|

|

|

|

|||||

|

|

|

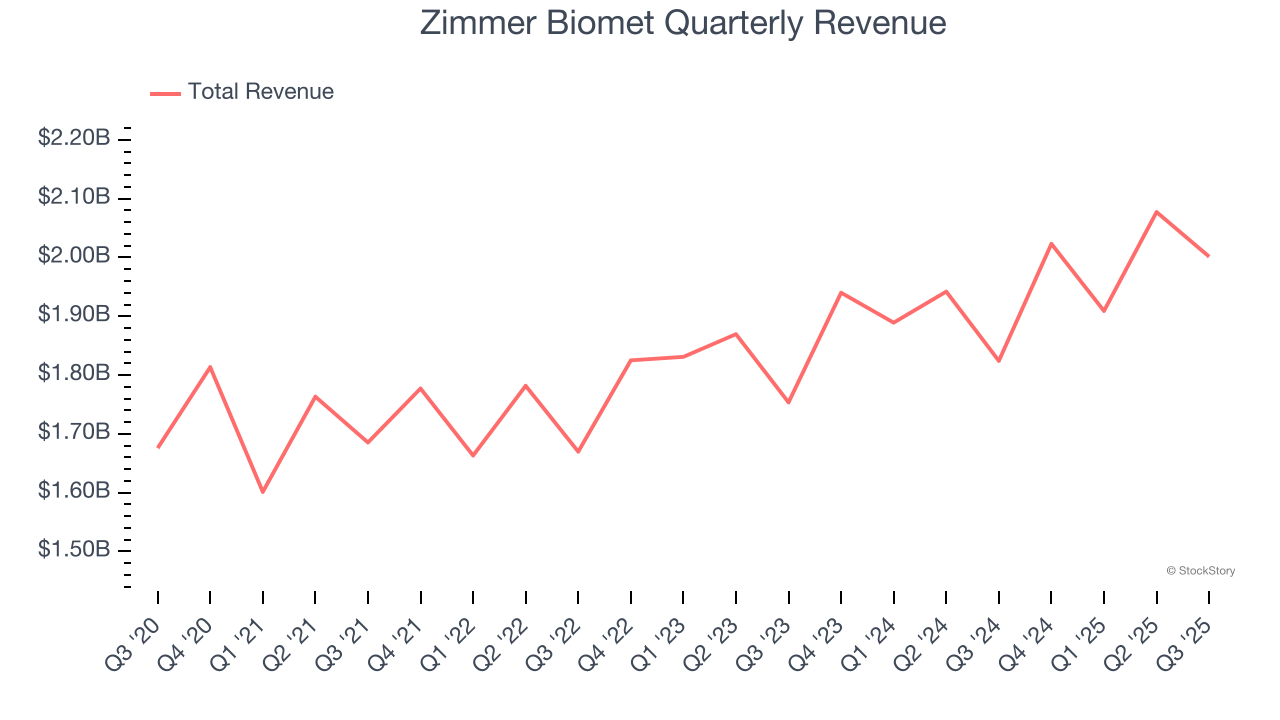

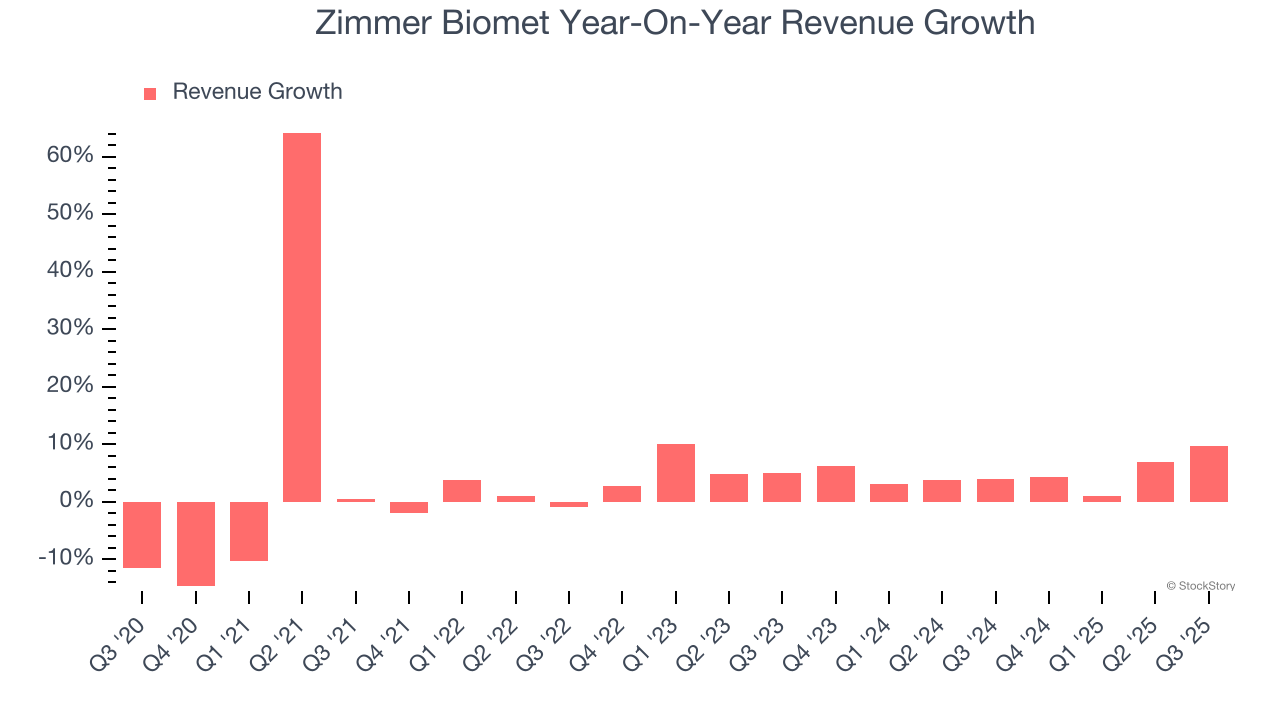

Medical device company Zimmer Biomet (NYSE:ZBH) met Wall Streets revenue expectations in Q3 CY2025, with sales up 9.7% year on year to $2.00 billion. Its non-GAAP profit of $1.90 per share was 2.1% above analysts’ consensus estimates.

Is now the time to buy Zimmer Biomet? Find out by accessing our full research report, it’s free for active Edge members.

"Our third quarter performance was anchored by 5.6% organic revenue growth in our critical U.S. business, driven by accelerated adoption of our key new products referred to as the 'Magnificent Seven,'" said Ivan Tornos, Chairman, President and CEO of Zimmer Biomet.

With a history dating back to 1927 and a presence in over 100 countries worldwide, Zimmer Biomet (NYSE:ZBH) designs and manufactures orthopedic products including knee and hip replacements, surgical tools, and robotic technologies for joint reconstruction and spine surgeries.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Zimmer Biomet grew its sales at a tepid 3.8% compounded annual growth rate. This was below our standard for the healthcare sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Zimmer Biomet’s annualized revenue growth of 4.9% over the last two years is above its five-year trend, but we were still disappointed by the results.

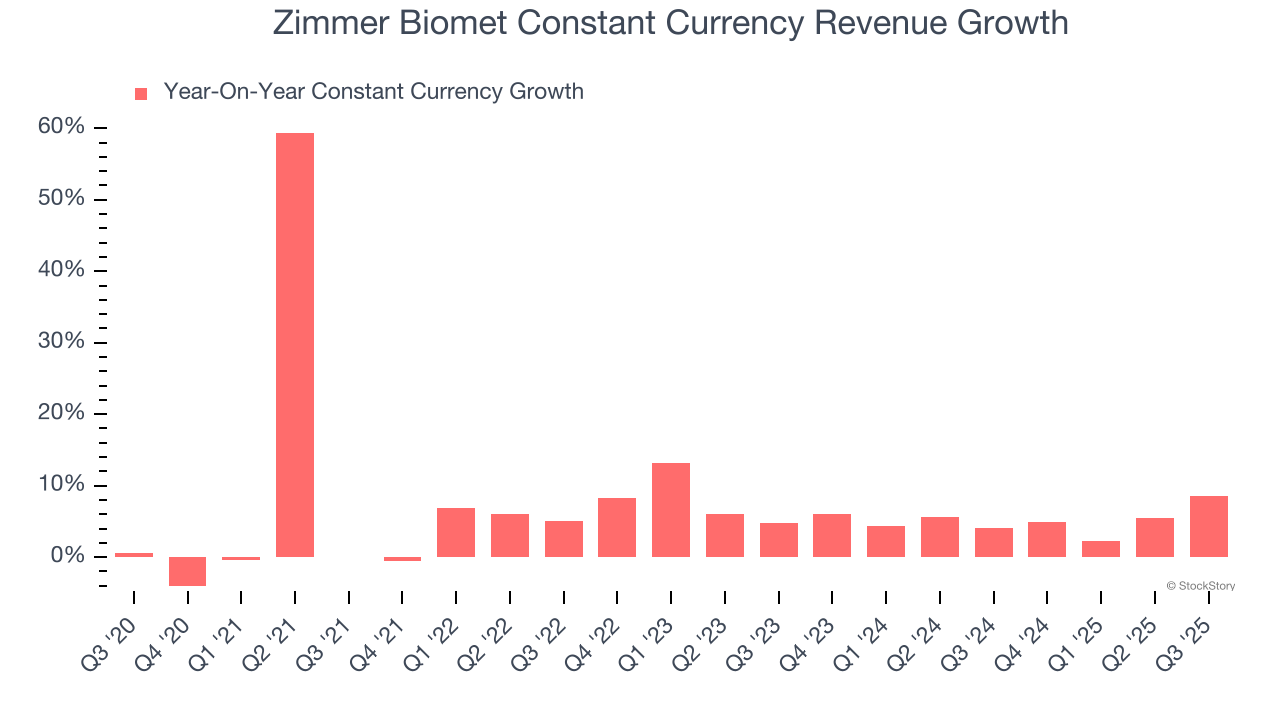

Zimmer Biomet also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.2% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Zimmer Biomet has properly hedged its foreign currency exposure.

This quarter, Zimmer Biomet grew its revenue by 9.7% year on year, and its $2.00 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.4% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will catalyze better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

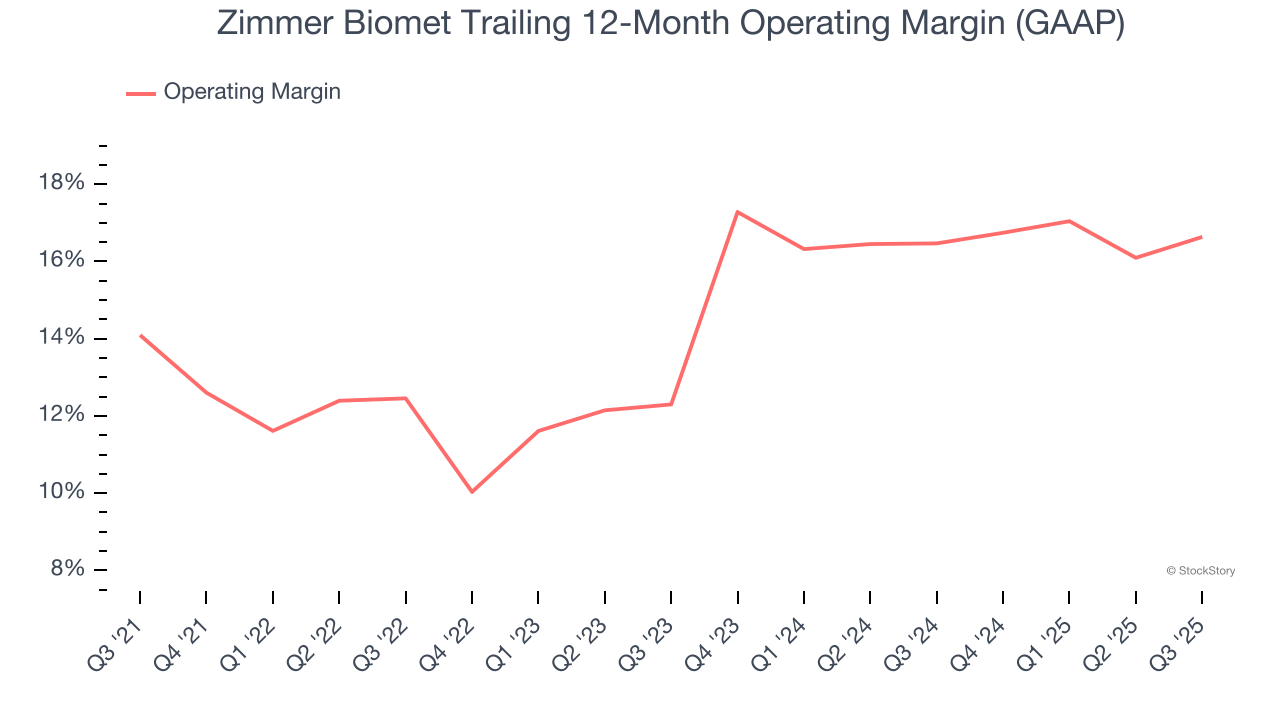

Zimmer Biomet has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14.5%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Zimmer Biomet’s operating margin rose by 2.5 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 4.3 percentage points on a two-year basis.

In Q3, Zimmer Biomet generated an operating margin profit margin of 17.6%, up 2.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

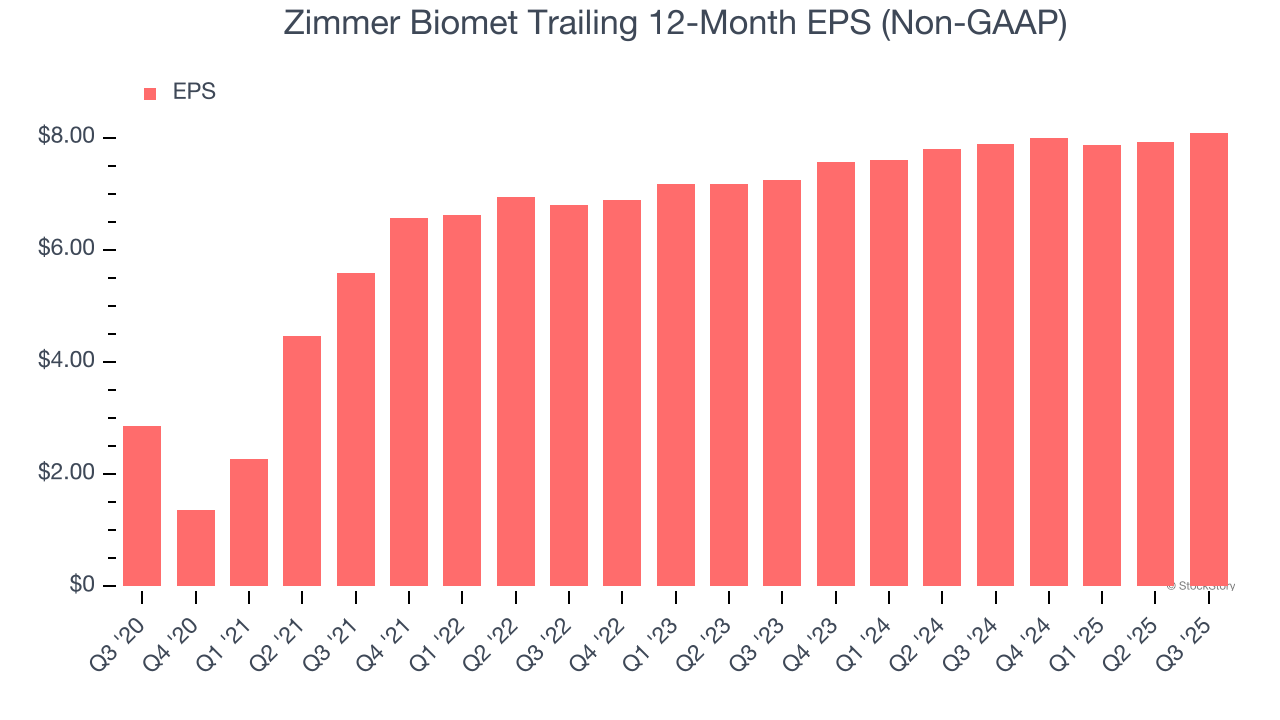

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Zimmer Biomet’s EPS grew at an astounding 23.2% compounded annual growth rate over the last five years, higher than its 3.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

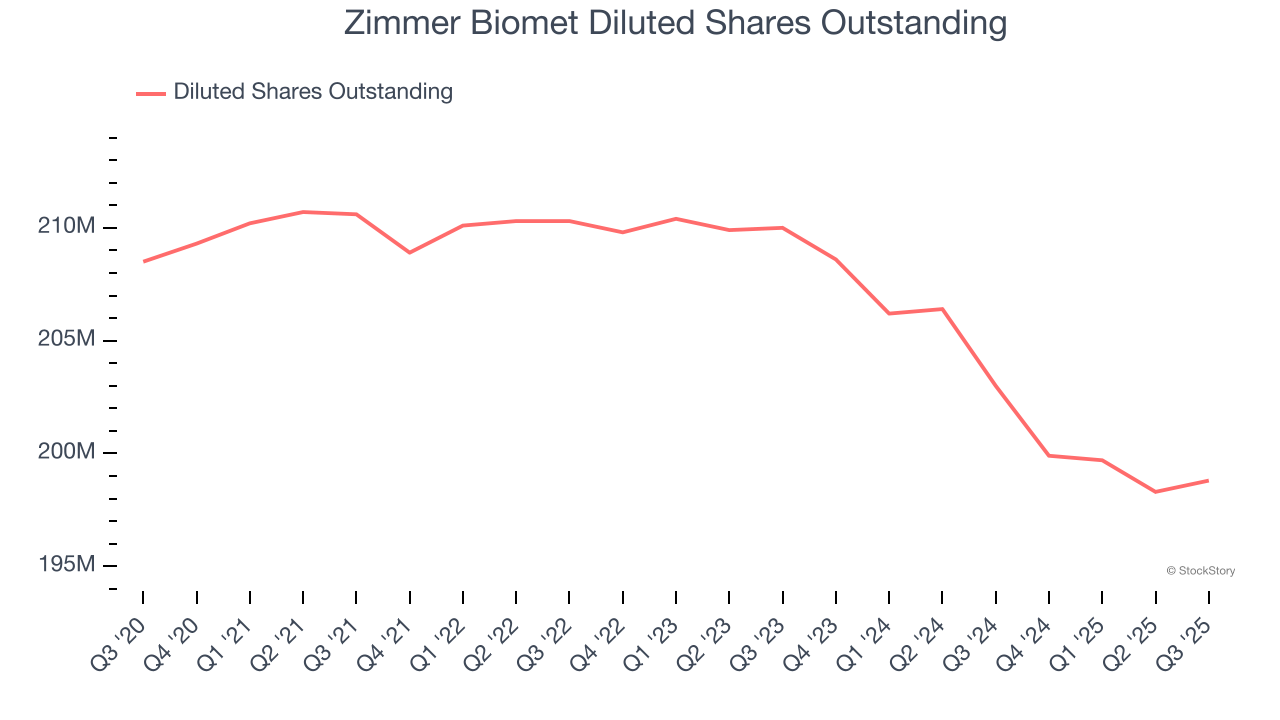

We can take a deeper look into Zimmer Biomet’s earnings to better understand the drivers of its performance. As we mentioned earlier, Zimmer Biomet’s operating margin expanded by 2.5 percentage points over the last five years. On top of that, its share count shrank by 4.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q3, Zimmer Biomet reported adjusted EPS of $1.90, up from $1.74 in the same quarter last year. This print beat analysts’ estimates by 2.1%. Over the next 12 months, Wall Street expects Zimmer Biomet’s full-year EPS of $8.09 to grow 4.7%.

It was good to see Zimmer Biomet narrowly top analysts’ full-year EPS guidance expectations this quarter. On the other hand, its revenue was in line. Overall, this was a mixed quarter. The stock traded down 8.8% to $94.10 immediately following the results.

Big picture, is Zimmer Biomet a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jun-02 | |

| May-22 | |

| May-12 | |

| May-12 | |

| May-06 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-24 | |

| Apr-13 | |

| Apr-09 | |

| Apr-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite