|

|

|

|

|||||

|

|

|

AbbVie’s ABBV reported third-quarter 2025 results on Oct. 31, before market open. The company beat estimates for both earnings and sales. While sales rose 9.1% year over year, earnings declined 38% due to costs related to acquisitions. AbbVie raised its revenue and EPS guidance for 2025 for the third time this year, backed by strong momentum year to date.

However, AbbVie’s stock declined post earnings release, probably due to softer sales of oncology drugs and continued weakness in its Aesthetics unit.

However, the stock has recovered after the Q3 dip and on Nov. 12, crossed the 50-day moving average. This may have confused investors about whether they should buy, sell or hold the stock post the dip.

Let’s understand the company’s strengths and weaknesses in detail to make a proper investment decision.

AbbVie lost patent protection for its blockbuster drug, Humira, in the United States in January 2023 and in the EU in 2018. Humira's sales are declining due to LOE and biosimilar erosion. However, AbbVie has successfully navigated the loss of exclusivity (LOE) of the drug, which once generated more than 50% of its total revenues. It has accomplished this by launching two other successful new immunology medicines, Skyrizi and Rinvoq, which are performing extremely well, bolstered by approvals in new indications, and should support top-line growth in the next few years.

Skyrizi and Rinvoq generated combined sales of $18.5 billion in the first nine months of 2025.

The drugs are seeing strong performance across all approved indications, especially in the popular inflammatory bowel disease (IBD) space, which includes two conditions — ulcerative colitis (UC) and Crohn’s disease (CD).

Skyrizi sales are now annualizing at almost $18 billion and Rinvoq at more than $8 billion. AbbVie expects to outperform its target of combined sales of Skyrizi and Rinvoq of more than $25 billion in 2025 and more than $31 billion by 2027. Strong immunology market growth, market share gains and momentum from new indications, such as the recent launch of Skyrizi in UC, as well as the potential for five new indications for Rinvoq over the next few years, are expected to drive these drugs’ growth.

AbbVie recently settled patent litigation with all generic manufacturers for Rinvoq, which extended the drug’s patent exclusivity by four years to 2037.

AbbVie has built a substantial oncology franchise with Imbruvica and Venclexta. Its oncology segment generated combined revenues of $5.0 billion in the first nine months of 2025, up 2.7% year over year as higher sales of Venclexta and contributions from new drugs, Elahere and Epkinly, more than offset the decline in Imbruvica sales. Some key oncology drugs approved in the past couple of years are Epkinly and Emrelis. Elahere was added to AbbVie’s oncology portfolio with the February 2024 acquisition of Immunogen. These three new drugs have strengthened AbbVie’s oncology franchise.

AbbVie’s neuroscience portfolio is also contributing to top-line growth. Sales of its neuroscience drugs increased 20.3% to almost $7.8 billion in the first nine months of 2025, driven by higher sales of Botox Therapeutic, depression drug Vraylar and newer migraine drugs Ubrelvy and Qulipta.

The initial international launch of Vyalev in Parkinson’s disease is encouraging, and the company’s Parkinson’s disease franchise, comprising Vyalev and once-daily oral treatment tavapadon (under review in the United States), is being seen as a key to growth in neuroscience.

Over the next couple of years. AbbVie expects new product approvals for tavapadon and pivekimab sunirine (blastic plasmacytoid dendritic cell neoplasm) and pivotal data readouts for key pipeline candidates, lutikizumab, Temab-A and etentamig. These pipeline programs have the potential to drive long-term growth for AbbVie, while Skyrizi and Rinvoq will boost near-term growth.

AbbVie has been on an inorganic growth track over the past couple of years to bolster its early-stage pipeline, which should drive long-term growth. Particularly, it is signing several M&A deals in the immunology space, its core area, while also entering into some early-stage alliances in oncology and neuroscience. AbbVie has executed more than 30 M&A transactions since the beginning of 2024. In a key recent deal, it acquired private biotech, Gilgamesh Pharmaceuticals' bretisilocin, a novel, investigational therapy for major depressive disorder. The agreement will strengthen its neuroscience pipeline.

Sales of Humira are declining due to biosimilar erosion. The launch of Humira biosimilars in the United States in 2023 significantly eroded the drug’s sales in 2024, with the decline being sharper in 2025 and expected to continue in 2026 as more plans excluded branded Humira and moved to exclusive biosimilar contracts. Humira sales declined more than 50% in the first nine months of 2025.

AbbVie is seeing decreasing sales of the Aesthetics unit. AbbVie’s global sales of its aesthetics portfolio declined 0.6% in 2024 and 7.4% in the first nine months of 2025.

Continued macro challenges and low consumer sentiment, especially in the United States, as concerns about the economy and inflation weigh on discretionary spending, are hurting aesthetics sales. Juvederm sales fell 14.6% in 2024 and 16.7% in the first nine months of 2025. Botox Cosmetics sales declined 7.4% in the first nine months of 2025. AbbVie now expects category growth to be below previous expectations.

On the third-quarter conference call, AbbVie lowered its expectation for its Aesthetics business from $5.1 billion to $4.9 billion due to greater-than-expected market softness globally.

ABBV stock has risen 31.6% this year so far compared with an increase of 14.2% for the industry. The stock has also outperformed the sector and the S&P 500 Index, as seen in the chart below.

From a valuation standpoint, AbbVie is reasonably priced. Going by the price/earnings ratio, the company’s shares currently trade at 16.74 forward earnings, lower than 16.81 for the industry. The stock is trading above its five-year mean of 13.36. AbbVie stock seems cheaper compared to other large drugmakers, such as Eli Lilly LLY, J&J JNJ and AstraZeneca AZN, following their results.

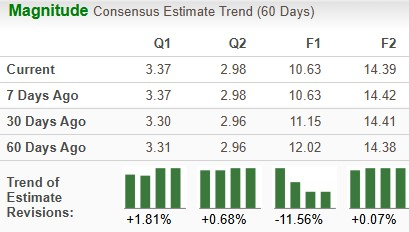

The Zacks Consensus Estimate for 2025 earnings has declined from $11.15 per share to $10.63, while that for 2026 has decreased from $14.41 to $14.39 per share over the past 30 days.

AbbVie combats its share of headwinds, like Humira LOE impact, increasing competitive pressure on Imbruvica and continued macro woes for Aesthetics. However, the company has faced its biggest challenge — Humira’s patent cliff — quite well and looks well-positioned for continued strong growth in the years ahead. AbbVie is returning to robust revenue growth in 2025, which is just the second year following the U.S. Humira LOE, driven by its ex-Humira platform.

Sales of AbbVie’s ex-Humira drugs rose more than 20% (on a reported basis) in the third quarter, which was above its expectations, driven by Skyrizi, Rinvoq and neuroscience.

Boosted by its new product launches, AbbVie expects to return to mid-single-digit revenue growth in 2025 with a high single-digit CAGR through 2029, as it has no significant LOE events for the rest of this decade. A substantial portion of this growth is expected to be driven by the robust performance of Skyrizi and Rinvoq. In the first nine months of the year, its total revenues rose 8.2%, in line with its expectation of mid-single-digit revenue growth. With no significant LOEs in this decade, AbbVie enjoys the flexibility to invest more in R&D to continue to acquire external innovation.

AbbVie recently increased its quarterly cash dividend by 5.5%. Though estimates have declined, we believe that it is due to costs related to acquisitions, which should eventually boost growth.

Rising stock price, a decent valuation, expectations for continued strong earnings growth and a robust pipeline are good enough reasons to stay invested in this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 17 min | |

| 33 min | |

| 47 min | |

| 57 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Novo Nordisk Files Deceptive Advertising Lawsuit Against Rival Eli Lilly

LLY

The Wall Street Journal

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite