|

|

|

|

|||||

|

|

|

Target has seen its in-store sales decline, while its digital sales have increased.

Target's membership and advertising businesses have shown promising growth.

With 54 consecutive years of dividend increases, Target is a Dividend King.

You can't deny that Target (NYSE: TGT) has been one of the premier retail stores in the U.S. for decades. However, this historical prestige hasn't kept the company's stock from going on a prolonged slump over the past few years.

From March 20, 2020, (the bottom of the COVID-19 bear market) to Aug. 13, 2021, Target's stock surged an impressive 168%, hitting an all-time high. Unfortunately, since then, the stock has plummeted by 65%. Just this year, shares lost more than a third of their value through the beginning of November.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Needless to say, this is less than ideal and has frustrated investors. But with the stock as beaten down as it is, is 2026 shaping up to be the year of the return? Let's take a look.

Image source: Target.

There hasn't been one single issue that's caused Target's slump; it's a few issues that happened to hit at the wrong time, causing a domino effect. The three main issues are declining sales and reduced in-store traffic, tightening margins, and community boycotts resulting from some controversial decisions made by leadership.

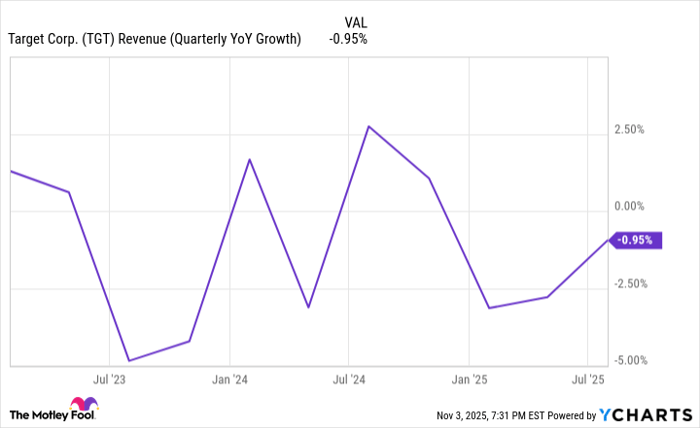

In the second quarter, Target's net sales decreased by nearly 1%, while its in-store sales declined by 3.2%. That continues a trend seen lately from the retailer. In the first quarter, those sales were down 3.8% and 5.7%, respectively.

TGT Revenue (Quarterly YoY Growth) data by YCharts

Aside from the stagnant sales growth (or lack thereof, in many cases), investors are also concerned about the effects new tariffs will have on Target's margins, as its costs are potentially set to increase.

We've seen the tariffs and their various percentages flip-flop, so it's hard to estimate how impactful they will be, but it's worth paying attention to for a retailer that relies heavily on imported goods.

Enough with the negatives. There are still positive things surrounding the business, especially when it comes to its growth beyond just its core retail business. Its membership plan, Target Circle 360, has been gaining traction among frequent shoppers. This is great news for Target's margins because it's recurring revenue coming in without needing to sell additional products.

It also has its marketplace platform, Target Plus, and advertising platform, Roundel. Together, these go hand in hand because more third-party sellers joining the marketplace means Target receives more valuable data, which helps strengthen Roundel's value through more effective targeted ad campaigns.

Although net sales were down in the second quarter, digital sales were up 4.3%. In the first quarter, they were up 4.7%. This is a positive sign that Target is able to capture online demand while its in-store sales remain stagnant.

To compete with companies like Walmart and Amazon, Target will need to double down on convenience and go beyond just standard retail. We've gotten to the point where consumers prioritize convenience and delivery speed, and Target has been making efforts to cement itself as a retailer that can provide that.

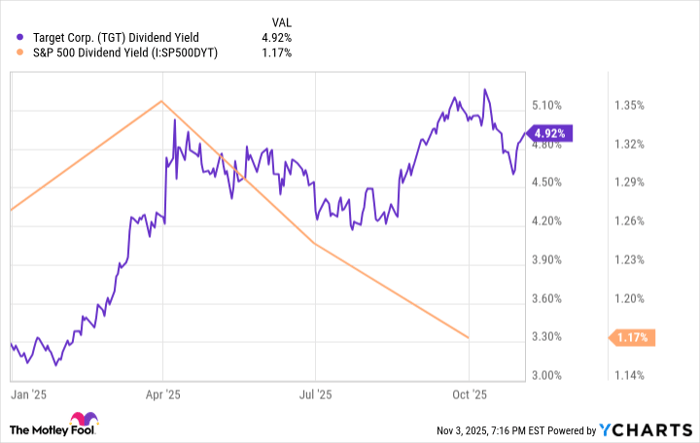

One thing that remains stable with Target is its dividend. With 54 consecutive years of dividend increases, Target is one of only a couple of dozen Dividend Kings (a company with at least 50 consecutive years of increases).

Its quarterly dividend is $1.14 per share, but given how much its stock price has fallen, its yield is fairly high at just over 4.9%. That's more than four times the S&P 500 (SNPINDEX: ^GSPC) average, placing it in ultra-high-yield dividend stock territory.

TGT Dividend Yield data by YCharts

Target's dividend doesn't negate the issues the company is facing, but it's a good incentive for investors to remain patient while the company tries to get back on track.

Nobody can say definitively how Target's stock will perform in 2026, but one thing is certain: With its low valuation, there's much more upside than downside heading into the new year. I wouldn't bank on it turning the corner in 2026, but it's a good value for long-term investors.

Before you buy stock in Target, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Target wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $612,872!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,184,044!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 194% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Target and Walmart. The Motley Fool has a disclosure policy.

| 36 min | |

| 3 hours | |

| 4 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite