|

|

|

|

|||||

|

|

|

Palantir's valuation is far above what investors witnessed at the peak of the dot-com bubble.

UnitedHealth stock sold off earlier this year amid some operational headwinds.

Warren Buffett bought the dip in UnitedHealth stock.

Despite some volatility earlier in the year, 2025 has shaped up to be another impressive year for artificial intelligence (AI) stocks. Per usual, data analytics platform Palantir Technologies (NASDAQ: PLTR) has remained one of the best AI stocks -- with shares surging 130%.

One sector that has been relatively weak this year, however, is health insurance. Among notable laggards is UnitedHealth Group (NYSE: UNH), whose share price plummeted by 36% so far this year -- making it the poorest-performing stock in the Dow Jones Industrial Average (DJINDICES: ^DJI).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Despite these lackluster returns, Warren Buffett decided to buy the dip in UnitedHealth Group earlier this year -- adding roughly 5 million shares to Berkshire Hathaway's portfolio.

Let's unpack why Palantir's historic rally may come to an end sooner than investors realize. In addition, I'll explain the factors that caused UnitedHealth Group to sell off in the first place and make the case for why the stock looks like a bargain right now.

Image source: Getty Images.

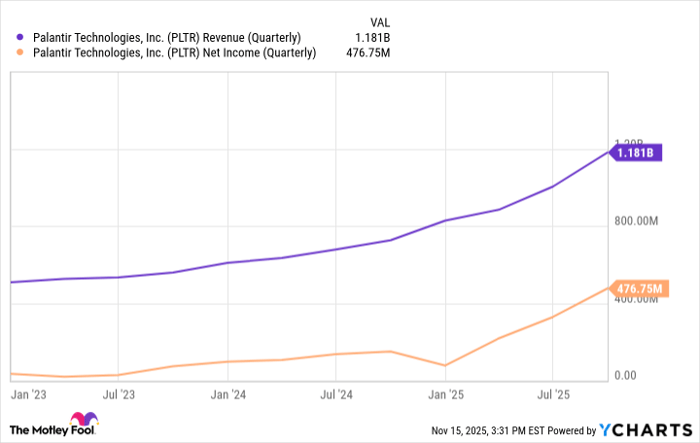

If the snapshot below is any indication, the AI revolution has been a transformative catalyst for Palantir. Over the last three years, the company's AI-powered software suite -- comprised of the Foundry, Apollo, and Gotham platforms -- has witnessed exponential demand from both government agencies and private sector enterprises.

Data by YCharts.

Moreover, Palantir's transition to profitability underscores how lucrative the AI market has been for the data mining darling. These positive -- and improving -- unit economics help Palantir stand out in a fiercely competitive software landscape. The company has done a stellar job rivaling larger incumbents like Salesforce and SAP, and its operational momentum doesn't appear to be slowing down.

While I can applaud Palantir's business performance, my reservations stem from something else entirely: Valuation.

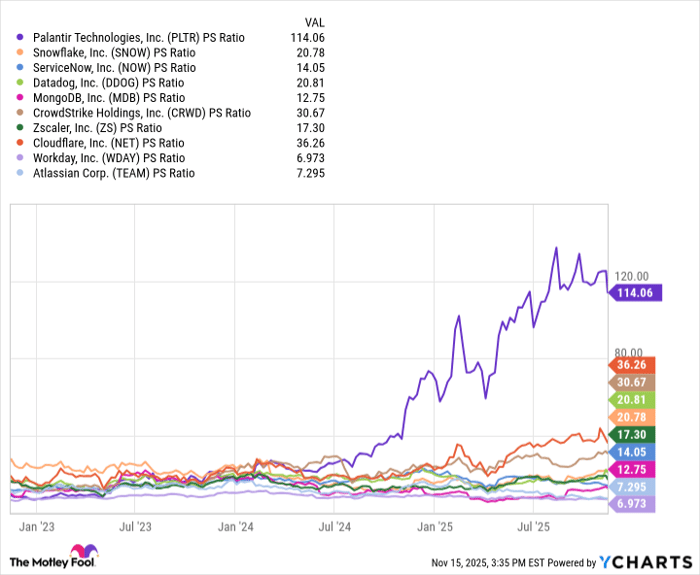

Data by YCharts.

In the analysis above, I've benchmarked Palantir against a comprehensive cohort of leading software businesses. Not only is Palantir's price-to-sales (P/S) ratio of 114 magnitudes higher than any other company in the peer group, but it's also expanding at a notable pace.

Generally speaking, as valuations soar, so do investor expectations. This can be a hard needle to thread in the long run because even if Palantir delivers a blowout quarter, the company increasingly faces the risk of not delivering on lofty -- and likely unrealistic -- expectations. As a result, the stock could enter a prolonged sell-off.

Moreover, Palantir's current valuation multiples far exceed what investors witnessed during the dot-com bubble in the late 1990s. In my eyes, it's this relationship that may have inspired famed hedge fund investor Michael Burry to short Palantir.

Although Palantir could still be a long-term winner of the AI revolution, I think shares face the risk of a pronounced correction. It could take years before Palantir stock climbs back (or above) its current valuation.

Over the next five years, I think Palantir stock could normalize quite dramatically as a valuation de-rating seems almost inevitable at this point.

UnitedHealth's downward spiral occurred earlier this year after the company reduced its financial guidance. The cause behind the company's lower earnings forecast had two influences:

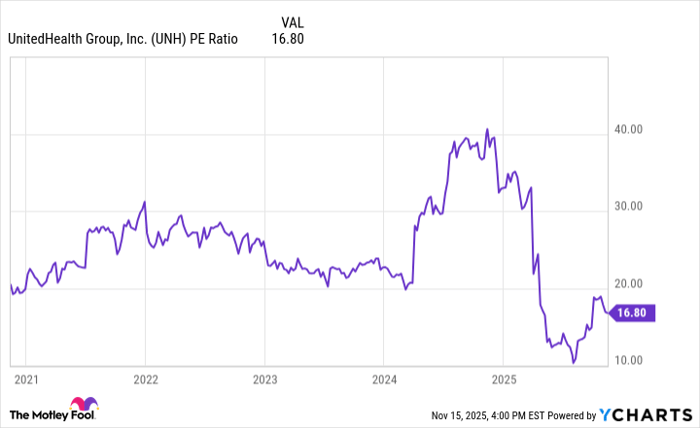

Although it may take several quarters for investors to start seeing a return to accelerating revenue and earnings growth, UnitedHealth's sell-off may have been overblown. My reasoning for this is that the company's price-to-earnings (P/E) multiple of 16.8 is hovering near five-year lows. Despite its operational turbulence, UnitedHealth's cratering valuation dynamics seem a bit exaggerated given the company still provides a mission-critical service in health insurance.

Data by YCharts.

Moreover, I think UnitedHealth could wind up being a stealthy beneficiary of AI over the next several years. Large language models (LLMs) have the ability to scan medical bills as well as digest volumes of ever-changing legislation in real time. These capabilities could prove useful in forecasting important business functions, such as utilization rates broken down by geographic and age demographics.

Lastly, in the midst of UnitedHealth's sell-off, several insiders were buying the stock alongside Buffett. The combination of a turnaround plan, insider buying, Berkshire's institutional approval, and the potential tailwinds of AI makes a compelling setup for a bounce back in UnitedHealth over the next several years.

As of this writing, UnitedHealth boasts a market capitalization of $291 billion -- about 43% below Palantir's market value.

While that's a meaningful disparity, I think UnitedHealth has the right mix of appropriate investor expectations combined with macro tailwinds that could ignite a period of robust valuation expansion. By contrast, Palantir is trading at unsustainable levels and appears due for a healthy pullback.

Against this backdrop, I think UnitedHealth stock is a rare combination of both growth and value in an otherwise frothy stock market. For these reasons, I see UnitedHealth Group as a no-brainer opportunity for investors with a long-term horizon.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $599,785!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,165,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,035% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 17, 2025

Adam Spatacco has positions in Palantir Technologies. The Motley Fool has positions in and recommends Atlassian, Berkshire Hathaway, Cloudflare, CrowdStrike, Datadog, MongoDB, Palantir Technologies, Salesforce, ServiceNow, Snowflake, Workday, and Zscaler. The Motley Fool recommends UnitedHealth Group. The Motley Fool has a disclosure policy.

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 4 hours | |

| 8 hours | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite