|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

The Boston Beer Company, Inc. SAM, a prominent player in the craft beer industry, is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 21.45X, which positions it at a premium compared with the industry’s average of 15.22X. The valuation indicates that the stock is overvalued.

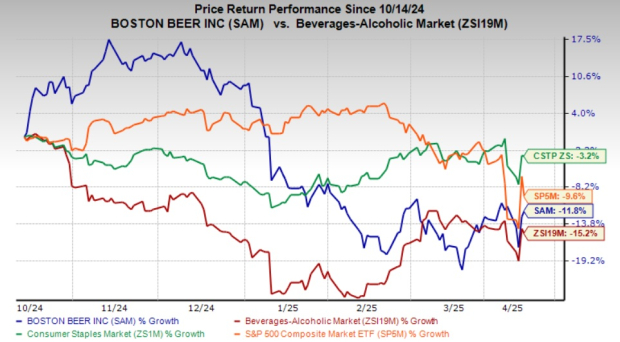

Boston Beer’s shares have plunged 11.8% in the past six months, slightly outperforming the industry’s 15.2% dip but underperforming the broader Consumer Staples sector, which fell 3.2%. However, it lagged the S&P 500, which slipped by just 9.6% in the same period. This reflects broad-based market weakness, with defensive sectors like Consumer Staples facing greater pressure.

Such a premium valuation often signals high investor expectations for growth. While this may concern some value-focused investors, it is essential to consider whether the fundamentals justify the price. Now the question arises, what will be the best move for SAM at the current valuation?

Boston Beer is grappling with challenges in its shipment and depletion volumes. Shipment volume has been weak in recent quarters due to the weak performance of Truly Hard Seltzer, although growth in Twisted Tea, Sun Cruiser and Hard Mountain Dew partially offset the decline.

As of early 2025, depletions were expected to remain stable year over year, with inventory levels for its brands being more in line with historical averages compared to the previous quarter. The outlook for the full year indicates modest fluctuations in depletions and shipments, with some potential upside in the first half of 2025, driven by specific brand demand and wholesaler inventory patterns, particularly for Sun Cruiser, Hard Mountain Dew and Truly Unruly. However, overall industry challenges, including consumer landscape conditions, may affect performance throughout the year.

Boston Beer has been facing a persistent slowdown in the hard seltzer category, which has weighed on the demand for its Truly brand in recent quarters. The declining trends in hard seltzer have impacted the company’s depletions, reflecting broader shifts in consumer preferences.

The deceleration in the hard seltzer market is primarily due to the loss of novelty among consumers, as a growing number of beyond-beer products have entered the marketplace. Additionally, the challenging macroeconomic environment has prompted a shift in volume from hard seltzers to premium light beers, which are more competitively priced.

On its last earnings call, Boston Beer issued guidance for 2025, expecting depletions and shipments to range from a slight decline in low-single digits to a modest increase in low-single digits for the year. This outlook reflects the slower pace of improvement in the overall consumer landscape. However, shipments for the first half of 2025 are projected to be at the high end of the full-year guidance, driven by the timing of planned demand and wholesaler inventory levels, particularly for brands like Sun Cruiser, Hard Mountain Dew and Truly Unruly. Additionally, the company anticipates a price increase of 1-2% for 2025 to offset commodity and inflationary pressures.

Reflecting the negative sentiment around SAM, the Zacks Consensus Estimate for fiscal 2025 and 2026 has seen downward revisions. In the past seven days, analysts have lowered estimates for the current fiscal by 3.7% to $10.47 and for the next fiscal by 6.2% to $11.75 per share.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Boston Beer is currently trading at a premium, which indicates that the stock is overvalued. With the recent stock decline, the company faces significant challenges such as shifting consumer spending patterns and a slowdown in the hard seltzer market. Given the downward revisions in earnings estimates and the ongoing headwinds, SAM's elevated valuation appears unsustainable. The stock carries a Zacks Rank #5 (Strong Sell) at present, indicating a cautious near-term outlook.

Primo Brands Corporation PRMB is a branded beverage company with a focus on healthy hydration, delivering sustainably and domestically sourced diversified offerings across products, formats, channels, price points and consumer occasions, distributed primarily in every state and Canada. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Primo Brands’ current financial-year sales and EPS indicates growth of 146.9% and 54.5%, respectively, from the prior-year levels. PRMB has a trailing four-quarter earnings surprise of 7.2%, on average.

Molson Coors Beverage Company TAP, a global manufacturer and seller of beer and other beverage products, has an impressive diverse portfolio of owned and partner brands. TAP currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Molson Coors’ current financial-year EPS indicates growth of 6.7% from the prior-year levels. The company has a trailing four-quarter earnings surprise of 18.1%, on average.

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. It currently carries a Zacks Rank of 2. UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average.

The consensus estimate for United Natural Foods’ current financial-year sales and earnings implies growth of 1.9% and 485.7%, respectively, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-22 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite