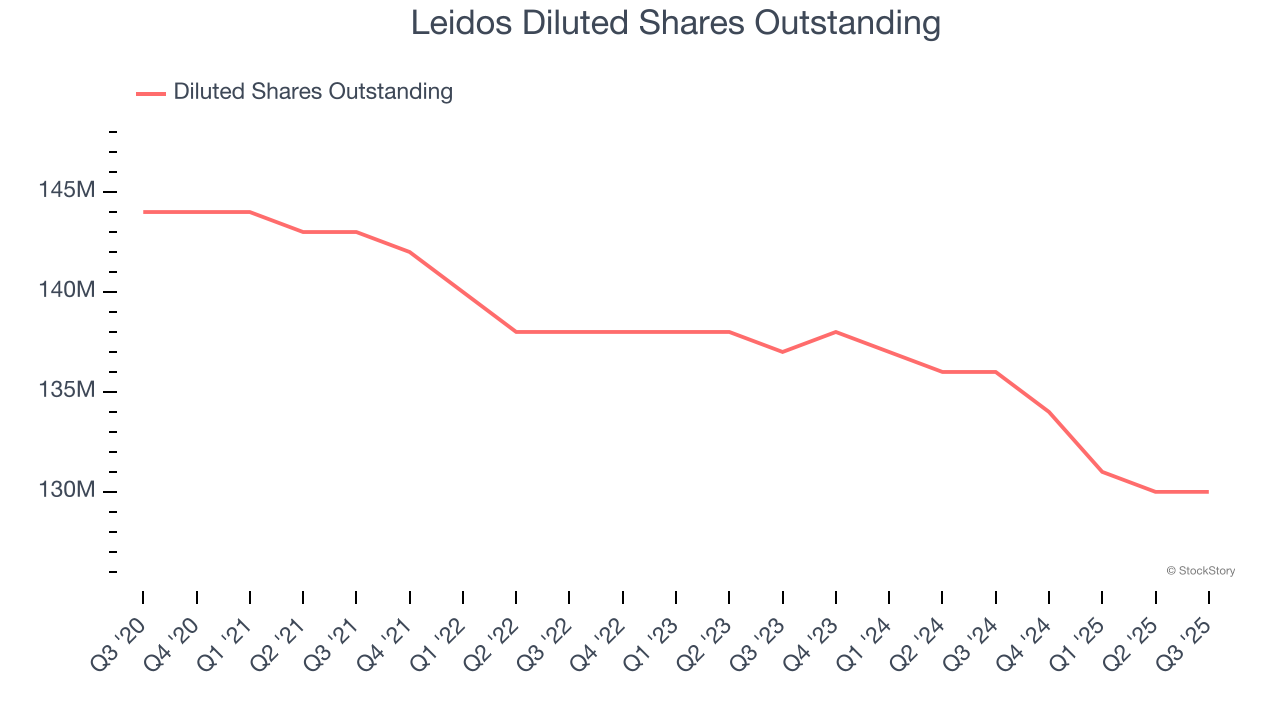

Diving into the nuances of Leidos’s earnings can give us a better understanding of its performance. As we mentioned earlier, Leidos’s operating margin was flat this quarter but expanded by 3.1 percentage points over the last five years. On top of that, its share count shrank by 9.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Leidos, its two-year annual EPS growth of 27.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, Leidos reported adjusted EPS of $3.05, up from $2.93 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Leidos’s full-year EPS of $11.60 to stay about the same.

We were impressed by how significantly Leidos blew past analysts’ backlog expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance was in line. Zooming out, we think this quarter featured some important positives. The stock traded up 2.7% to $198.29 immediately after reporting.

Leidos had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Apr-01 | |

| Mar-30 | |

| Mar-29 | |

| Mar-17 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-02 | |

| Mar-01 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite