|

|

|

|

|||||

|

|

|

Shares of Lockheed Martin Corporation LMT have surged 4.6% in the past three months, underperforming the Zacks Aerospace-Defense industry’s growth of 4.9%. However, it outperformed the broader Zacks Aerospace sector’s gain of 3.8%. It also came below the S&P 500’s return of 7.7% in the same time frame.

Other industry players, such as Huntington Ingalls Industries HII and General Dynamics GD, have delivered a stellar performance in the past three months. Shares of HII and GD have risen 18.8% and 10.6%, respectively, in the said period.

With LMT’s recent gains, some investors may want to buy the stock. However, it’s important to check if the company’s fundamentals can support long-term growth or if the rise is only short-term. Understanding LMT’s growth outlook and risks is key to making an informed decision.

LMT’s recent performance appears to be supported by its strong quarterly results, strategic partnerships and notable contract wins, which have helped sustain investor confidence. In October, the company reported its third-quarter 2025 results, showing revenue growth of 8.8% and a 2.2% rise in net earnings compared with the same period last year.

In November 2025, LMT formed a strategic collaboration with PsiQuantum to advance quantum computing research and applications for aerospace and defense. This agreement marks an important step toward exploring how quantum computing can help address complex national security and aerospace challenges. It also supports the development of large-scale, fault-tolerant quantum hardware designed to deliver reliable results for critical missions.

In October 2025, LMT’s Sikorsky unit received a contract from the County of Los Angeles for two S-70i FIREHAWK helicopters. These aircraft will strengthen the county’s wildfire suppression, rescue and emergency medical service capabilities across its 4,000-square-mile area.

In the same month, the company announced a partnership with Google Public Sector to integrate Google’s generative AI technology, including its Gemini models, into the Lockheed Martin AI Factory. This collaboration will bring Google’s advanced AI tools into Lockheed Martin’s secure, on-premises and isolated environments, making them accessible to employees across the organization.

Additionally, LMT was awarded a $233 million contract to deliver IRST21 Block II systems and initial spares to the U.S. Navy and Air National Guard.

For defense contractors like LMT, a steady flow of contract wins from the Pentagon and U.S. allies for its combat-proven defense products, such as the most recent awards, serves as a major growth catalyst.

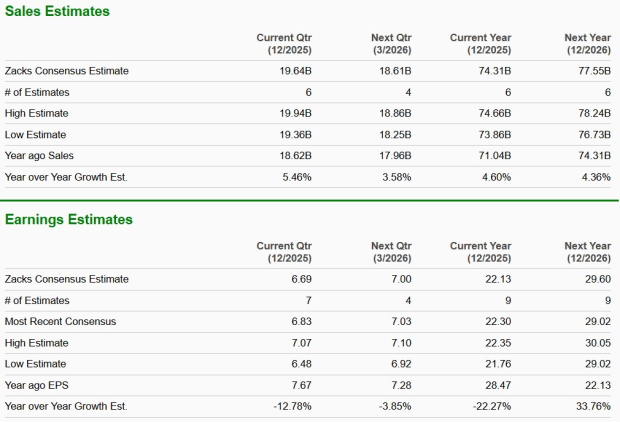

The Zacks Consensus Estimate for LMT’s 2025 sales implies year-over-year growth of 4.6%, while that for 2026 sales indicates an improvement of 4.4%. The consensus estimate for its 2025 earnings implies a year-over-year decline of 22.3%, while that for 2026 earnings indicates an improvement of 33.8%.

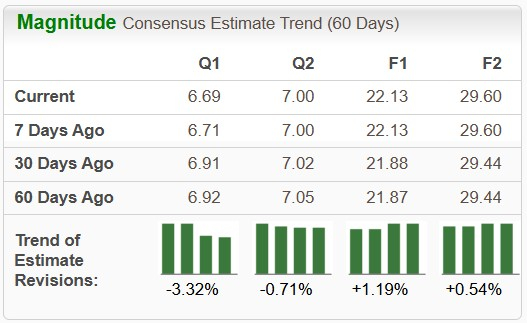

Further, the upward revision in its 2025 and 2026 earnings over the past 60 days suggests investors’ increasing confidence in this stock’s earnings generation capabilities.

In terms of valuation, LMT’s forward 12-month price-to-earnings (P/E) is 15.55X, a discount to the industry average of 29.21X. This suggests that investors will be paying a lower price than the company's expected earnings growth compared with its industry average.

HII and GD are trading at a premium in comparison with LMT. HII’s forward 12-month price-to-earnings is 18.98X, while GD’s forward 12-month price-to-earnings is 20.61X.

LMT continues to face financial and operational challenges that may pressure its performance. Persistent labor shortages across the aerospace-defense sector pose operational risks. The 2025 Workforce Study by the Aerospace Industries Association and McKinsey found that nearly a quarter of the workforce is more than 55, while attrition remains elevated at about 14.5%. Such workforce issues may lead to production delays, cost pressures and delivery setbacks, potentially weighing on Lockheed Martin’s margins and investor sentiment.

LMT has faced notable financial setbacks on several classified contracts. During the first nine months of 2025, the company recorded losses of $950 million on an ongoing classified program at its Aeronautics business segment, $570 million on the Canadian Maritime Helicopter Program, $95 million on the Turkish Utility Helicopter Program at its RMS business segment, and $105 million of unfavorable profit adjustments on C-130 programs at the Aeronautics business segment. Any further cost overruns or performance issues could result in additional material losses, putting further pressure on the company’s future financial results.

Given LMT’s discounted valuation and improving long-term growth outlook, the stock appears fairly valued with potential for steady returns. Its strong quarterly performance and strategic partnerships with firms like Google and PsiQuantum provide a positive foundation for future growth.

However, ongoing labor shortages, cost overruns on classified contracts and operational risks could weigh on near-term performance. Therefore, existing shareholders may consider holding the stock, while new investors might prefer to wait for more stability in the company’s financial and operational performance before taking a position.

LMT currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 6 hours |

Palantir AI Boosts Pentagon Capabilities but LMT, RTX May Be the Better Missile Shortage Plays

LMT

Benzinga Prediction Markets

|

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite