|

|

|

|

|||||

|

|

|

Last week, Canopy Growth Corporation CGC reported its second-quarter results for fiscal 2026 (year ending March 2026). While earnings beat our estimates, sales missed the mark.

This Canada-based cannabis operator posted a narrower-than-expected loss of 1 cent, significantly lower than the 95-cent loss reported in the year-ago period. Sales rose 6% year over year to more than $48 million (~C$67 million), primarily driven by encouraging momentum for marketed products in the Canadian market.

However, long-term investors typically focus beyond a single quarter’s numbers and assess broader fundamentals. Let’s explore the company’s fundamentals to better understand how to play the stock after its latest results.

Canopy’s cannabis business spans both recreational and medical markets, and the recent results indicate encouraging progress in both areas. Overall, cannabis revenues rose 12% year over year, supported by double-digit growth in adult-use and medical cannabis segments across Canada.

In Canada, adult-use revenues climbed 30%, driven by a strong uptake for infused pre-roll joints (PRJ) and the recently launched All-In-One (AIO) vapes under its Tweed and 7ACRES. Meanwhile, medical cannabis sales in the country increased 17%, supported by growth in insured patient enrollments, larger order volumes, and an expanded range of cannabis products under the Spectrum Therapeutics banner.

This rising uptake more than offset the soft sales performance of Canopy’s international cannabis division and its Storz & Bickel subsidiary during the quarter. While international cannabis sales were impacted by the ongoing supply-chain challenges in Europe, Storz & Bickel faced a tough comparison to last year’s elevated sales levels and broader consumer spending pressures.

Looking ahead, Canopy expects growth to accelerate in the second half of fiscal 2026, supported by new product launches such as PRJ and AIO vapes. The company is also working to streamline its European supply chain, though meaningful stabilization is not expected until the end of the fiscal year. Meanwhile, Storz & Bickel revenues are projected to rebound sequentially in Q3, driven by the growing uptake of the recently launched Veazy sales and seasonal holiday demand. However, tariff-related pressures may weigh on near-term performance in the United States.

Over the past two years, Canopy Growth has been streamlining operations by exiting lower-margin businesses and selling non-core assets in order to boost liquidity, reduce operating expenses and clear its path toward profitability. A major strategic focus has been unifying its medical cannabis operations globally, while sharpening commercial execution in Canada’s adult-use market.

Canopy’s overall gross margins for Q2 slipped 200 basis points over the year-ago period to 33%, reflecting lower sales of higher-margin cannabis in international markets and increased inventory provisions. Despite this, the company still beat bottom-line estimates on the back of lower SG&A expenses, which helped improve adjusted EBITDA by 45% year over year. Canopy also strengthened its balance sheet by prepaying $50 million in senior secured debt, marking continued progress in its deleveraging strategy.

Looking ahead, the company aims to further streamline its cost of goods sold through operational efficiencies, improved cultivation yields and tighter supplier management. These initiatives, coupled with disciplined capital allocation and product mix optimization, are expected to support Canopy’s goal of achieving sustained profitability in the coming quarters.

Tilray continues to operate in a crowded field, facing stiff competition from Aurora Cannabis ACB, Curaleaf Holdings CURLF and Tilray Brands TLRY. Each of these players is pursuing aggressive international expansion and cost-optimization efforts, making it difficult to sustain outsized market share gains.

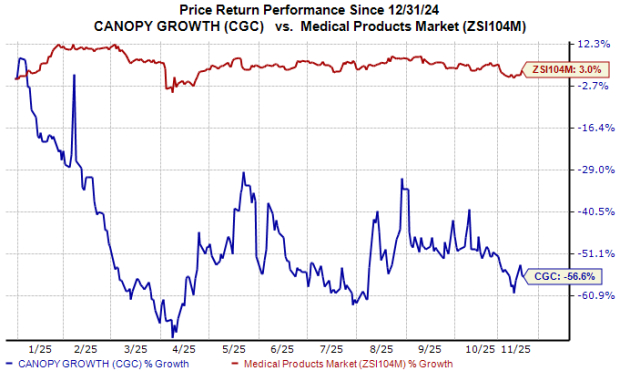

Shares of Canopy Growth have plunged 57% year to date against the industry’s 3% growth, as seen in the chart below.

Bottom-line estimates for fiscal 2026 and 2027 have improved significantly over the past 7 days.

While competitive pressures and international supply challenges remain near-term risks, rising sales and improving profitability signal that Canopy’s turnaround efforts are gaining traction. Upward revisions in bottom-line estimates further suggest that sentiment toward the stock is turning more constructive, reflecting growing analyst optimism around its operational progress.

In addition, recent comments from President Trump supporting marijuana rescheduling have reignited optimism across the sector, potentially setting the stage for a more favorable policy environment. For investors seeking selective exposure to the cannabis recovery trend, this Zacks Rank #3 (Hold) stock could warrant a closer look.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 hours | |

| 14 hours | |

| 15 hours | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite