|

|

|

|

|||||

|

|

|

Vistra Corp. VST is expected to deliver an improvement in the top line and a decline in the bottom line when it reports third-quarter 2025 results on Nov. 6, before market open.

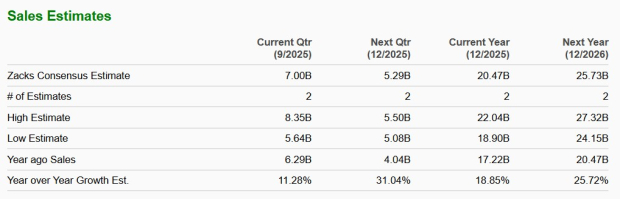

The Zacks Consensus Estimate for VST’s third-quarter revenues is pegged at $7 billion, indicating an increase of 11.28% from the year-ago reported figure.

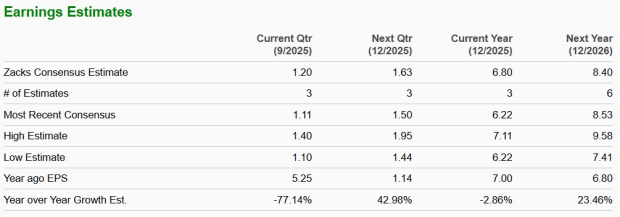

The Zacks Consensus Estimate for VST’s third-quarter earnings is pegged at $1.20 per share, indicating a 77.14% decline from the year-ago reported figure.

Vistra’s earnings surpassed expectations in two of the last four quarters, reported on par once and missed once, with the average surprise being 69.75%.

Our model does not conclusively predict a likely earnings beat for Vistra this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you can see below.

Vistra Corp. price-eps-surprise | Vistra Corp. Quote

You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Earnings ESP: Vistra has an Earnings ESP of 0.00%.

Zacks Rank: VST currently carries a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Some companies in the same sector with the right combination of the two factors for an earnings beat this season are Duke Energy Corporation DUK, having an Earnings ESP of +1.63% and a Zacks Rank #2, and Alliant Energy Corporation LNT, having an Earnings ESP of +0.43% and a Zacks Rank of 3.

Vistra's third-quarter performance is likely to have benefited from increasing demand for clean electricity across its service area. This surge in demand has been largely fueled by the rapid growth of large U.S. data centers, continued reshoring of industrial operations in the United States and the ongoing electrification of the Permian Basin. With a diversified generation portfolio that includes a high-quality nuclear fleet, Vistra is well-positioned to capitalize on this accelerating load growth and derive meaningful benefits.

The company’s share repurchase program has enhanced shareholder value and supported earnings per share growth, contributing positively to its third-quarter performance. Between November 2021 and Aug. 1, 2025, VST executed $5.4 billion in share buybacks, reducing outstanding shares and boosting EPS. Management plans to maintain this strategy, targeting at least $1.4 billion in additional repurchases between 2025 and 2026, which is expected to further strengthen earnings going forward.

VST’s third-quarter earnings are likely to have benefited from its integrated business model. In the evolving market conditions, Vistra is focused on providing reliable and affordable electricity to customers, which has been boosting its revenues.

Vistra utilizes a hedging program to reduce the impact of market changes and price fluctuations, and 100% of its 2025 generation volume is hedged. This extensive hedging has helped to secure its third-quarter generation volumes.

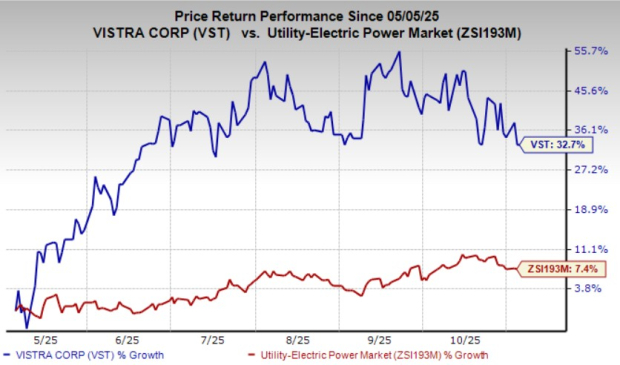

VST’s shares have gained 32.7% in the past six months compared with the industry’s rise of 7.4%.

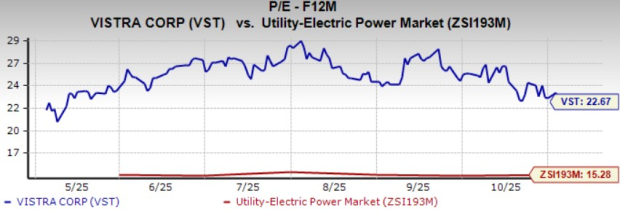

Vistra is currently valued at a premium compared with its industry on a forward 12-month P/E basis.

Vistra is growing its generation capacity through a combination of organic initiatives and strategic acquisitions. Its integrated business model provides a significant competitive advantage compared with non-integrated counterparts.

Vistra’s disciplined capital allocation strategy remains central to the sustained value creation, allowing it to strengthen financial flexibility while enhancing shareholder returns. By prioritizing high-return projects and maintaining prudent leverage, Vistra ensures consistent cash flow generation and efficient use of capital.

However, operating nuclear power plants involves considerable risks that could materially impact the company’s revenues and financial performance. Additionally, Vistra may lack adequate insurance coverage to fully offset these risks and potential liabilities.

Vistra operates in a region experiencing growing demand for clean electricity. The company is expanding its clean energy generation capacity through both acquisitions and organic growth to meet this demand and capitalize on the opportunity. Vistra’s stable hedging strategy and an expanding residential customer base further strengthen its position.

However, with the stock currently trading at a premium, it may be prudent for new investors to hold off and wait for a more attractive entry point.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-27 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite