|

|

|

|

|||||

|

|

|

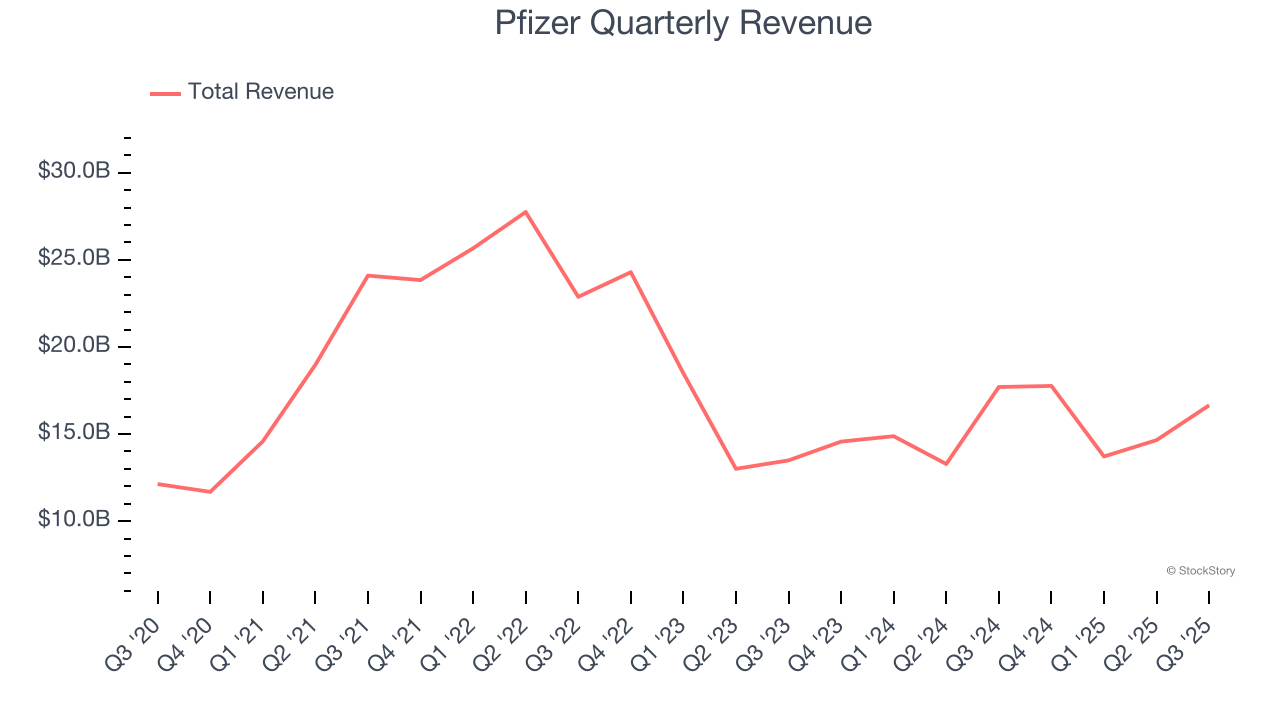

Global pharmaceutical company Pfizer (NYSE:PFE) met Wall Streets revenue expectations in Q3 CY2025, but sales fell by 5.9% year on year to $16.65 billion. On the other hand, the company’s full-year revenue guidance of $62.5 billion at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP profit of $0.87 per share was 37% above analysts’ consensus estimates.

Is now the time to buy Pfizer? Find out by accessing our full research report, it’s free for active Edge members.

With roots dating back to 1849 when two German immigrants opened a fine chemicals business in Brooklyn, Pfizer (NYSE:PFE) is a global biopharmaceutical company that discovers, develops, manufactures, and sells medicines and vaccines for a wide range of diseases and conditions.

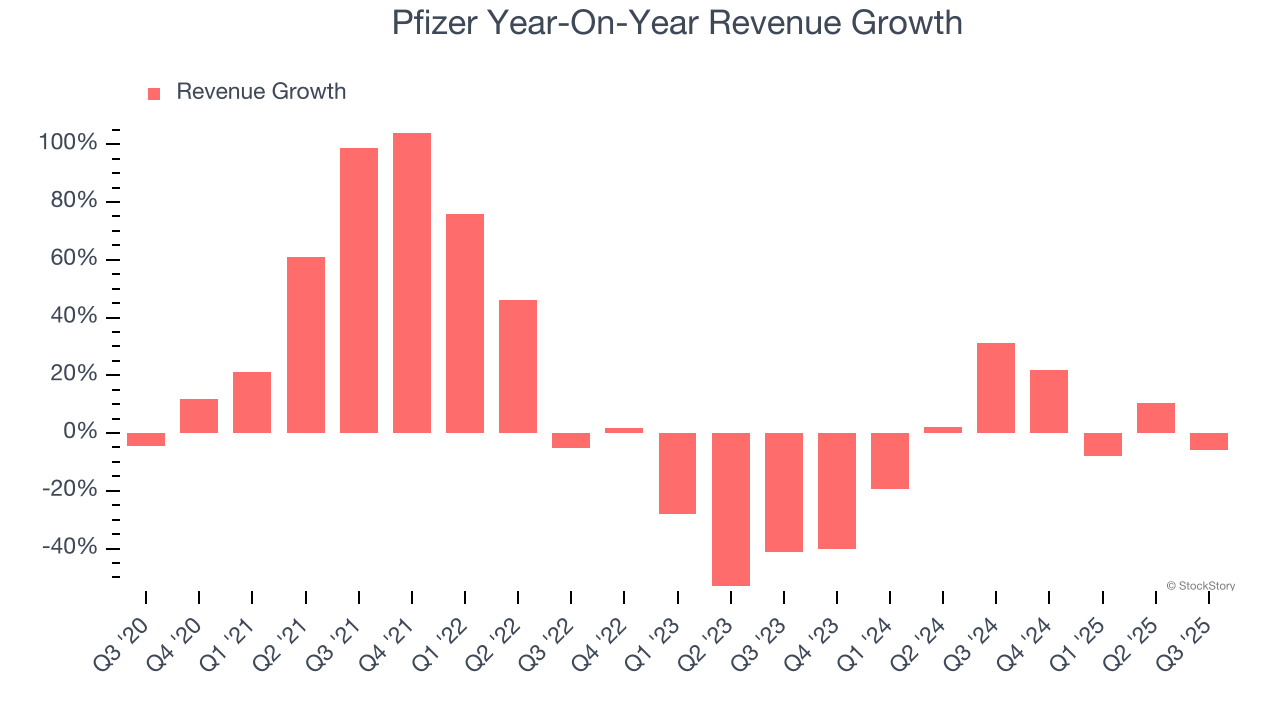

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Pfizer’s 6.2% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the healthcare sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Pfizer’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 4.8% annually.

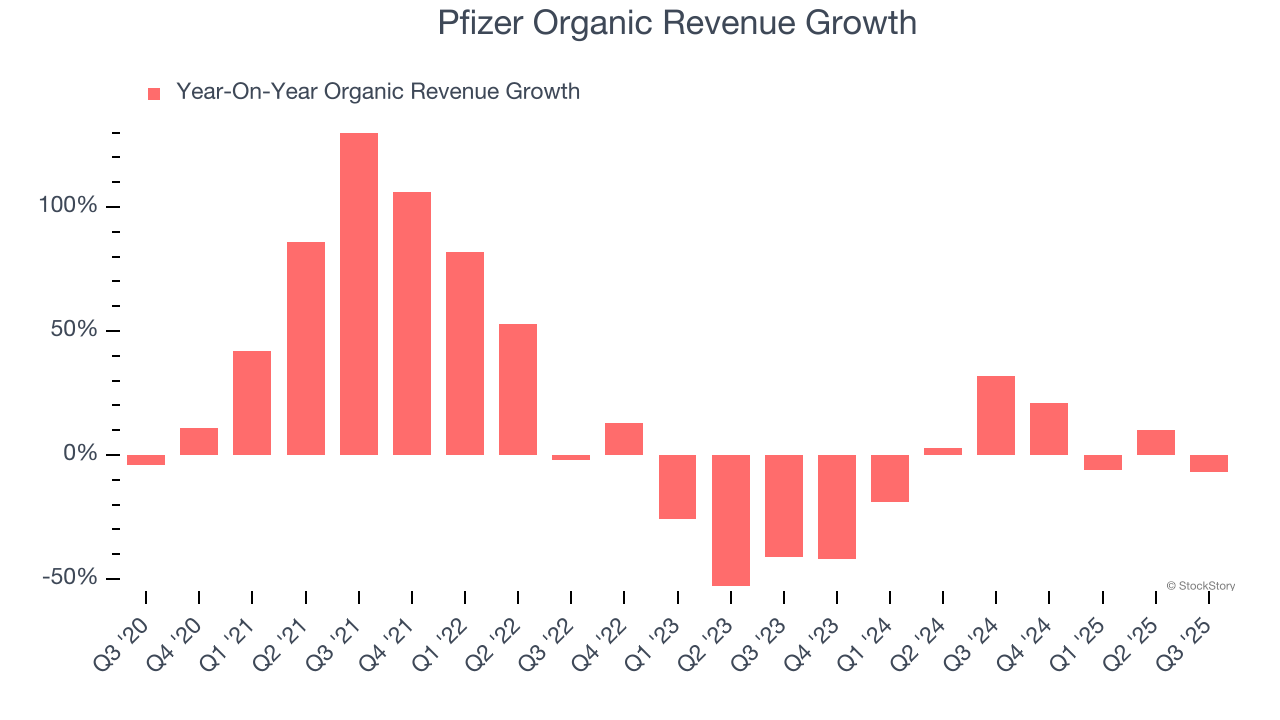

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Pfizer’s organic revenue was flat. Because this number is better than its two-year revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Pfizer reported a rather uninspiring 5.9% year-on-year revenue decline to $16.65 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 2% over the next 12 months. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

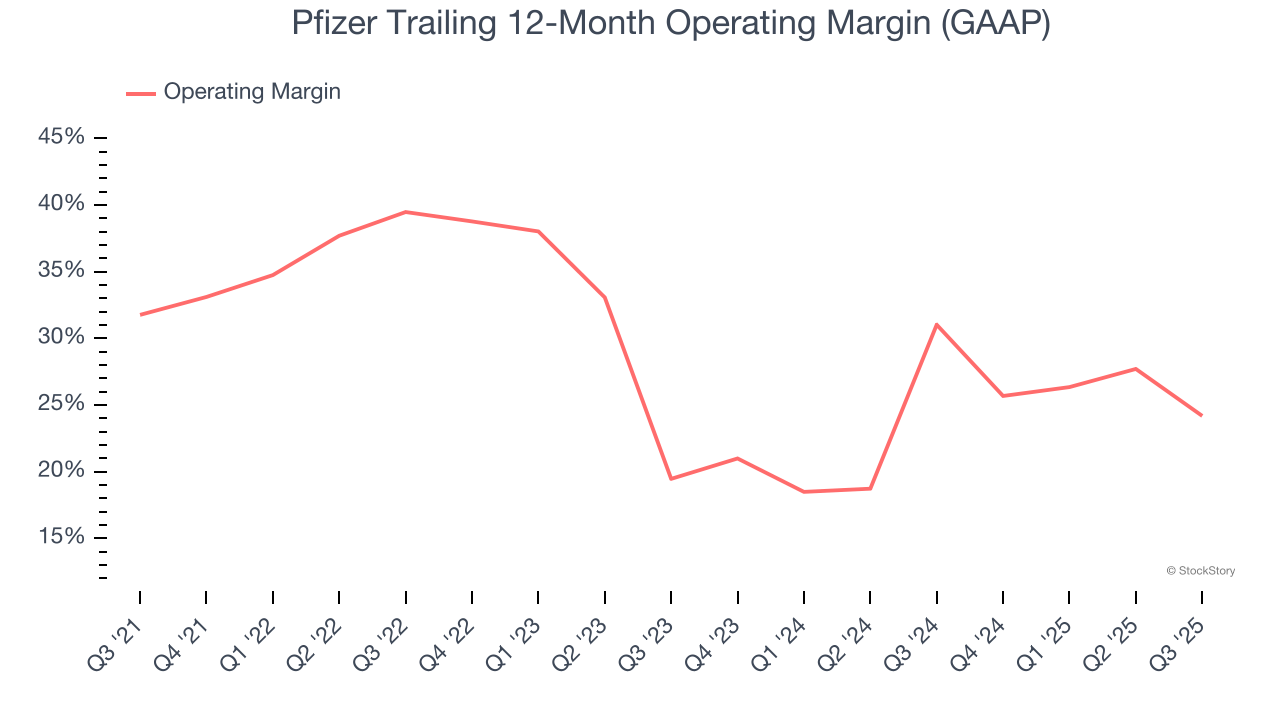

Pfizer has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average operating margin of 30.1%.

Looking at the trend in its profitability, Pfizer’s operating margin decreased by 7.6 percentage points over the last five years, but it rose by 4.7 percentage points on a two-year basis. Still, shareholders will want to see Pfizer become more profitable in the future.

This quarter, Pfizer generated an operating margin profit margin of 20%, down 13 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

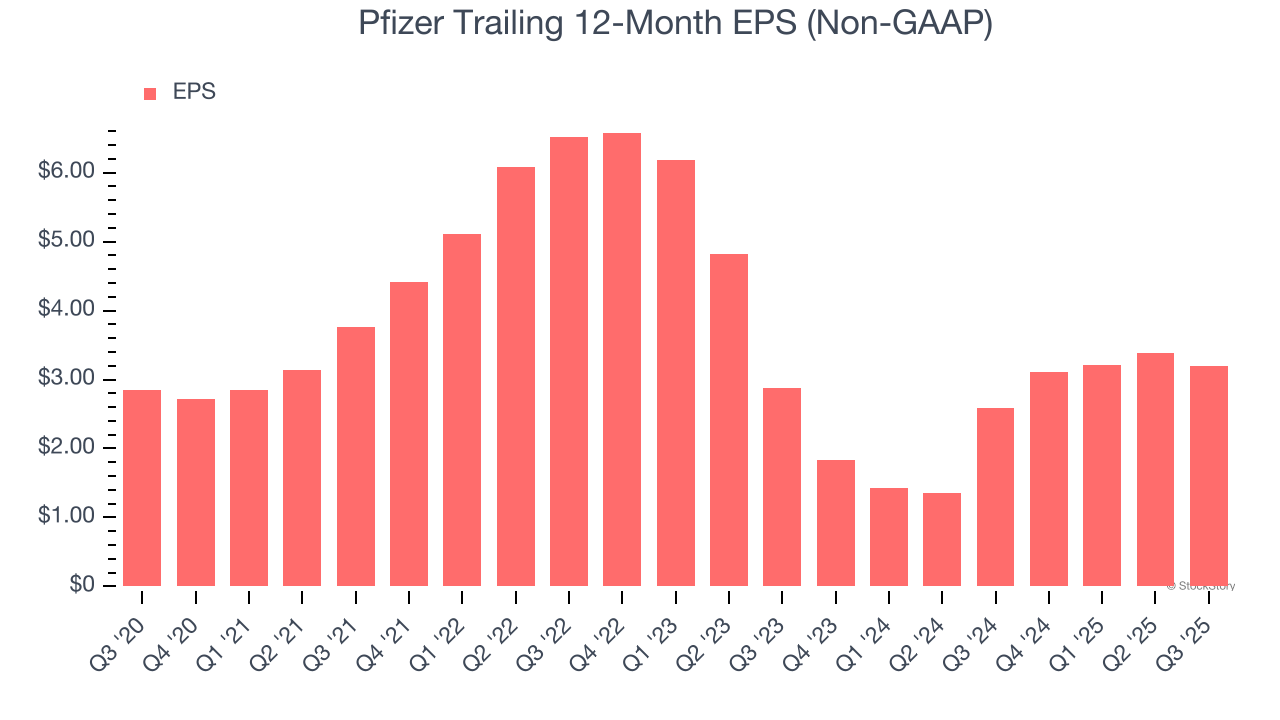

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Pfizer’s EPS grew at an unimpressive 2.3% compounded annual growth rate over the last five years, lower than its 6.2% annualized revenue growth. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as taxes affected its ultimate earnings.

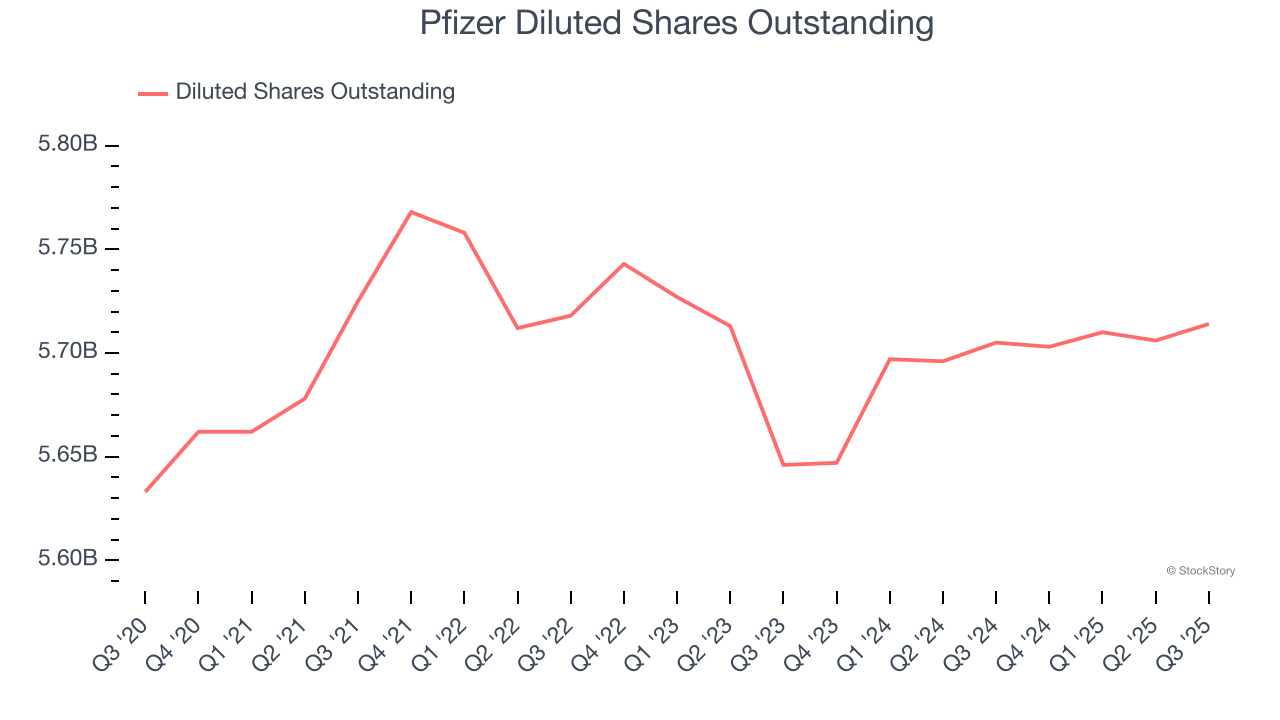

Diving into the nuances of Pfizer’s earnings can give us a better understanding of its performance. As we mentioned earlier, Pfizer’s operating margin declined by 7.6 percentage points over the last five years. Its share count also grew by 1.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q3, Pfizer reported adjusted EPS of $0.87, down from $1.06 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Pfizer’s full-year EPS of $3.20 to shrink by 3%.

It was good to see Pfizer beat analysts’ EPS expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. On the other hand, its organic revenue missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $24.50 immediately after reporting.

Big picture, is Pfizer a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| 2 hours | |

| 3 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite