|

|

|

|

|||||

|

|

|

Beyond Meat became the latest hyped stock for retail investors following a 1,600% four-day rally in October.

This parabolic ascent was driven by social media misinformation and not a short squeeze.

Beyond Meat's outstanding share count has gone parabolic, and additional share offerings will likely be needed to offset its persistent cash burn.

Roughly 30 years ago, the arrival and proliferation of the internet altered the corporate landscape by opening new sales channels for businesses that hadn't previously existed. But the rise of the internet also paved the way for the retail investor revolution. It broke down information barriers that had previously existed between Wall Street and Main Street, and gave everyday investors the ability to buy and sell stocks online.

Over time, retail investors have come to play a larger role on Wall Street. As of 2021, everyday investors accounted for 25% of total equities trading volume, which is almost double where things stood one decade prior, according to a report from the University of Missouri-Kansas City School of Law.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

While a sizable percentage of retail investors have come to realize that time is their ally, the short squeeze hype that occurred in early 2021 also ushered in the meme stock era. Instead of a company's operating performance dictating its valuation, social media hype (briefly) ruled the roost.

Image source: Getty Images.

Last month, plant-based food company Beyond Meat (NASDAQ: BYND) became the latest hyped meme stock following a trough-to-peak surge of 1,600% in its share price in less than four trading sessions.

While social media interest can provide a brief spark for publicly traded companies, a combination of misinformation and share-based dilution appears poised to halt Beyond Meat stock in its tracks.

Most meme stock investors rally around the thesis of making life difficult for short-sellers. These are investors wagering on the share price of a public company to decline. Whereas gains for short-sellers cap at 100% (a company's share price can't fall below $0), their losses are, in theory, limitless.

The ideal outcome for meme stock investors in companies with high short interest is a short squeeze. For a short squeeze to take place, one or more of the following variables are needed:

The only variable that's an absolute necessity for a short squeeze is to have pessimists running for the exit all at once. Since short-sellers have to buy shares to get out of their position, it can cause an already rising share price to briefly turn parabolic.

While it would appear that a short squeeze took place in October, Beyond Meat's filings with the Securities and Exchange Commission (SEC) show otherwise.

On Oct. 15, more than 316.1 million shares were issued in a convertible note debt-for-equity swap. Based on a company filing with the SEC, these shares became freely tradable on Oct. 17. We also know this to be fact because three out of four beneficial owners (former convertible bondholders) filed Schedule 13D or 13G with SEC showing they'd sold shares.

While investors were relying on third-party financial websites, which can take a few days to update short interest and float data, primary sources made clear that Beyond Meat's outstanding share count and float had more than quintupled. This pushed its short interest relative to float into the mid-teens, and not the 81% to 162% figure that was floating around on social media message boards.

What we witnessed with Beyond Meat was nothing short of a misinformation-driven FOMO (fear of missing out) event -- not a short squeeze.

Image source: Getty Images.

Since Beyond Meat shares hit their crescendo in pre-market trading on Oct. 22, they've plunged by 86%, as of the closing bell on Nov. 11. With share price momentum waning, the company's operating performance and strategy have come into focus -- and that's terrible news for shareholders.

On Nov. 10, Beyond Meat unveiled its third-quarter operating results, which disappointed in a number of respects.

Leading up to this release, Beyond Meat had already issued preliminary sales guidance, as well as delayed the filing of its report by a week to determine the value of a non-cash impairment charge tied to select long-lived assets. The $70.2 million in net sales for the quarter was in-line with prior guidance, but down more than 13% from the previous year. Meanwhile, it's $112.3 million operating loss included the aforementioned $77.4 million, one-time charge related to certain long-lived assets.

These headline figures aren't the story. Rather, it's what the company had to say about its performance and how it's tackling its many headwinds.

For example, the greater than 18% third-quarter sales drop in its U.S. retail channel was spurred by a decline in product sold, higher trade discounts, and price decreases for select products. The entire thesis of plant-based meats was the perception of their health benefits and the expectation that consumers would willingly pay a premium for these benefits. Beyond Meat is plainly telling investors that U.S. consumers are unwilling to pay this premium.

Keep in mind, this isn't a one-quarter trend. Guidance for the December-ended quarter calls for $60 million to $65 million in sales, which is well below the $70 million consensus Wall Street analysts had been expecting. Beyond Meat's operating uncertainties aren't going to dissipate anytime soon.

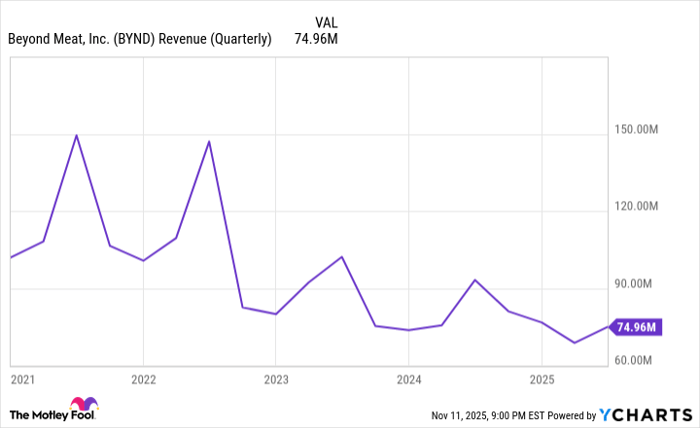

Beyond Meat's sales have been trending lower for years. BYND Revenue (Quarterly) data by YCharts. Above chart has not factored in the $70.2 million in sales reported for the September-ended quarter.

But the real drag for investors has been share-based dilution, which looks to be a necessary evil for Beyond Meat, if management is to right the ship.

More than 317 million shares were ultimately issued for its convertible note debt-for-equity exchange, and the company announced in its third-quarter operating results that nearly 58.9 million additional shares had been sold via an at-the-market (ATM) offering in October. This means Beyond Meat's outstanding share count has risen close to 500% in less than a month.

To put this increase into perspective, Beyond Meat shares closed at $2.01 on Oct. 10, which at the time worked out to a market cap of around $154 million. Even though its share price has declined 39% to $1.22, as of Nov. 11, its market cap is closer to $553 million, with more than 453 million shares now outstanding. In other words, Beyond Meat's market value has increased 259% in a month, even as its share price has plunged 39%.

The need to dilute investors to raise capital likely isn't over. Although Beyond Meat has effectively exhausted its ATM program, the company is seeking to increase its authorized outstanding share count from 500 million to 3 billion (Proposal 3 on the company's annual meeting proxy).

Selling more stock will almost certainly be necessary given Beyond Meat's persistent cash outflow from operations. Despite the efforts of management to reduce certain expenses, it's lost money on a quarterly basis for five years, and it's burning in the neighborhood of $30 million in cash from its operating activities per quarter.

Dilution is the only solution for Beyond Meat at the moment, which paints a worrisome picture for its stock and its shareholders.

Before you buy stock in Beyond Meat, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Beyond Meat wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $612,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,184,044!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 194% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Beyond Meat. The Motley Fool has a disclosure policy.

| Mar-12 | |

| Mar-09 | |

| Mar-07 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 |

Beyond Meat drops the 'Meat' from its name as it expands to plant-based drinks and snacks

BYND

Associated Press Finance

|

| Mar-04 | |

| Mar-02 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-24 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite