|

|

|

|

|||||

|

|

|

Over the past six months, Triumph Financial’s stock price fell to $53.56. Shareholders have lost 10.7% of their capital, which is disappointing considering the S&P 500 has climbed by 16.9%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Triumph Financial, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons you should be careful with TFIN and a stock we'd rather own.

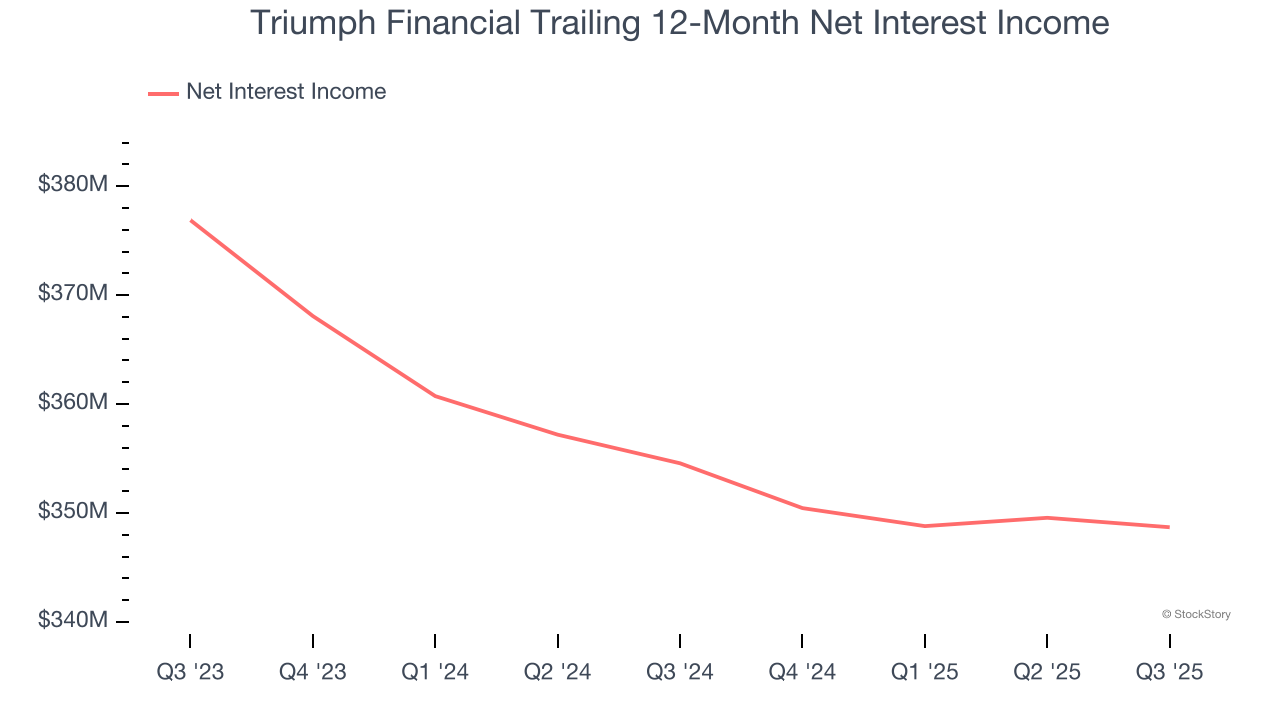

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Triumph Financial’s net interest income has grown at a 5.3% annualized rate over the last five years, worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

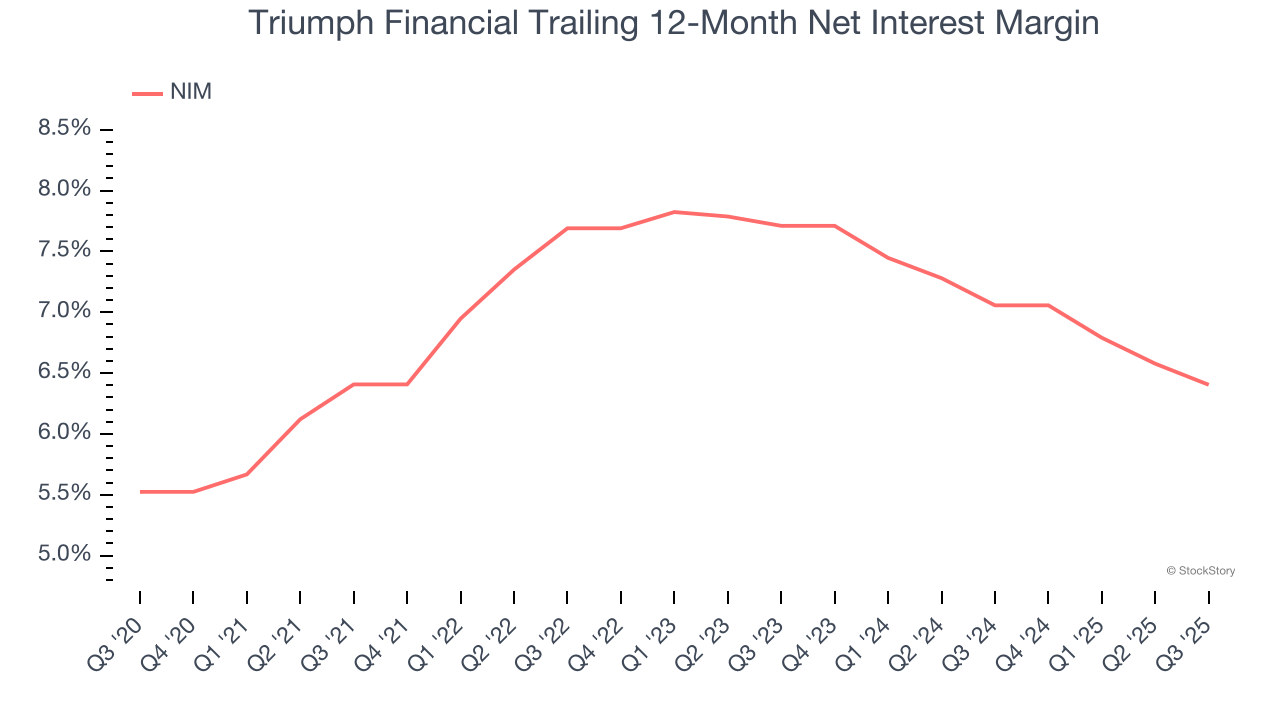

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, Triumph Financial’s net interest margin averaged 6.7%. However, its margin contracted from 7.7% to 6.4% over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Triumph Financial either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

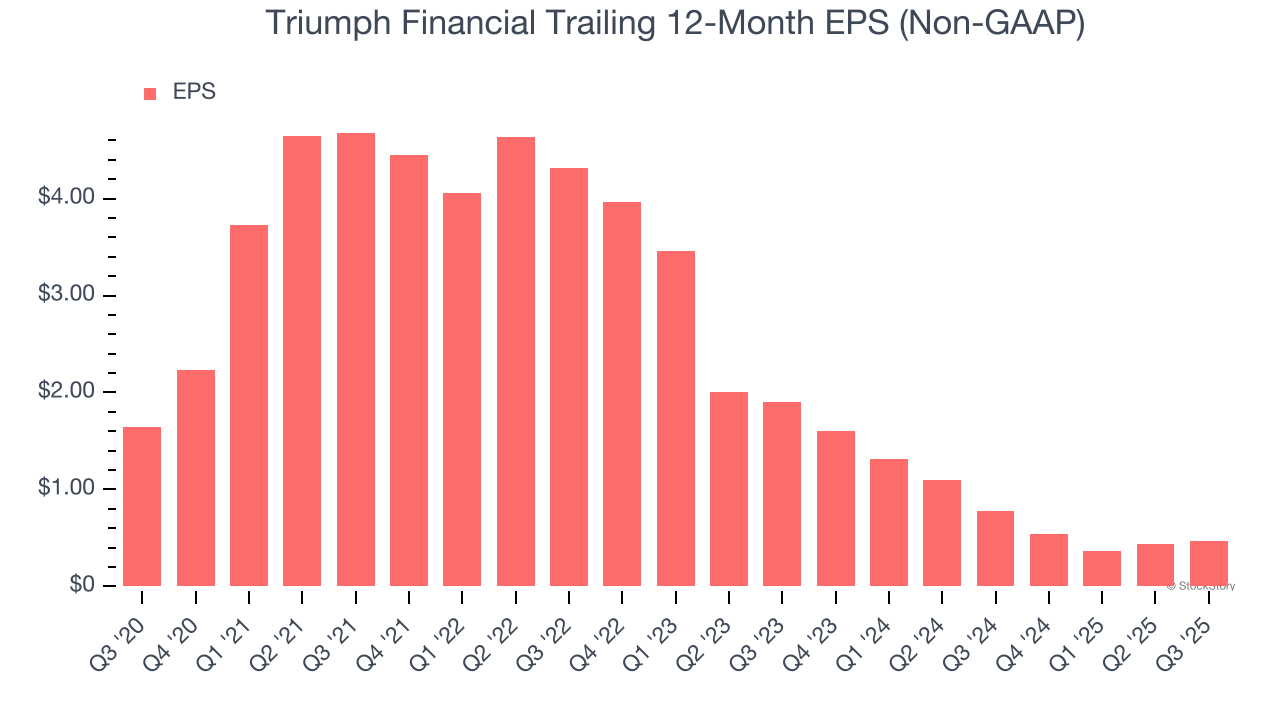

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Triumph Financial, its EPS declined by 22.1% annually over the last five years while its revenue grew by 6%. This tells us the company became less profitable on a per-share basis as it expanded.

Triumph Financial isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 1.4× forward P/B (or $53.56 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at one of our top software and edge computing picks.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-08 | |

| Jun-16 | |

| May-29 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-21 | |

| Apr-08 | |

| Feb-27 | |

| Feb-27 | |

| Feb-23 | |

| Feb-17 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite