|

|

|

|

|||||

|

|

|

Over the last six months, CVB Financial’s shares have sunk to $18.62, producing a disappointing 6.7% loss - a stark contrast to the S&P 500’s 16.9% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in CVB Financial, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Despite the more favorable entry price, we're cautious about CVB Financial. Here are three reasons you should be careful with CVBF and a stock we'd rather own.

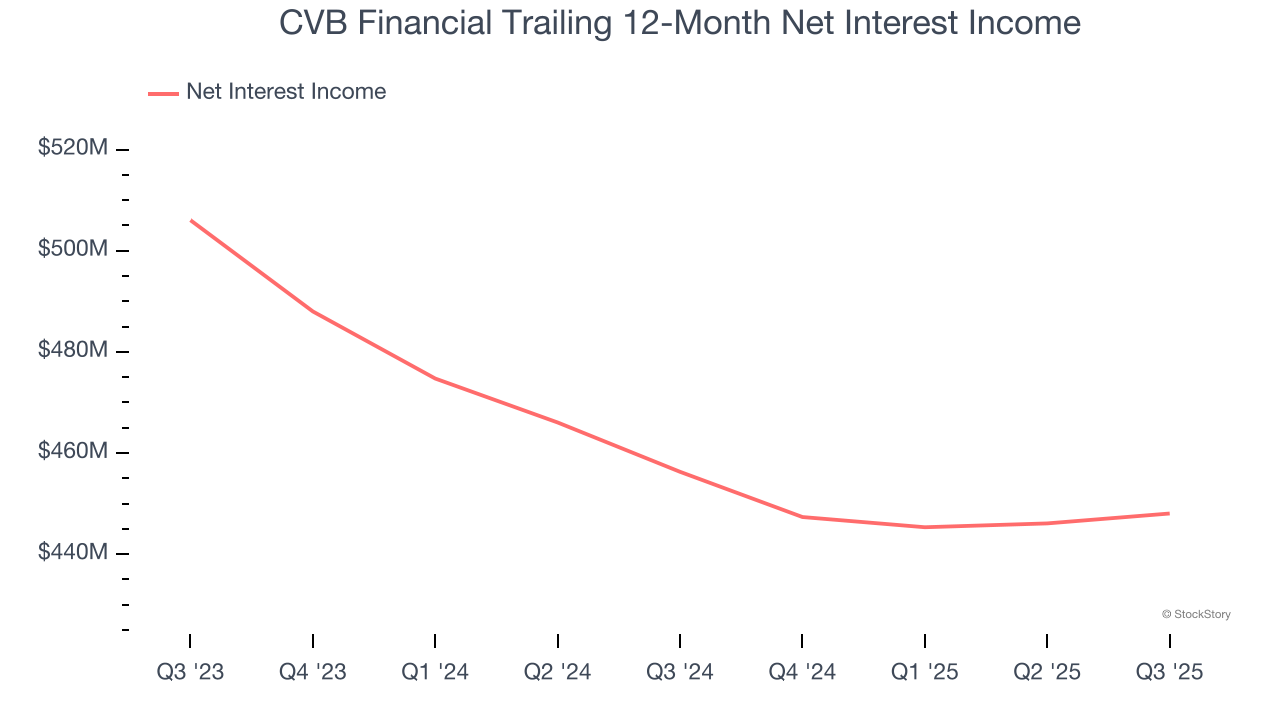

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

CVB Financial’s net interest income has grown at a 1.7% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

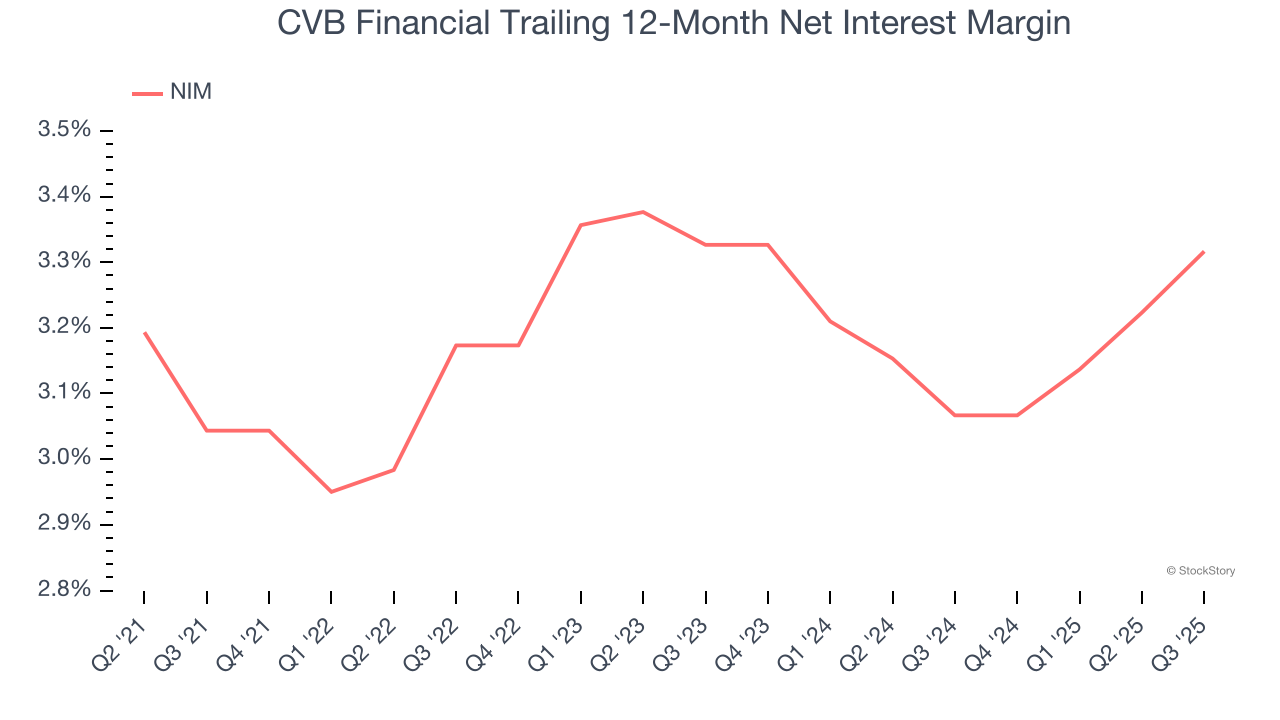

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that CVB Financial’s net interest margin averaged a subpar 3.2%, reflecting its high servicing and capital costs.

Tangible book value per share (TBVPS) serves as a key indicator of a bank’s financial strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during financial distress.

Although CVB Financial’s TBVPS increased by a meager 3% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at an impressive 14.4% annual clip over the past two years (from $8.39 to $10.98 per share).

CVB Financial isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 1.1× forward P/B (or $18.62 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jun-24 | |

| Jun-15 | |

| May-21 | |

| Apr-24 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-17 | |

| Apr-01 | |

| Mar-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite