|

|

|

|

|||||

|

|

|

Rio Tinto RIO reported iron ore shipments from Pilbara (on a 100% basis) of 84.3 million tons (Mt) for the third quarter of 2025. It was flat year over year but marked a 6% sequential rise. Despite major maintenance and infrastructure work, this marked Pilbara’s second-highest third-quarter performance since 2019.

Production was also stable year over year at 84.1 MT (on a 100% basis). Gudai-Darri achieved its highest-ever quarterly production in the quarter, with a 51 Mtpa run rate.

RIO’s peer Vale S.A. VALE produced 94.4 MT of iron ore in the third quarter, 3.8% higher than the year-ago quarter. VALE expects iron ore production in 2025 to range between 325 MT and 335 MT.

Bauxite production rose 9% year over year to 16.4 Mt in the third quarter. This marked the second consecutive quarterly production record with Amrun continuing to operate above nameplate capacity.

Rio Tinto’s aluminum output was up 6% year over year to 0.86 Mt. Alumina output was 1.9 MT, up 7% year over year, driven by improving performance at Yarwun and Alumar, partially offset by a planned shutdown at Vaudreuil.

In the third quarter, copper production was 204 thousand tons, 10% higher than the year-ago quarter. Oyu Tolgoi delivered a record copper production, despite a planned concentrator shutdown in September. Output was also higher at Escondida, but was offset by lower output at Kennecott as it navigates challenging geotechnical conditions impacting the south wall of the mine.

Rio Tinto expects Pilbara iron ore shipments (100% basis) to be at the lower end of 323-338 Mt. The range indicated a year-over-year decline of 2% to growth of 3%. The lowered guidance reflects the impact of cyclones in the first quarter. Also, Pilbara iron ore guidance remains subject to the timing of approvals for planned mining areas and heritage clearances.

Bauxite production targeted range is 59-61 MT (revised from 57-59 Mt), which reflects consistently higher utilization rates, particularly at Weipa. The company had produced 58.7 Mt of bauxite in 2024.

Alumina production is anticipated between 7.4 Mt and 7.8 Mt, suggesting growth from the reported output of 7.3 Mt in 2024. Aluminum production is expected to be 3.25-3.45 Mt, whereas it produced 3.3 Mt in 2024.

Rio Tinto expects copper production to come in near the high end of its stated range of 780-850 kt for 2025, attributed to a strong ramp-up at Oyu Tolgoi. The company reported total copper production (mined and refined) of 792.6 kt in 2024.

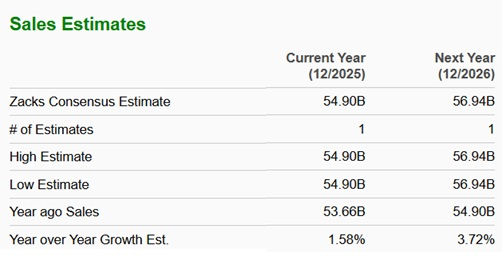

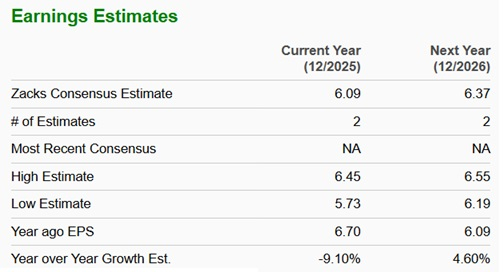

The Zacks Consensus Estimate for RIO’s 2025 revenues is pegged at $54.90 billion, suggesting a 1.6% year-over-year uptick. The estimate for earnings for 2025 is pegged at $6.09 per share, projecting a 9.1% decline.

The estimate for revenues for 2026 suggests a 3.72% year over year increase to $56.94 billion. The estimate for earnings of $6.37 projects 4.6% growth.

Notably, analyst earnings revisions for both 2025 and 2026 have trended upward, signaling growing optimism about Rio Tinto’s earnings trajectory.

Shares of Rio Tinto have gained 21.6% year-to-date compared with the industry's 26.5% growth. The Basic Materials sector has gained 23.3%, while the S&P 500 has risen 18.2% in the same timeframe.

Peers VALE, BHP Group BHP and Freeport-McMoRan Inc. FCX have gained 40.7%, 15.4% and 9.7%, respectively, so far this year.

RIO operates across 35 countries with a portfolio including iron ore, copper, aluminum and a range of other minerals, The company is focusing on new projects that can support the energy transition, currently exploring seven commodities in 17 countries.

Rio Tinto is working on building its lithium portfolio to capitalize on the rising demand for batteries and electric vehicles. The acquisition of Arcadium Lithium (Rio Tinto Lithium) earlier this year establishes Rio Tinto as a global leader in the supply of energy transition materials and a major lithium producer. It currently boasts one of the world’s largest lithium resource bases. Rio Tinto Lithium aims to grow the capacity of its Tier 1 assets to more than 200 thousand tons per year of lithium carbonate equivalent (LCE) by 2028

Its ongoing capital investment has delivered four consecutive years of production growth. The company remains on track to deliver on its 3% CAGR production over 2024-2033.

Rio Tinto trades at a forward price-to-earnings multiple of 11.23, lower than the industry's 16.43. The company is also trading at a discount compared with BHP Group’s 14.21X and and Freeport-McMoRan’s 22.11X. Vale is, however, trading lower at 6.51X.

Rio Tinto’s near-term shipment guidance may be tempered by operational headwinds, yet its diversified portfolio, project pipeline and lithium expansion poise it well for the energy transition trends.

With upward earnings revisions, attractive valuation and a Zacks Rank #2 (Buy), RIO presents a solid case for investors seeking exposure to global metals growth. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite