|

|

|

|

|||||

|

|

|

IonQ's third-quarter revenue came in much higher than management had previously predicted.

Over the last year, IonQ has spent billions of dollars acquiring competing quantum AI businesses.

For now, most of IonQ's growth appears fueled by acquisitions, rather than organic demand.

The quantum computing race is heating up. However, unlike other popular domains in the artificial intelligence (AI) landscape, quantum AI isn't dominated by big-tech darlings such as Nvidia or Palantir Technologies.

Instead, investors have taken a keen liking to more speculative businesses promising to revolutionize the computing industry. Among these companies is IonQ (NYSE: IONQ), which leverages exploratory trapped ion systems to develop its quantum technology.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Over the past year, shares of IonQ have skyrocketed. One of the main catalysts behind the company's meteoric rise is the stunning pace at which its revenue is growing. Does IonQ hold the keys to the next breakthrough frontier in the AI realm?

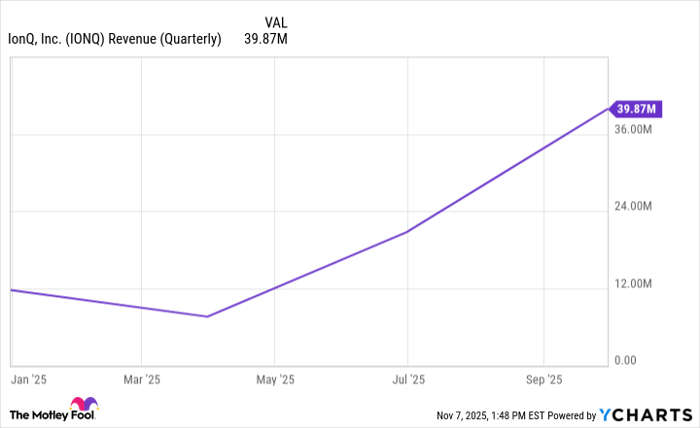

For the quarter ended Sept. 30, IonQ generated roughly $40 million in revenue. This represented growth of 222% year over year and came in 37% higher than management's previously stated guidance.

IONQ Revenue (Quarterly) data by YCharts.

With so much momentum across the company's top line, investors should be curious about what's fueling this growth. Thankfully, the detailed notes in IonQ's latest 10Q filing can help uncover the answer.

Image source: Getty Images.

IonQ doesn't reveal the specific names of its customers, but details in the company's filings still reveal some information. For the nine months ended Sept. 30, three customers accounted for 61% of IonQ's total revenue. Within this cohort, just two of the customers comprised 54% of sales.

Given these figures, it's clear that IonQ is vulnerable to customer concentration risk. Said differently, if any one of these three customers churned, IonQ's revenue could take a nosedive. This leads to another important idea -- how IonQ is trying to diversify its customer base. Over the last year, IonQ completed the following acquisitions:

Taking this one step further, IonQ reported revenue of $68 million through the first nine months of 2025. In the company's disclosures, management explains that had all of IonQ's acquisitions been closed in January 2024, the pro forma revenue figure would be about $101 million.

This implies that a meaningful portion of IonQ's revenue is coming from the other businesses outlined above -- calling into question the strength of the company's organic-growth profile.

Another way of looking at this picture is to say that IonQ is inheriting the clients of competing quantum businesses, rather than winning over new customers of its own through savvy sales and marketing tactics or competitive technological advantages.

Image source: Getty Images.

From my perspective, IonQ isn't on the verge of a quantum breakthrough, given that its revenue is artificially inflated from all of these deals. While the idea of quantum computing is interesting, the technology itself has yet to deliver commercial application at scale -- yet another reason demand for IonQ's products remains fairly muted.

Moreover, given the prices IonQ is willing to pay in these deals, I'm worried that management could burn through the company's $3.5 billion of cash relatively quickly -- further casting doubt about the company's long-term sustainability. As a result, projecting the company's sales trajectory looks more like an exercise in false precision than anything else.

I see IonQ as a stock primarily influenced by day traders and retail investors chasing what could be a pipe dream. Investors seeking durable opportunities to buy and hold for the long term are likely better off passing on IonQ in favor of more established blue chip companies in the AI realm.

Before you buy stock in IonQ, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and IonQ wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $612,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,184,044!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 194% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Adam Spatacco has positions in Nvidia and Palantir Technologies. The Motley Fool has positions in and recommends IonQ, Nvidia, and Palantir Technologies. The Motley Fool has a disclosure policy.

| Feb-28 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite