|

|

|

|

|||||

|

|

|

China's e-commerce titans Alibaba BABA and JD.com JD dominate the world's largest retail market, yet their strategic roadmaps diverge significantly. Alibaba pursues an ambitious RMB 380 billion three-year AI transformation, while JD.com focuses on operational excellence and strategic European expansion via CECONOMY acquisition. Management guidance reveals contrasting philosophies: Alibaba emphasizes AI infrastructure despite margin pressure, while JD.com projects sustained profitability expansion.

Let's delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

Alibaba's strategy centers on RMB 380 billion over three years for AI and cloud infrastructure, targeting a projected $1.8 trillion global AI market by 2030. First-quarter fiscal 2026 earnings showed AI-related revenue maintaining triple-digit growth for eight consecutive quarters, exceeding 20% of Cloud Intelligence Group's external revenues. Management expects continued market outpacing growth across automotive, manufacturing, and agriculture verticals.

However, near-term profitability challenges lack resolution visibility. Management prioritizes user acquisition and expanding use cases over immediate margin improvements, signaling prolonged pressure on profitability metrics. Quick commerce requires incremental RMB 50 billion, targeting RMB 1 trillion annualized GMV within three years, yet management provided no breakeven timeline, noting only that unit economics losses should improve by approximately half through logistics optimization.

October 2025 announcements reveal escalating deployment. The Plan C AI project, competing with ByteDance, plus the Hong Kong office acquisition with Ant Group, represent substantial spending beyond core commitment. Management refused to provide fiscal 2026 revenue or margin guidance, reflecting competitive uncertainty and unclear investment returns. While customer management revenues should accelerate in the coming quarters through higher take rates, the absence of quantitative milestones leaves investors without profitability anchors.

Capital allocation discipline appears questionable. Despite RMB 18.8 billion cash burn in the fiscal first quarter, Alibaba pursues multiple capital-intensive initiatives simultaneously. Management acknowledged potential quarterly fluctuations in capital expenditure pacing alongside supply chain backup plans, suggesting execution risks. For profitability-focused investors, Alibaba's outlook offers insufficient margin stabilization clarity.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.57 per share, down 13% over the past 30 days.

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

JD.com's outlook emphasizes operational execution on a proven playbook that management expects will deliver sustained margin expansion. Management indicated that the core retail business continues improving operating efficiency, with gross margins expanding for 13 consecutive quarters while operating margins maintain steady upward momentum. This signals operational leverage will continue driving profitability improvements.

Strategic priorities center on three initiatives. First, user engagement acceleration with quarterly active customers and shopping frequency both exceeding 40% year-over-year growth. Management noted this creates compounding effects through better unit economics and more efficient customer acquisition. Second, omnichannel strategy through JD MALL expansion and the One Step Ahead upgrade program targets consumption upgrade opportunities, which management identifies as key future growth drivers.

July 2025 CECONOMY acquisition provides European leadership pathway. Management emphasized the strategic importance of global expansion to leverage the company's distinctive supply chain capabilities, operational expertise, and technology platforms. The €4.60 per share offer securing 57.1% of MediaMarkt and Saturn's parent provides access to 1,000+ stores across 11 countries. Management structured the deal, maintaining CECONOMY as a standalone with local technology, minimizing integration risk while maximizing supply chain synergies.

Management's disciplined new business investment contrasts with competitors. While JD Food Delivery impacted second-quarter income, management emphasized efficient capital deployment at a measured pace aligned with market dynamics. Plans to maximize synergies across the broader ecosystem highlight capital-efficient growth. The $5 billion buyback, with $1.5 billion deployed in the first half of 2025, demonstrates confidence in generating substantial cash flow for both growth and returns.

The consensus mark for 2025 earnings is pegged at $2.8 per share, having moved north by 2.9% over the past 30 days.

JD.com, Inc. price-consensus-chart | JD.com, Inc. Quote

JD trades at a forward P/E of 9.15X versus Alibaba's 19.21X — a discount unjustified given JD's superior margin trajectory. This gap reflects food delivery skepticism, though management's disciplined allocation mitigates concerns.

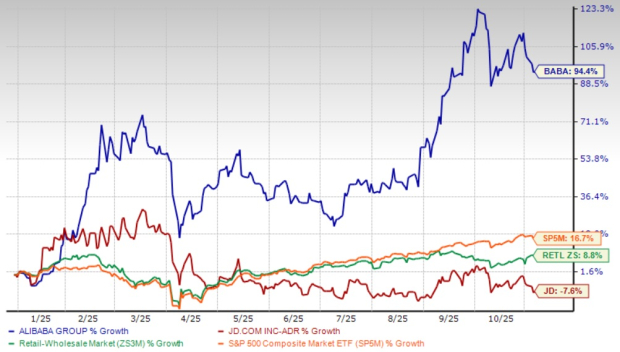

Alibaba's 94.4% year-to-date rally versus JD's 7.6% decline creates an attractive JD entry point. Alibaba's surge stemmed from AI enthusiasm rather than earnings power, leaving it vulnerable if investments disappoint. JD's muted performance despite consistent margin expansion suggests market underappreciation. JD's Nov. 13, 2025, third-quarter report offers an imminent catalyst for valuation reassessment.

JD.com represents a superior investment based on credible forward guidance, disciplined capital allocation, and attractive valuation. While Alibaba pursues capital-intensive AI transformation without margin stabilization timelines, JD management articulates a compelling roadmap for sustained margin expansion, strategic European growth through CECONOMY, and efficient ecosystem synergies. Trading at 9.15X forward P/E versus Alibaba's 19.21X — despite a superior operational trajectory — JD offers substantial upside as disciplined execution drives fundamental recognition. Investors should track JD for attractive entries while avoiding Alibaba until management provides credible evidence that AI investments will generate returns offsetting profitability sacrifices. BABA currently carries a Zacks Rank #5 (Strong Sell), whereas JD has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite