|

|

|

|

|||||

|

|

|

DraftKings Inc.’s DKNG third-quarter 2025 results may have sparked fresh concerns, but it insists the long-term profitability trajectory remains intact.

In third-quarter 2025, revenues rose 4% year over year to $1.14 billion, though customer-friendly sports outcomes created a more than $300 million revenue drag and weighed on adjusted EBITDA, which came in at negative $127 million. Management emphasized that these swings are temporary and will normalize over time.

Despite the headline miss, underlying business fundamentals appear strong. DraftKings continues to improve its sportsbook net revenue margin through a higher parlay mix and more efficient promotions while maintaining high customer retention. Handle growth accelerated into October, with sportsbook wagering up 17% from the prior year, supporting confidence in margin expansion ahead of 2026.

Importantly, the company reiterated that it expects to generate $450-$550 million in positive adjusted EBITDA in 2025, after swinging from a nearly $1 billion EBITDA loss in 2022, an indicator that the profitability model remains scalable. Partnerships with ESPN and NBCUniversal and the rollout of Spanish-language capabilities are expected to deepen engagement and expand DraftKings’ addressable market.

Looking to 2026, management highlighted incremental upside from its upcoming launch of DraftKings Predictions, allowing entry into states that still lack online sports betting. While investment will be measured and data-driven, the initiative could unlock a “significant incremental opportunity” and pressure more states to adopt full-scale regulated betting, further strengthening the path to sustainable profits.

In short, while quarterly volatility remains part of the playbook, DraftKings’ execution, market share momentum and product expansion suggest it is still driving toward durable profitability in 2026.

As DraftKings advances toward sustained profitability, competitive dynamics will continue to shape its path. Flutter Entertainment plc’s FLUT FanDuel remains the U.S. market leader in online sports betting, supported by a proven parlay-driven margin strategy and tighter promotional discipline. Its earlier scale advantages have enabled more consistent profitability, creating a high bar for DraftKings to meet in terms of efficiency and long-term margin expansion.

Meanwhile, BetMGM, operated via MGM Resorts International MGM and Entain plc, is leaning on omnichannel benefits, integrating its land-based casino ecosystem with online wagering. This provides a powerful cross-selling engine, especially in iGaming, where BetMGM holds a strong position.

As industry growth shifts from expansion to optimization, DKNG must continue to sharpen product innovation, enhance hold rates and strategically invest in marketing to remain on track for sustainable profitability into 2026.

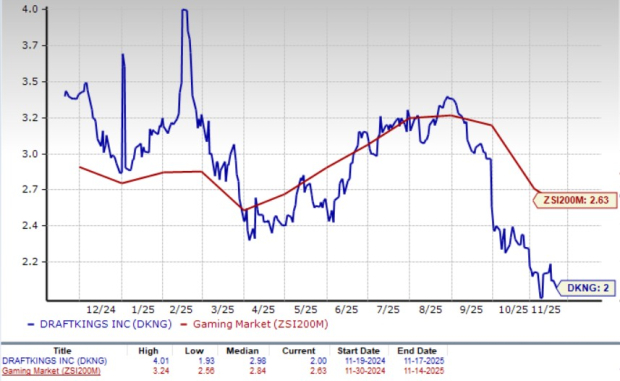

Shares of DKNG have lost 36% in the past three months compared with the industry’s decline of 7.6%.

DraftKings is currently trading at a discount compared with the industry peers, with a forward 12-month price-to-sales ratio of 2.0X.

The Zacks Consensus Estimate for DKNG’s 2025 and 2026 has declined in the past 30 days.

DKNG currently carries a Zacks Rank #5 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-27 | |

| Mar-27 | |

| Mar-25 | |

| Mar-24 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite