|

|

|

|

|||||

|

|

|

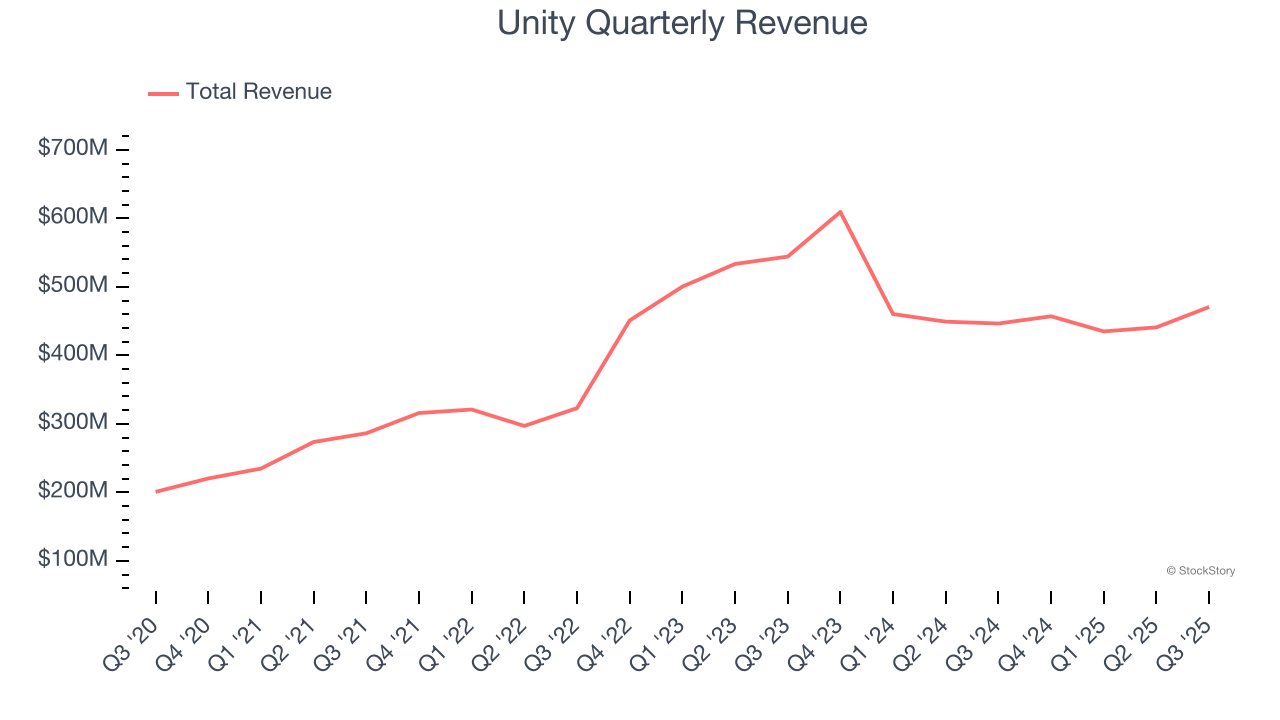

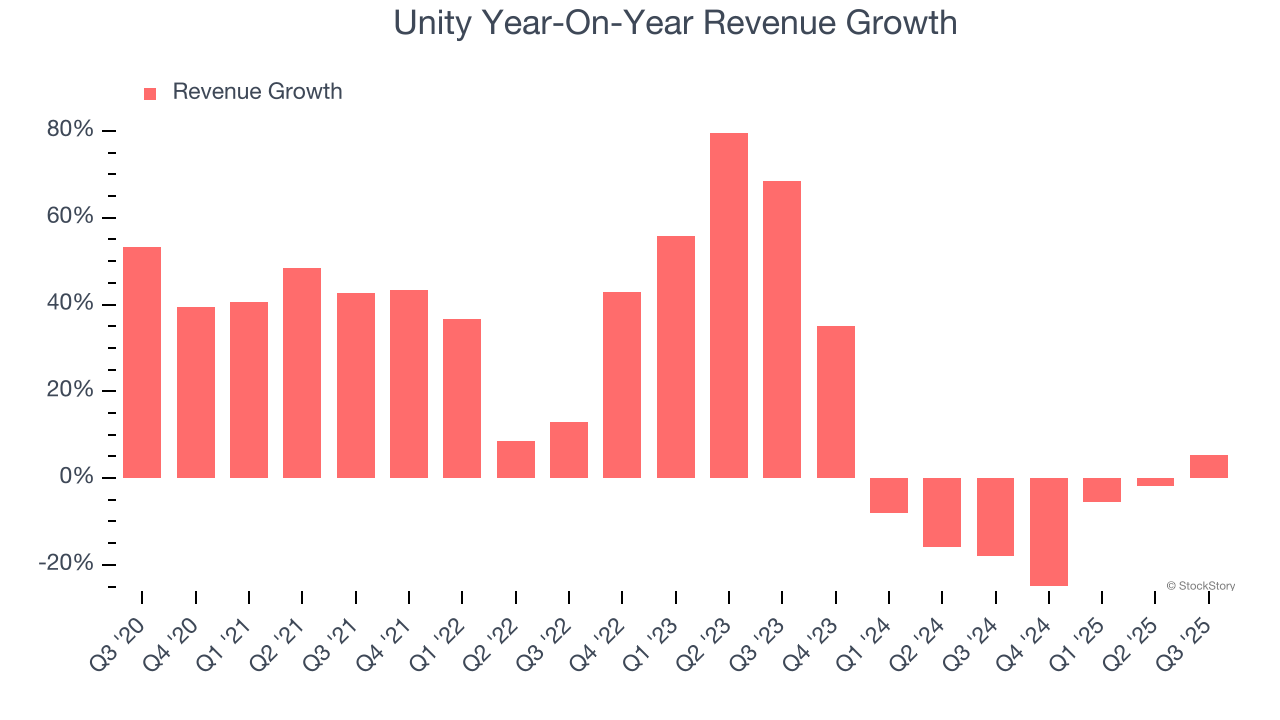

Interactive software platform Unity (NYSE:U) announced better-than-expected revenue in Q3 CY2025, with sales up 5.4% year on year to $470.6 million. Guidance for next quarter’s revenue was better than expected at $485 million at the midpoint, 1.2% above analysts’ estimates. Its non-GAAP profit of $0.20 per share was 19.6% above analysts’ consensus estimates.

Is now the time to buy Unity? Find out by accessing our full research report, it’s free for active Edge members.

Powering over half of the world's mobile games and expanding into industries from automotive to architecture, Unity (NYSE:U) provides software tools and services that allow developers to create, run, and monetize interactive 2D and 3D content across multiple platforms.

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Unity’s 20.5% annualized revenue growth over the last five years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Unity’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 5.7% over the last two years.

This quarter, Unity reported year-on-year revenue growth of 5.4%, and its $470.6 million of revenue exceeded Wall Street’s estimates by 4.6%. Company management is currently guiding for a 6.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.3% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Unity is efficient at acquiring new customers, and its CAC payback period checked in at 42 months this quarter. The company’s relatively fast recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

We were impressed by how significantly Unity blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EBITDA guidance for next quarter missed. Overall, this print had some key positives. The stock traded up 9.9% to $39.41 immediately after reporting.

Unity had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Apr-02 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-27 | |

| Mar-26 | |

| Mar-13 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite