|

|

|

|

|||||

|

|

|

Walmart Inc. WMT and Target Corporation TGT stand as two of the most recognized names in the U.S. retail industry. While they share similarities in scale and omnichannel ambitions, their business models and strategic focuses remain distinctly different.

Walmart’s foundation rests on unparalleled global scale and operational reach. The company operates more than 10,500 stores across 19 countries, spanning its flagship Walmart U.S. segment, Sam’s Club, and Walmart International. Its business model centers on “everyday low prices” — a value-driven approach that continues to attract a broad customer base across income levels. The company boasts a market capitalization of about $817 billion.

Target, with a market cap of $41.2 billion, operates nearly 2,000 stores across the United States, strategically positioned to serve as both retail destinations and fulfillment centers. Its model blends style and affordability, offering a curated mix of essentials, apparel, home goods and discretionary categories — all underpinned by a strong owned-brand portfolio that exceeds $30 billion in annual sales.

As consumers tighten spending amid tariff pressures and ongoing cost inflation, the question is: Which of these retail giants is better positioned to sustain growth?

Walmart has evolved far beyond its brick-and-mortar roots. It has built one of the largest omnichannel ecosystems in the world, using its store network as fulfillment hubs for pickup and same-day delivery. This integration of digital and physical assets has enhanced convenience while keeping last-mile costs competitive. E-commerce remains a key growth lever, supported by initiatives like Walmart Marketplace and its third-party fulfillment services.

Complementing its retail strength are newer, higher-margin businesses such as Walmart Connect (advertising), Walmart+ (membership) and financial services offerings. These ventures are transforming Walmart’s profit profile, helping diversify earnings beyond merchandise sales. Its membership base also strengthens customer loyalty and recurring income streams, reinforcing the company’s ecosystem advantage.

Technology and automation continue to be central to Walmart’s long-term strategy. From AI-driven inventory systems to supply-chain digitization and advanced analytics, Walmart’s investments aim to enhance productivity, improve in-stocks and preserve its price leadership despite tariff-related cost pressures. The company’s international operations, including growth markets like Mexico, China, and India (Flipkart), provide additional expansion avenues and geographic diversification.

In the second quarter of fiscal 2026, Walmart’s consolidated sales rose 5.6% at constant currency, with global e-commerce up 25%. Advertising revenues soared 46% globally (with Walmart Connect up 31%), while membership income grew 15% in the quarter, led by Walmart+ and Sam’s Club Plus tiers.

However, Walmart faces persistent challenges, including higher goods costs due to tariffs, rising claims expenses, and moderation in discretionary spending among middle- and lower-income households. Yet, with a diversified model, strong balance sheet, and growing share in e-commerce and advertising, the company appears well-equipped to manage these pressures.

Target’s strength lies in merchandising and brand experience. Its stores are designed to inspire discovery, appealing to shoppers who value convenience but also seek design and quality. The company’s private-label brands — such as Cat & Jack, Good & Gather and Threshold — reinforce its differentiation and provide margin stability. Target also partners with major brands to enhance in-store excitement and exclusivity.

Digitally, Target has built a highly efficient fulfillment engine that integrates online and store-based operations. Services like Drive Up, Order Pickup and same-day delivery through Target Circle 360 (its expanded loyalty and membership ecosystem) have become critical components of its omnichannel strategy. These offerings leverage its store base to lower delivery costs and sustain traffic even as online sales grow.

In the second quarter of fiscal 2025, comparable sales declined 1.9%, marking a notable sequential improvement from the prior quarter’s steeper drop. However, digital sales went up 4.3%, fueled by strong demand for same-day fulfillment, which rose more than 25%.

Strategically, Target is focused on improving efficiency, accelerating technology adoption, and enhancing product freshness and availability. Investments in AI-based forecasting, inventory automation, and supply-chain modernization aim to improve execution and speed. Initiatives like “Fun 101” — which refresh product assortments with trend-led innovation — demonstrate Target’s effort to reclaim its merchandising leadership.

Still, Target faces near-term headwinds. Its discretionary-heavy mix makes it more exposed to fluctuations in consumer sentiment. Tariff-related cost pressures, competitive pricing dynamics, and higher promotional intensity also weigh on margins. However, the company’s brand equity, loyal customer base and strong store network provide a sturdy platform for recovery once macro conditions stabilize.

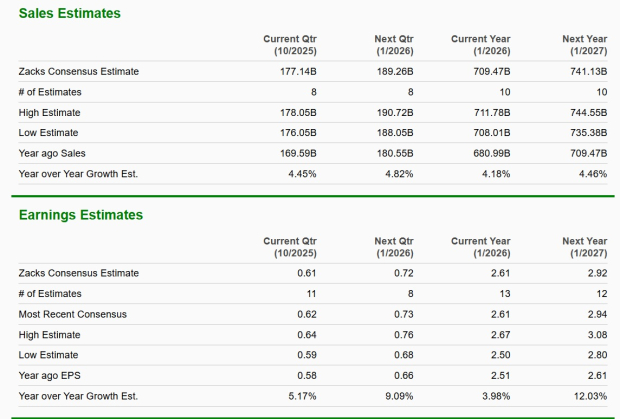

The Zacks Consensus Estimate for Walmart’s current fiscal-year sales and EPS suggests a year-over-year increase of nearly 4% each. The consensus estimate for EPS for the current fiscal year has increased by a penny to $2.61 over the past 60 days.

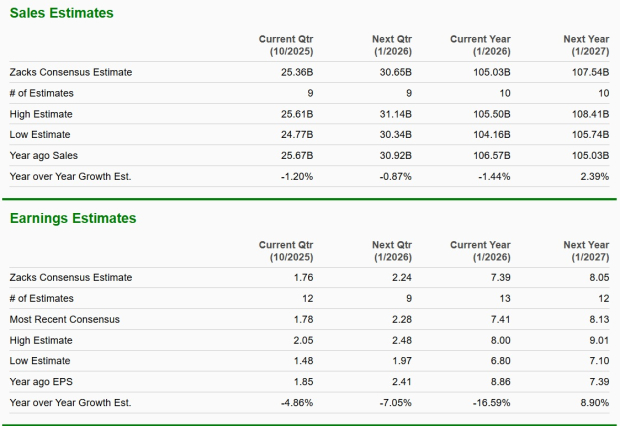

The Zacks Consensus Estimate for Target’s current fiscal-year sales and EPS implies year-over-year declines of 1.4% and 16.6%, respectively. The consensus estimate for EPS for the current fiscal year has declined from $7.45 to $7.39 over the past 60 days.

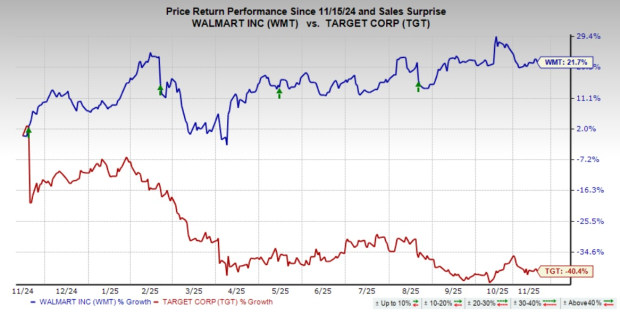

Over the past year, shares of Walmart have gained 21.7%, while Target has slumped 40.4%. Based on recent performance, Walmart appears to be the stronger pick.

Walmart’s forward P/E of 35.88 sits above its median of 35.67. Target is trading at a forward 12-month price-to-earnings (P/E) ratio of 11.4, below its one-year median of 12.44. On valuation grounds, Target looks better, as its forward P/E is below its historical median, signaling relative undervaluation compared to Walmart’s premium multiple above its median.

Walmart and Target remain integral forces in U.S. retail, yet their paths forward differ meaningfully. Walmart’s unmatched scale, strong e-commerce growth, and expanding profit engines in advertising and membership provide stability and consistent earnings visibility. Meanwhile, Target retains a powerful brand identity and an improving digital and supply-chain foundation, but near-term growth is constrained by discretionary weakness and margin pressure. While Target offers valuation appeal, Walmart currently stands as the stronger contender, backed by diversified growth drivers, global reach and proven operational resilience.

WMT and TGT each carry a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite