|

|

|

|

|||||

|

|

|

Perrigo PRGO reported adjusted earnings of 80 cents per share in the third quarter of 2025, beating the Zacks Consensus Estimate of 75 cents. The reported figure fell 1.2% year over year, attributable to lower sales volume in the quarter.

Net sales declined 4.1% year over year to $1.04 billion, missing the Zacks Consensus Estimate of $1.10 billion. The downside was due to the soft sales performance of its infant formula and oral care businesses, as well as the loss of sales stemming from exited businesses and product lines, partially offset by favorable currency movements.

In the quarter, sales dropped 1.3% year over year on account of exited businesses and product lines, but benefited 1.6% from favorable currency movements. At constant currency (excluding foreign currency translation), sales fell 5.7%. Organic net sales (excluding the effects of acquisitions and divestitures, and the impacts of currency) declined 4.4%.

Perrigo reports its results under the following segments: Consumer Self Care Americas (“CSCA”) and Consumer Self Care International (“CSCI”).

CSCA: The segment’s net sales in the quarter came in at $646 million, down 3.8% year over year. Though sales grew across the Upper Respiratory, Skin Care and Women’s Health categories, more than offset by lower sales in the Infant Formula and Oral Care businesses. Organic net sales also declined 3.8%. The reported segment sales missed the Zacks Consensus Estimate of $664 million and our model estimate of $676 million.

CSCI: The segment reported net sales of $398 million, down 4.5% from the year-ago period due to the soft sales performances of its Upper Respiratory, VMS (Vitamins, Minerals and Supplements), and Women's Health categories. This decline was partially offset by favorable currency movements in the quarter. At constant-currency rates, sales moved down 8.7% year over year. Organically, sales declined 5.3%. CSCI sales missed the Zacks Consensus Estimate and our model estimate of $432 million and $429 million, respectively.

Perrigo lowered its financial guidance for total sales this year due to infant formula industry dynamics and challenging market consumption trends. As a result, the company expects sales to decline 2.5-3% against the previously issued guidance of growth in sales toward the lower end of 0-3%. This revision was likely the reason for the 12% decline in Perrigo’s stock price during pre-market trading today.

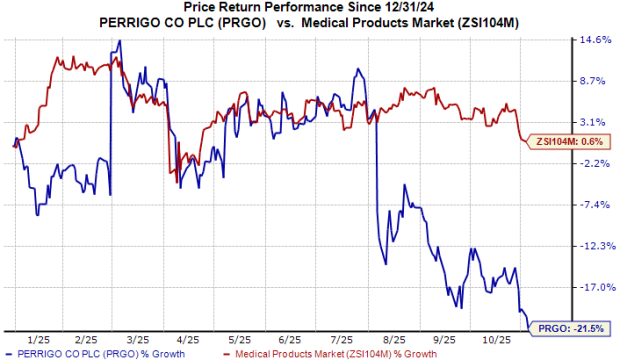

Year to date, shares of Perrigo have lost more than 21% against the industry’s 1% growth.

Perrigo also lowered some of its other 2025 financial targets, including an adjusted EPS of $2.70-$2.80 (previously: $2.90-$3.10) and an adjusted gross margin of 39% (previously: 40%). The company reiterated its guidance for the adjusted operating margin near 15%.

In a separate press release, the company announced it is initiating a strategic review of its infant formula business — a unit expected to generate $360 million in net sales in 2025, yet representing less than 10% of its total annual net sales. This review, which is part of Perrigo’s “Three-S” (Stabilize, Streamline, Strengthen) plan, aims to evaluate a full range of alternatives to maximize shareholder value. The company has not set any specific timeline for completing this process.

Perrigo currently has a Zacks Rank #4 (Sell).

Perrigo Company plc price | Perrigo Company plc Quote

Some better-ranked stocks from the sector are Alkermes ALKS, CorMedix CRMD and ANI Pharmaceuticals ANIP. ALKS and CRMD sport a Zacks Rank #1 (Strong Buy) at present, and ANIP carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

EPS estimates for Alkermes’ 2025 have increased from $1.78 to $1.96, while those for 2026 have risen from $1.69 to $1.77 in the past 60 days. ALKS stock has gained 6% year to date.

Alkermes’ earnings beat estimates in three of the trailing four quarters and missed the mark on one occasion, delivering an average negative surprise of 4.58%.

In the past 60 days, estimates for CorMedix’s earnings per share (EPS) have increased from $1.24 to $1.85 for 2025. During the same time, EPS estimates for 2026 have increased from $2.09 to $2.49. Year to date, shares of CRMD have rallied 41%.

CorMedix’s earnings beat estimates in the trailing four quarters, the average surprise being 34.85%.

In the past 60 days, estimates for ANI Pharmaceuticals’ EPS have increased from $7.25 to $7.29 for 2025. In the same time, EPS estimates for 2026 have increased from $7.74 to $7.81. Year to date, shares of ANIP have surged 71%.

ANI Pharmaceuticals' earnings beat estimates in the trailing four quarters, the average surprise being 22.66%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-24 | |

| Jul-22 | |

| Jul-16 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jun-30 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite