|

|

|

|

|||||

|

|

|

Regency Centers Corp. REG is well-positioned to gain from its strategically located portfolio of premium shopping centers, concentrated in affluent suburban areas and near urban trade areas where consumers have high spending power. Its focus on grocery-anchored shopping centers ensures dependable traffic.

The company is witnessing solid demand for its centers in a healthy retail real estate environment, driving leasing activity, occupancy levels and rent growth. In the third quarter, Regency Centers executed around 1.8 million square feet of comparable new and renewal leases at a blended cash rent spread of 12.8%.

Strategic buyouts and an encouraging development pipeline bode well for long-term growth. However, growing e-commerce adoption raises concerns. High debt burden and geographic concentration of assets in select markets add to its woes.

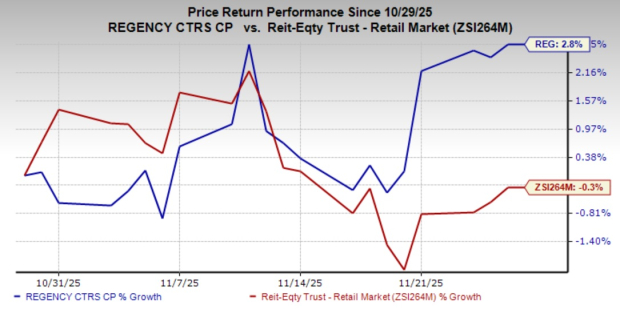

Shares of Regency have gained 2.8% in the past month against its industry’s decline of 0.3%. Analysts seem bullish on this Zacks Rank #3 (Hold) company. The Zacks Consensus Estimate for its 2025 and 2026 FFO per share has moved marginally northward over the past three months to $4.61 and $4.80, respectively.

Regency has a high-quality open-air shopping center portfolio, with more than 85% grocery-anchored neighborhood and community centers. This focus on building a premium portfolio of grocery-anchored shopping centers is a strategic fit because such centers are usually necessity-driven and attract dependable traffic. In uncertain times, the grocery component has benefited retail REITs, and Regency has numerous industry-leading grocers as tenants.

Regency’s premium shopping centers are situated in affluent suburban areas and near the urban trade areas where consumers have high spending power, enabling the company to attract top grocers and retailers. Furthermore, the best-in-class operators are opening new locations in its high-quality centers. Anchor tenants comprised 42% (based on pro-rata ABR) of its portfolio as of Sept. 30, 2025. Regency’s embedded rent escalators have also been a key driving factor behind its rent growth. In the third quarter of 2025, same-property base rents contributed 4.7% to same-property net operating income (NOI) growth.

Regency is making efforts to improve its portfolio with acquisitions and developments in key markets. In the third quarter of 2025, Regency Centers acquired a portfolio of five shopping centers located within the Rancho Mission Viejo master planned community in Orange County, CA, for $357 million. As of Sept. 30, 2025, Regency Centers’ in-process development and redevelopment projects have estimated net project costs of around $668 million at the company’s share. REG has incurred 51% of the cost as of the same date.

Regency is focused on strengthening its balance sheet. This retail REIT had $1.5 billion of capacity under its revolving credit facility as of Sept. 30, 2025. As of the same date, its pro-rata net debt and preferred stock-to-operating EBITDAre were 5.3, while the fixed charge coverage ratio was 4.2. Regency also enjoys a large pool of unencumbered assets. As of Sept. 30, 2025, 86.9% of its wholly owned real estate assets were unencumbered. Moreover, the investment-grade credit ratings of ‘A3’ from Moody’s and ‘A-’ with a stable outlook from S&P Global Ratings render it access to the debt market at favorable costs.

Solid dividend payouts are the biggest attraction for REIT investors, and Regency Centers is committed to boosting shareholder wealth. In October 2025, Regency declared a quarterly cash dividend payment on its common stock of 75.5 cents, an increase of 7.1% from the prior quarter's dividend. The company has hiked its dividend five times in the past five years, and its payout has grown 3.96% over the same time period. REG's payout ratio currently sits at 62% of earnings. Given the company’s solid operating platform, scope for growth and decent financial position compared to that of the industry, this dividend rate is expected to be sustainable over the long run. Check Regency Centers’ dividend history here.

The market is witnessing a shift in retail shopping from brick-and-mortar stores to internet sales. Particularly, the efforts of online retailers in recent years to go deeper into the grocery business have emerged as a concern for REG, which focuses on building a premium portfolio of grocery-anchored shopping centers.

This is expected to adversely impact the market share for brick-and-mortar stores. This is likely to lead to a lesser scope for the company to increase rents and hurt occupancy growth.

Regency has a substantial debt burden, with total debt of approximately $4.92 billion as of Sept. 30, 2025. With a high level of debt, interest expenses are likely to remain elevated. Interest expenses for the third quarter of 2025 jumped 9% year over year to $51.3 million.

Some better-ranked stocks from the REIT sector are Federal Realty Investment Trust FRT and Phillips Edison & Company, Inc. PECO. Both Federal Realty and Phillips Edison & Company carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Federal Realty’s 2025 FFO per share has been raised marginally over the past month to $7.23, suggesting a 6.8% increase year over year.

The consensus estimate for Phillips Edison’s 2025 FFO per share has been revised upward marginally to $2.58 over the past two months, calling for a rise of 6.2% year over year.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-02 | |

| Jul-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite