|

|

|

|

|||||

|

|

|

ServiceNow’s NOW subscription revenues have been benefiting from growing demand for its workflows. Subscription revenues, which account for roughly 97% of the company’s total revenues, have increased 21% over the trailing nine-month period in 2025 compared with the year-ago period’s reported figure.

ServiceNow raised subscription revenue guidance for 2025 post third-quarter 2025 results, which is now expected between $12.835 billion and $12.845 billion, suggesting 20% on a non-GAAP constant currency (cc) basis and 20.5% on a reported basis from 2024’s reported figure. However, this is slower than NOW’s subscription revenue growth rate of 23% in 2024.

So, what should investors do with the NOW stock? Let’s find out.

ServiceNow shares have plunged 17.9% in the past year, underperforming the Zacks Computer and Technology sector as well as competitors, including Workday WDAY, Oracle ORCL and SAP SE SAP. While shares of Workday have dropped 16% over the same time frame, Oracle and SAP shares have returned 24.6% and 8.5%, respectively.

NOW’s decline can be attributed to challenging macroeconomic trends, including uncertainty related to the ongoing government shutdown, along with stiff competition. The company’s fourth-quarter 2025 guidance reflects tightening budgets of the U.S. federal agencies, which is expected to hurt subscription revenues.

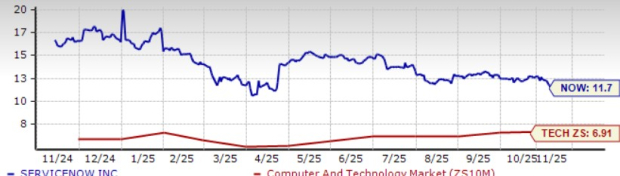

ServiceNow stock has a Value Score of F, which suggests a stretched valuation at this moment. The stock is trading at a premium, with a forward 12-month price/sales of 11.7X compared with the broader sector’s 6.91X, Workday’s 5.82X, SAP’s 6.63X and Oracle’s 9.09X.

Technically, NOW shares are trading below the 50-day and 200-day moving averages, indicating a bearish trend.

ServiceNow had 103 transactions over $1 million in net new annual contract value (ACV) in the third quarter, six of which were greater than $10 million in net new ACV. The company expanded its customer relationships, reaching 553 customers with more than $5 million in ACV at the end of the reported quarter. The number of customers contributing $50 million or more increased more than 20% year over year.

Technology workflows had 50 deals over $1 million, including six over $5 million. ITSM, ITOM and ITAM were all in 15 of NOW’s top 20 deals with double-digit deals over $1 million. Security and risk combined for 12 of the top 20 deals, with three deals over $1 million. CRM and industry workflows were in 14 of the top 20, with 15 deals over $1 million, and core business workflows were in 13 of the top 20, with 14 deals over $1 million. NOW saw 12 Now Assist deals over $1 million, including one over $10 million in the reported quarter. AI Control Tower deal volume more than quadrupled sequentially in the third quarter of 2025.

Net new ACV in transportation and logistics industries grew more than 90% year over year, while more than 50% growth was seen in retail and hospitality and education. Net new ACV at U.S. federal business grew more than 30% on a year-over-year basis.

Moreover, ServiceNow’s expanding partner base includes the likes of NVIDIA, Figma, Genesys and others. The expanded partnership with NVIDIA introduced Apriel 2.0, the next generation of NOW’s Apriel Nemotron open model family that is post???trained with NVIDIA and ServiceNow???provided data and engineered to deliver AI reasoning and multimodal capabilities to enterprises in a faster, smaller, more cost???efficient footprint. ServiceNow workflows are now getting integrated with the NVIDIA AI Factory for Government reference design to reimagine data center operations.

The Zacks Consensus Estimate for NOW’s fourth-quarter 2025 reflects downward revision trends. The current quarter earnings estimate of $4.35 per share has declined by a nickel over the past 30 days and suggests 18.53% growth over the figure reported in the year-ago quarter.

ServiceNow, Inc. price-consensus-chart | ServiceNow, Inc. Quote

However, 2025 and 2026 earnings estimates reflect positive trends. The Zacks Consensus Estimate for NOW’s 2025 earnings estimate is currently pegged at $17.29 per share, up 3% over the past 30 days and suggests 24.21% growth over 2024’s reported figure. The consensus mark for 2026 earnings estimate is currently pegged at $20.18 per share, up 1.7% over the past 30 days and suggests 16.66% growth over 2025’s estimated figure.

NOW’s expanding portfolio, growing workflow adoption and rich partner base are expected to improve its top-line growth. However, a challenging macroeconomic environment and a stretched valuation are concerns.

ServiceNow currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the NOW stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 12 min | |

| 21 min | |

| 26 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite