|

|

|

|

|||||

|

|

|

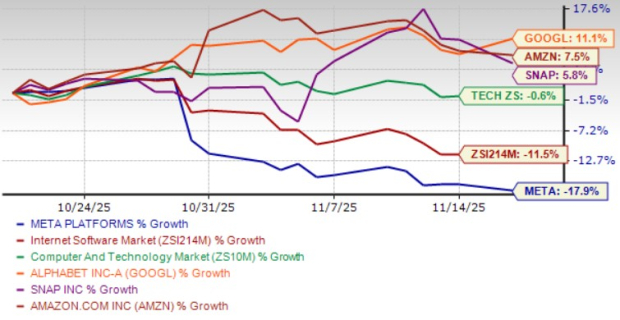

Meta Platforms’ META shares have dropped 17.9% in the past month, underperforming the broader Zacks Computer & Technology sector, as well as its advertising peers, including Amazon AMZN, Alphabet GOOGL and Snap SNAP. Meta Platforms, Alphabet and Amazon are expected to absorb more than 50% of the projected global ad spending this year and 56.2% in 2026.

Shares of Alphabet, Amazon, and Snap have appreciated 11.1%, 7.5% and 5.8%, respectively. The broader sector dropped 0.6% over the same time frame.

The decline in META’s share price can be attributed to its growing capital expenditure. The company now expects between $70 billion and $72 billion compared with the previous guidance of $66-$72 billion range. Per CNBC, Alphabet, Meta Platforms, Amazon and Microsoft on a combined basis are expected to spend roughly $380 billion on developing AI infrastructure in 2025.

So, what should you do with the META stock right now? Let’s find out.

META’s focus on integrating AI into its platforms — Facebook, WhatsApp, Instagram, Messenger and Threads — is driving user engagement to boost ad revenues. AI is heavily dependent on data, of which META has a trove, driven by its more than 3.54 billion daily users, including 3 billion monthly actives on Instagram and 150 million daily actives on Threads. The ranking optimizations Meta Platforms made in the third quarter of 2025 drove a 10% increase in time spent on Threads. In the United States, overall time spent on Facebook and Instagram grew in double digits year over year, driven by continued video strength as well as healthy growth in non-video time on Facebook.

AI recommendations that deliver higher quality and more relevant content are driving engagement. In the third quarter of 2025, time spent on Facebook increased 5% and 30% more on Threads. Reels now has an annual run rate of more than $50 billion as videos continue to grow across Meta Platforms’ apps. Vibes, META’s next-generation AI creation tools and content experience, is gaining traction. META is using Meta AI (currently used by more than one billion people) to boost user experience. Business AI is also gaining traction with more than one billion active threads between people and businesses across the company’s messaging platforms.

The ad business is benefiting from an improved AI ranking system. Annual run rate for META’s complete end-to-end AI-powered ad tools has passed $60 billion. In the third quarter of 2025, the average price per ad increased 10% year over year, benefiting from increased advertiser demand, largely driven by improved ad performance. The company has a strong pipeline of ad supply opportunities on both Threads and WhatsApp Status over the long term. Ads are now running globally in Feed on Threads, and META plans to optimize the ad formats and performance before increasing supply.

META’s Advantage+ creative suite is gaining traction, with the number of advertisers using at least one of its video generation features going up 20% on a sequential basis as adoption of image animation and video expansion continues to scale. The addition of more generative AI features is making it easier for advertisers to optimize their ad creatives and drive increased performance. Meta Platforms introduced AI-generated music for advertisers in the third quarter of 2025.

The Zacks Consensus Estimate for fourth-quarter 2025 earnings is pegged at $8.16 per share, up 0.7% over the past 30 days, suggesting 1.75% growth from the figure reported in the year-ago quarter.

Meta Platforms, Inc. price-consensus-chart | Meta Platforms, Inc. Quote

Meta Platforms expects fourth quarter 2025 total revenues to be in the range of $56-59 billion. The consensus mark for fourth-quarter 2025 revenues is pegged at $58.43 billion, indicating 20.76% growth from the figure reported in the year-ago quarter.

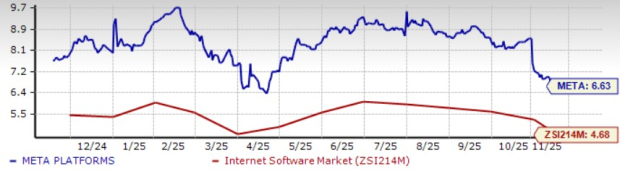

META shares are overvalued, as suggested by the Value Score of C. In terms of the forward 12-month price/sales (P/S), META is trading at 6.63X, a premium compared with the Zacks Internet Software industry’s 4.68X, Amazon’s 3.18X, and Snap’s 2.13X.

Meta Platforms is spending heavily on expanding AI infrastructure, which, along with the company’s heavy usage of AI across its platforms, is expected to boost user engagement, eventually driving top-line growth. However, stiff competition in the ad market and a stretched valuation are headwinds.

META currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 28 min | |

| 35 min | |

| 43 min | |

| 44 min | |

| 1 hour | |

| 1 hour |

Globalstar Stock Jumps After Report Amazon Is In Talks To Acquire Satellite Firm

AMZN

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite