|

|

|

|

|||||

|

|

|

What a time it’s been for Guardant Health. In the past six months alone, the company’s stock price has increased by a massive 171%, setting a new 52-week high of $106.25 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Guardant Health, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're cautious about Guardant Health. Here are three reasons there are better opportunities than GH and a stock we'd rather own.

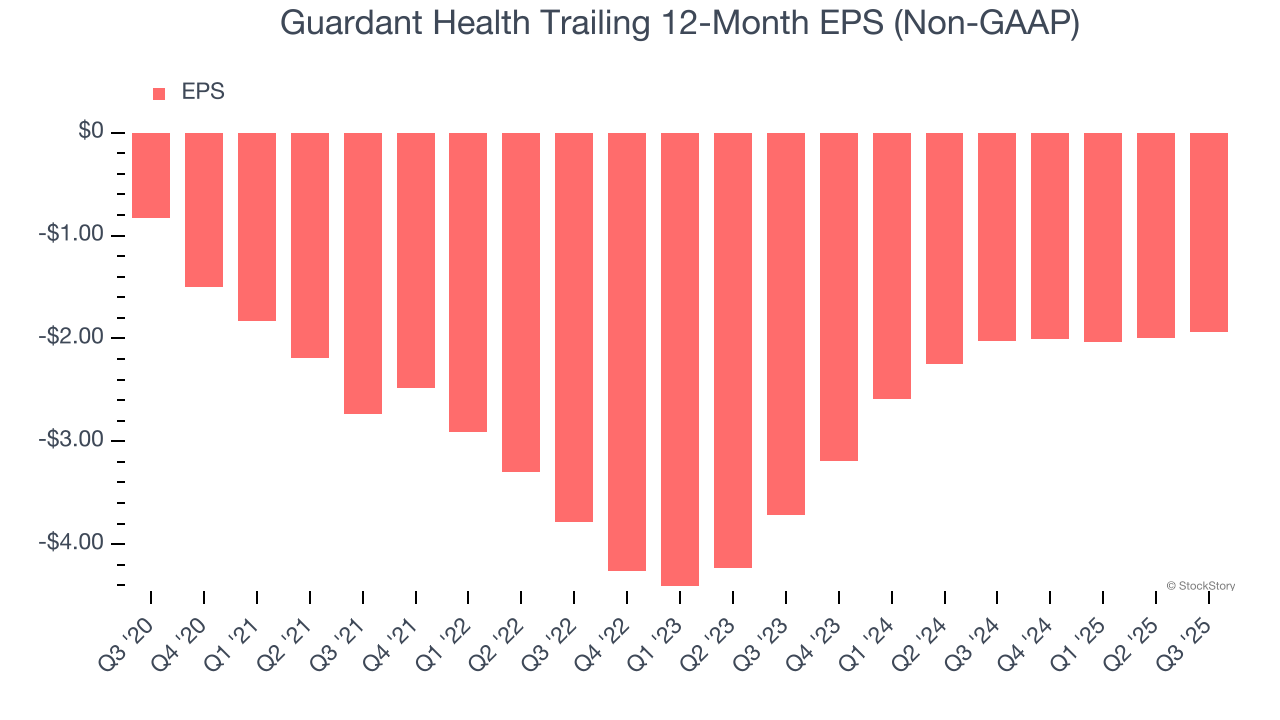

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Guardant Health’s earnings losses deepened over the last five years as its EPS dropped 18.5% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

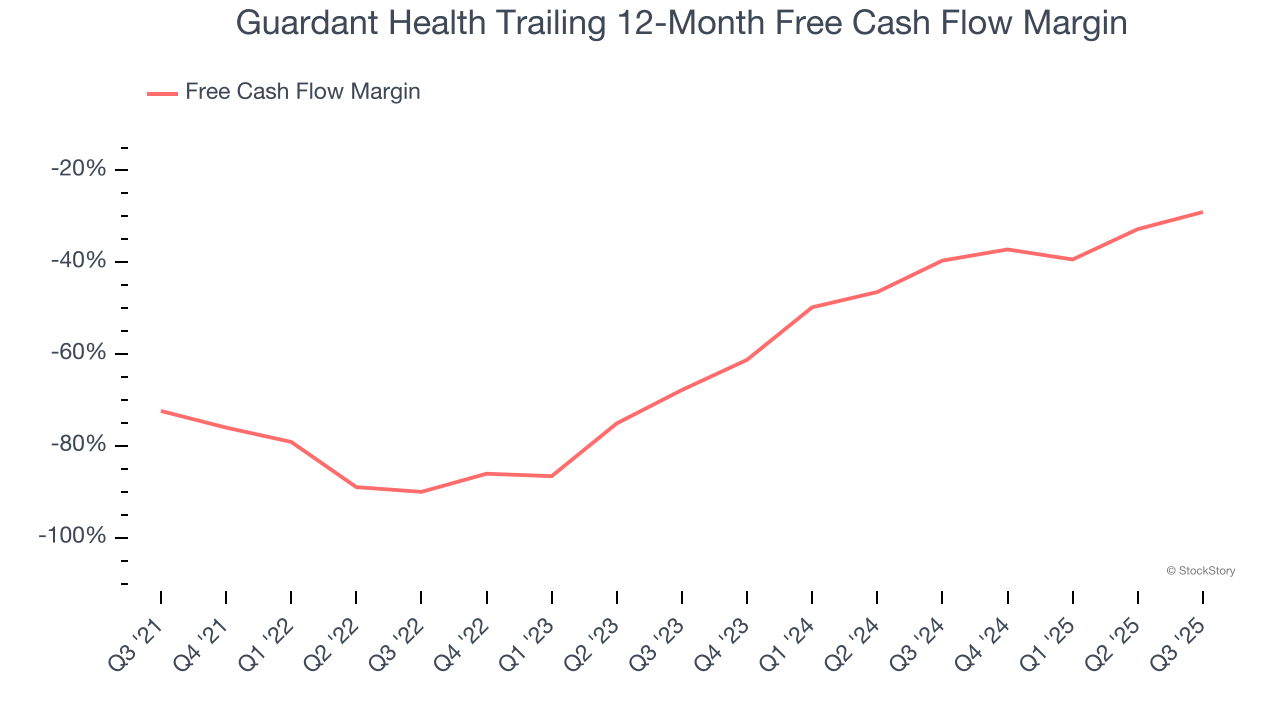

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Guardant Health’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 52.9%, meaning it lit $52.90 of cash on fire for every $100 in revenue.

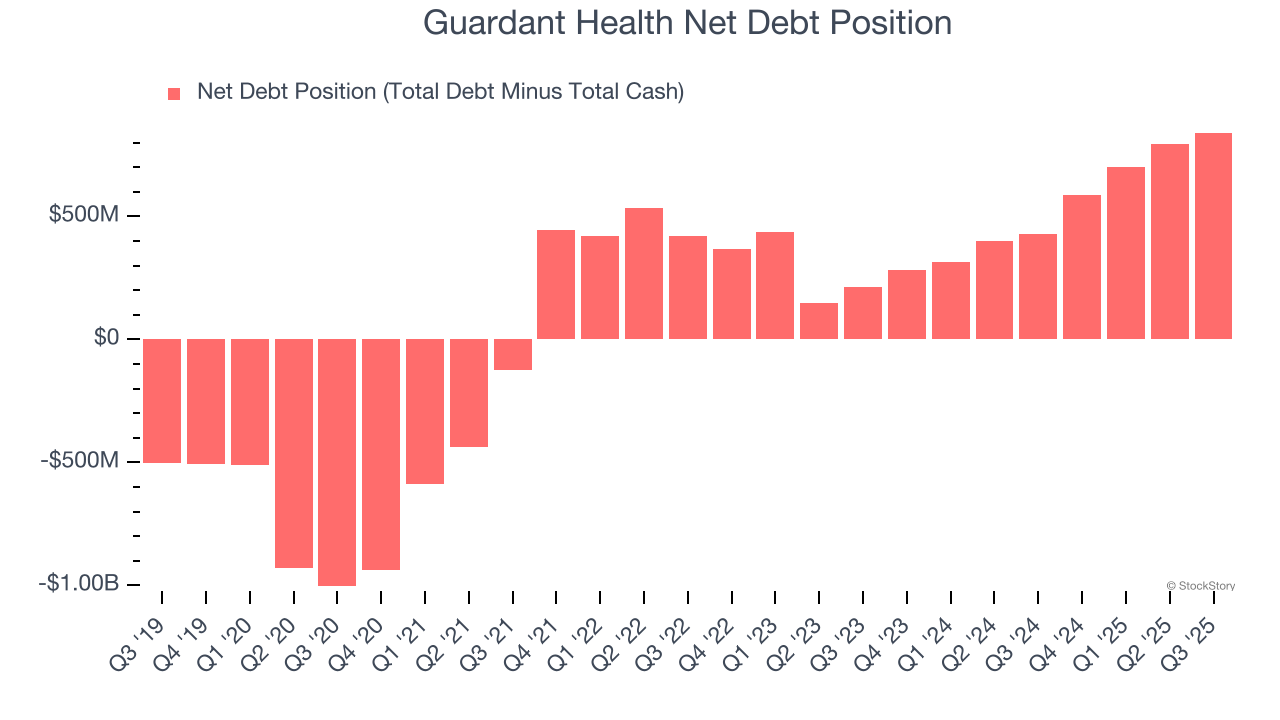

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Guardant Health posted negative $234.3 million of EBITDA over the last 12 months, and its $1.42 billion of debt exceeds the $580 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Guardant Health if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Guardant Health can improve its profitability and remain cautious until then.

Guardant Health isn’t a terrible business, but it doesn’t pass our bar. Following the recent rally, the stock trades at $106.25 per share (or a forward price-to-sales ratio of 10.8×). The market typically values companies like Guardant Health based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d recommend looking at the most entrenched endpoint security platform on the market.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 5 hours | |

| May-20 |

Guardant Health Leaps On A Major Win In Cancer Detection; Will Shares Break Out?

GH +17.09%

Investor's Business Daily

|

| May-20 | |

| May-18 | |

| May-07 | |

| May-07 | |

| May-06 | |

| May-04 | |

| Apr-30 | |

| Apr-29 | |

| Apr-16 | |

| Apr-08 | |

| Mar-30 | |

| Mar-30 | |

| Mar-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite