|

|

|

|

|||||

|

|

|

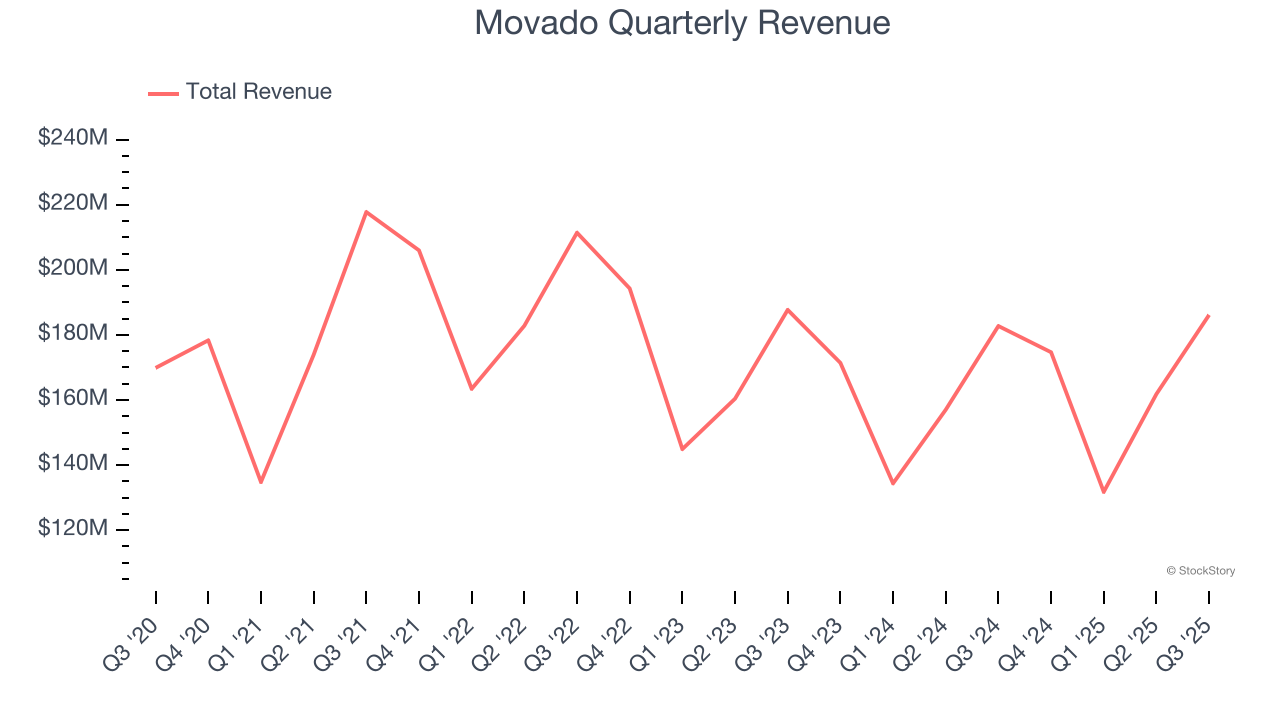

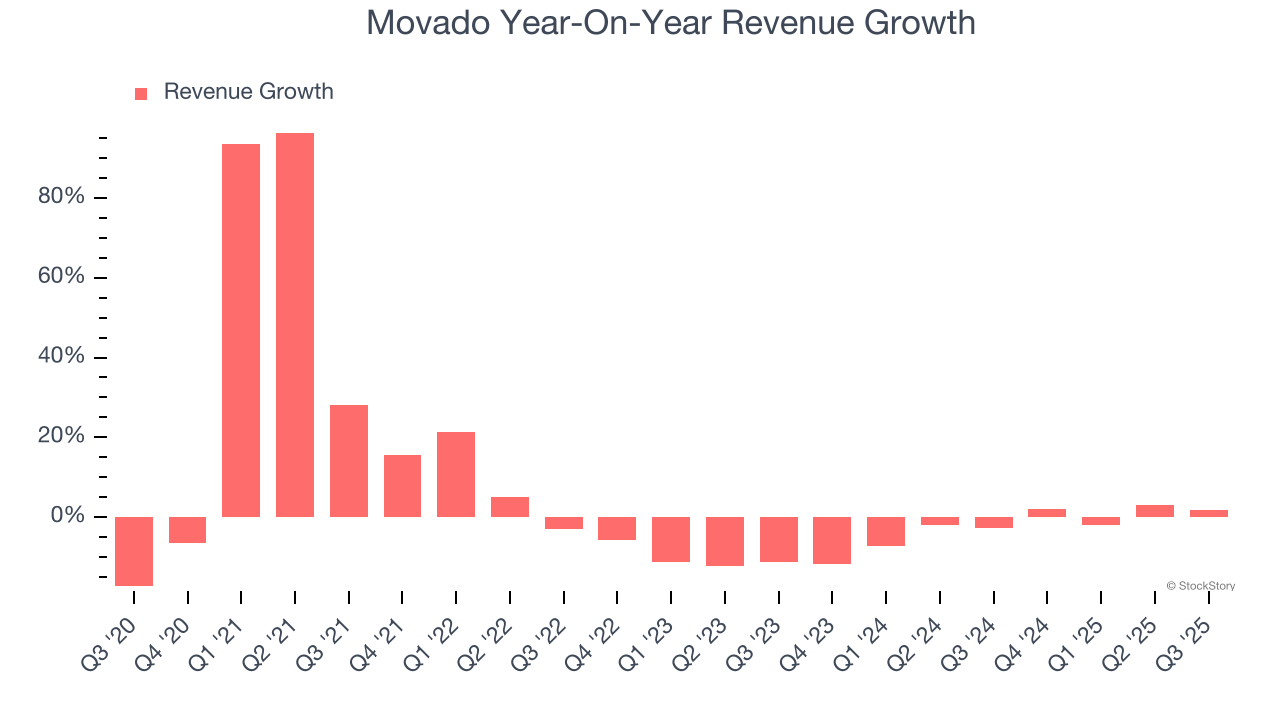

Luxury watch company Movado (NYSE:MOV) met Wall Streets revenue expectations in Q3 CY2025, with sales up 1.9% year on year to $186.1 million. Its GAAP profit of $0.42 per share was 26.8% below analysts’ consensus estimates.

Is now the time to buy Movado? Find out by accessing our full research report, it’s free for active Edge members.

Efraim Grinberg, Chairman and Chief Executive Officer, stated, “We are pleased with our third quarter results, delivering a 3% increase in net sales, 80 basis points of expansion in gross margin and a doubling in diluted earnings per share versus the third quarter last year, even as we absorbed material tariff cost increases in the period. We capitalized on the accelerating interest in the fashion watch category among younger consumers, delivering innovative watch and jewelry assortments that were strongly received across our iconic brands, especially in Europe and the United States. We achieved double-digit growth for the Movado brand in our direct-to-consumer channels, while continuing to optimize the brand's wholesale business, which we expect to return to growth in the fourth quarter.

With its watches displayed in 20 museums around the world, Movado (NYSE:MOV) is a watchmaking company with a portfolio of watch brands and accessories.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Movado’s 4.7% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Movado’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.4% annually.

This quarter, Movado grew its revenue by 1.9% year on year, and its $186.1 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

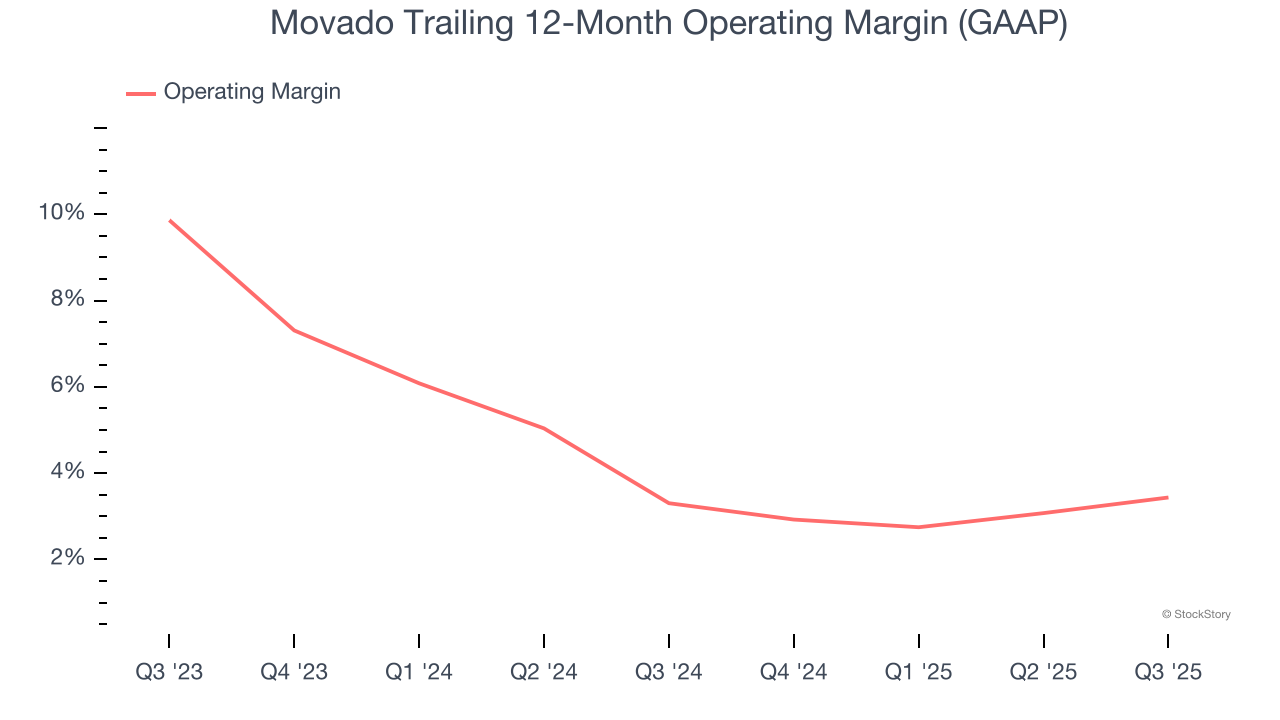

Movado’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 3.4% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Movado generated an operating margin profit margin of 6.3%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

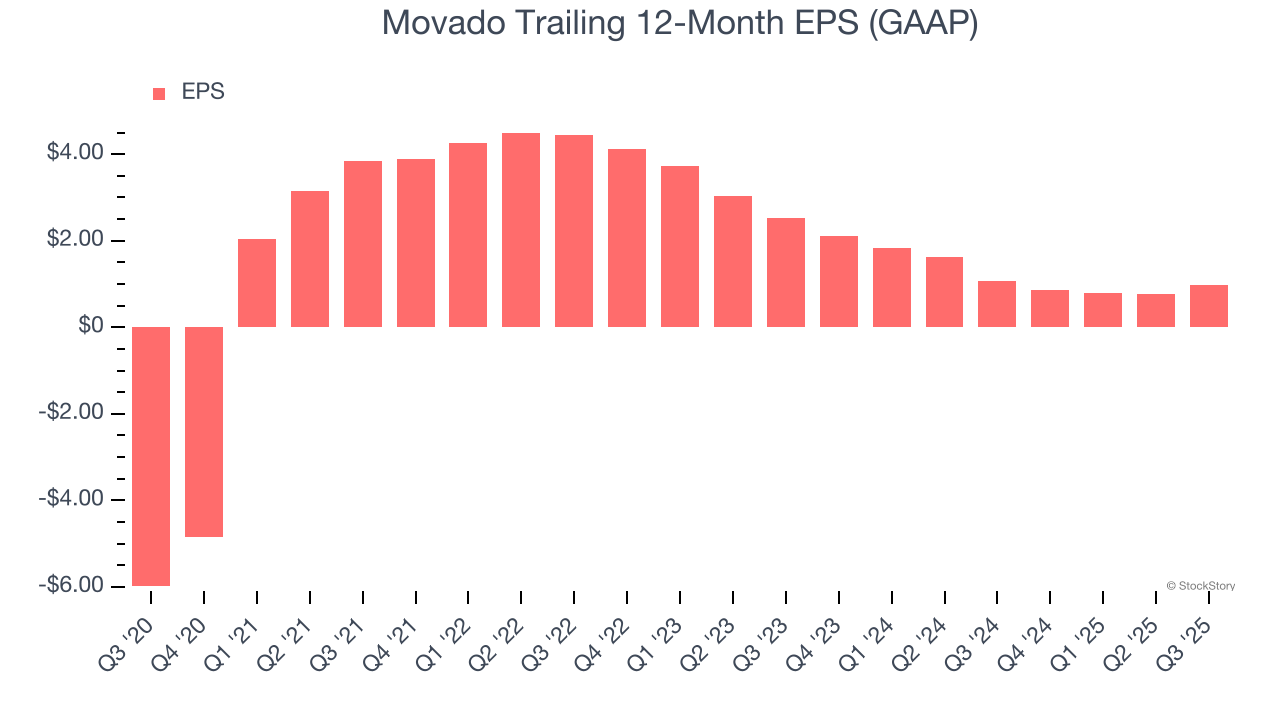

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Movado’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Movado reported EPS of $0.42, up from $0.22 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Movado’s full-year EPS of $0.97 to grow 111%.

We struggled to find many resounding positives in these results. Revenue was just in line and EPS missed. Overall, this was a weaker quarter. The stock remained flat at $19.49 immediately after reporting.

Is Movado an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-21 | |

| Jun-04 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-20 | |

| Mar-19 | |

| Mar-19 | |

| Mar-19 | |

| Mar-19 | |

| Mar-12 | |

| Mar-04 | |

| Feb-26 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite