|

|

|

|

|||||

|

|

|

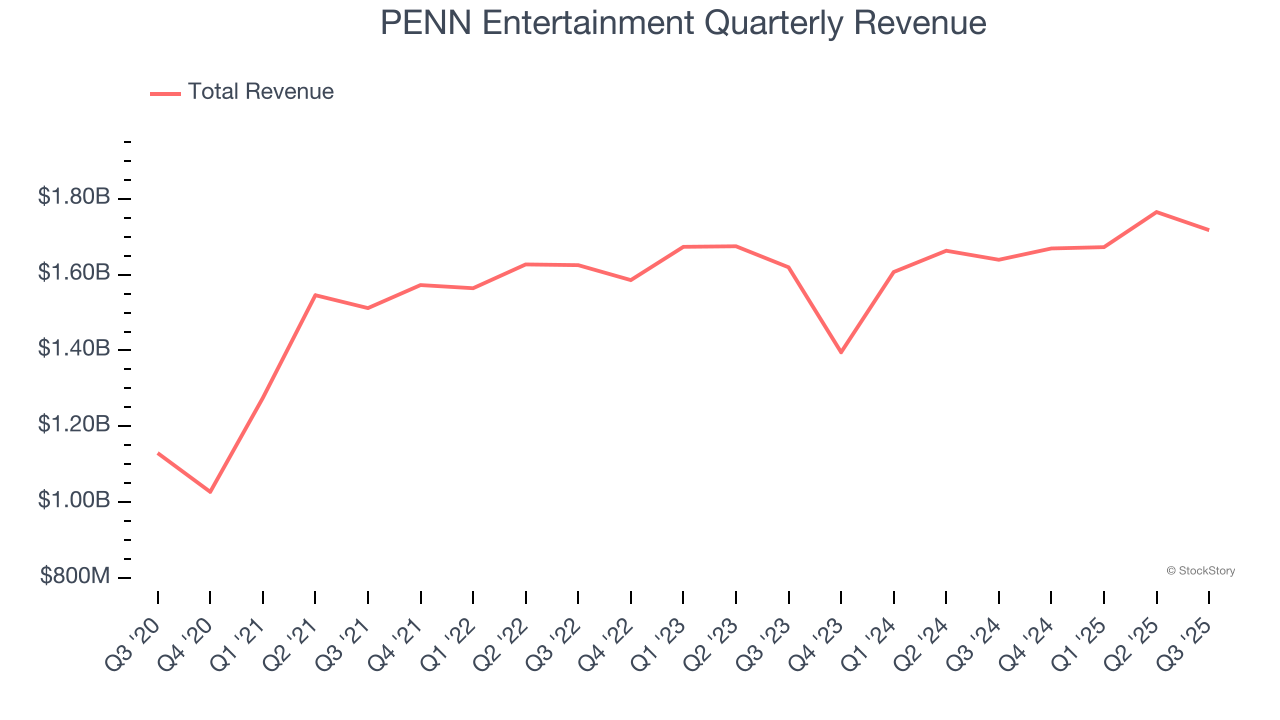

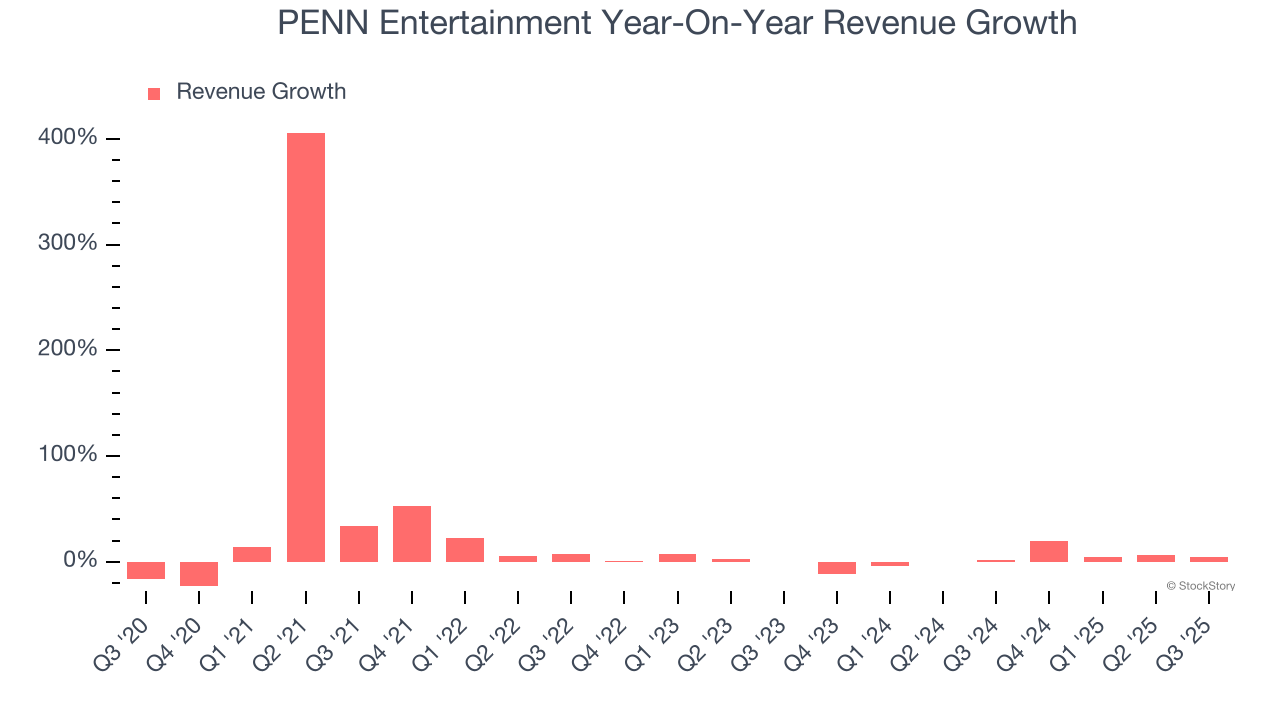

Casino, sports betting and entertainment operator PENN Entertainment (NASDAQ:PENN) fell short of the markets revenue expectations in Q3 CY2025 as sales rose 4.8% year on year to $1.72 billion. Its non-GAAP loss of $0.22 per share was significantly below analysts’ consensus estimates.

Is now the time to buy PENN Entertainment? Find out by accessing our full research report, it’s free for active Edge members.

As stated in the joint release issued this morning by PENN and ESPN, Jay Snowden, Chief Executive Officer and President, said: “When we first announced our partnership with ESPN, both sides made it clear that we expected to compete for a podium position in the space. Although we made significant progress in improving our product offering and building a cohesive ecosystem with ESPN, we have mutually and amicably agreed to wind down our collaboration.

Established in 1982, PENN Entertainment (NASDAQ:PENN) is a diversified American operator of casinos, sports betting, and entertainment venues.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, PENN Entertainment grew its sales at a 11.9% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. PENN Entertainment’s recent performance shows its demand has slowed as its annualized revenue growth of 2% over the last two years was below its five-year trend. Note that COVID hurt PENN Entertainment’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

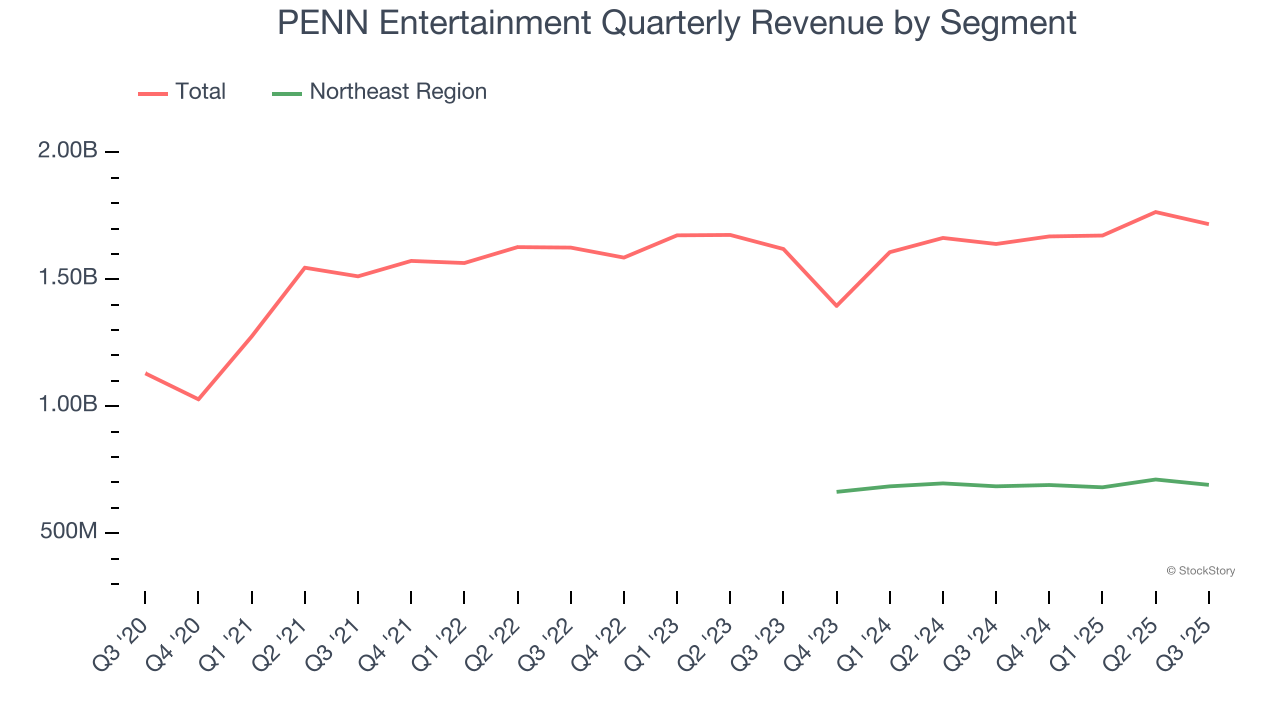

PENN Entertainment also breaks out the revenue for its most important segment, Northeast Region. Over the last two years, PENN Entertainment’s Northeast Region revenue (casinos, hotels) averaged 1.6% year-on-year growth.

This quarter, PENN Entertainment’s revenue grew by 4.8% year on year to $1.72 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

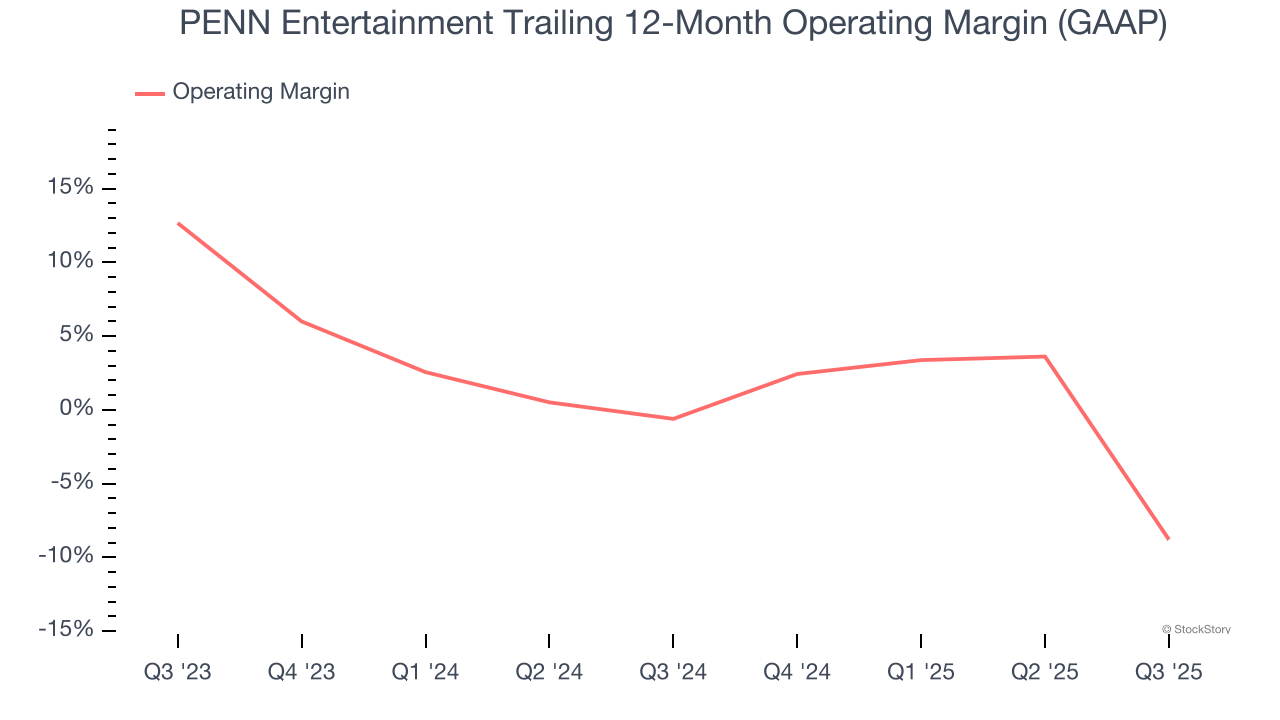

PENN Entertainment’s operating margin has shrunk over the last 12 months and averaged negative 4.9% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

This quarter, PENN Entertainment generated a negative 45.2% operating margin. The company's consistent lack of profits raise a flag.

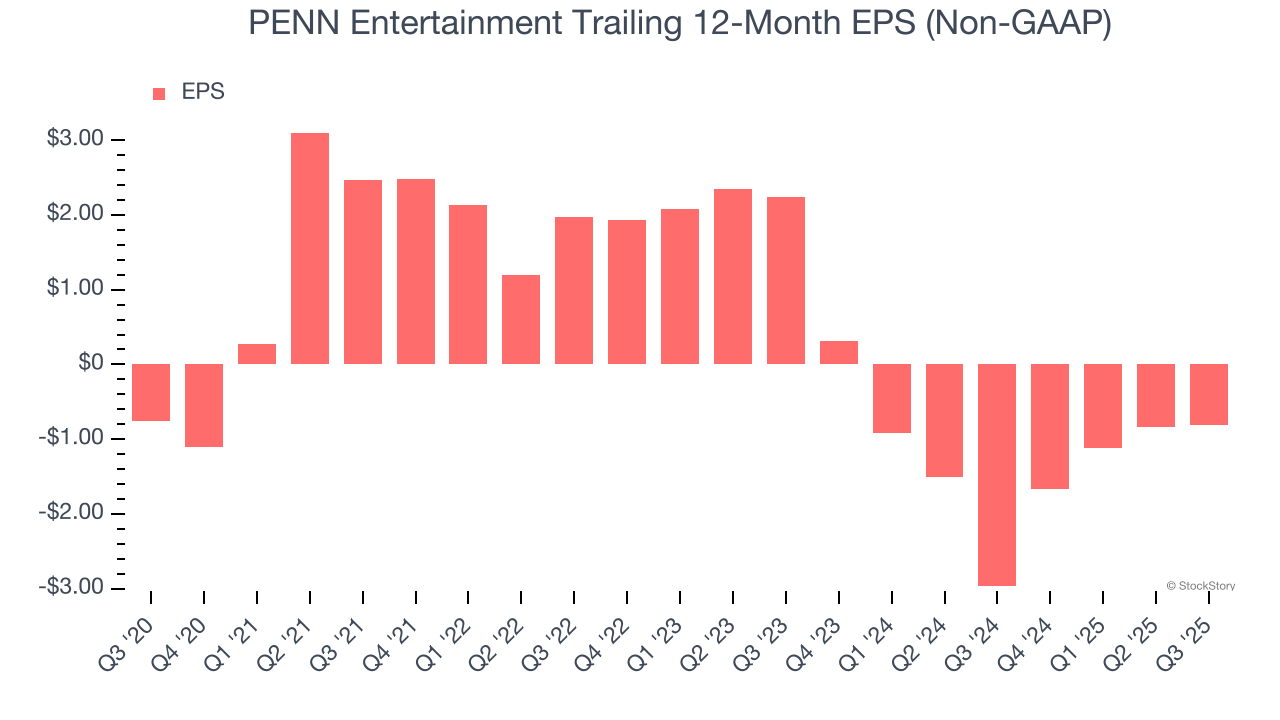

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

PENN Entertainment’s earnings losses deepened over the last five years as its EPS dropped 1.2% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, PENN Entertainment’s low margin of safety could leave its stock price susceptible to large downswings.

In Q3, PENN Entertainment reported adjusted EPS of negative $0.22, up from negative $0.25 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast PENN Entertainment’s full-year EPS of negative $0.81 will flip to positive $1.17.

We struggled to find many positives in these results. Its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 9.2% to $17.87 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Mar-30 | |

| Mar-23 | |

| Mar-21 | |

| Mar-19 | |

| Mar-12 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 | |

| Mar-02 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite