|

|

|

|

|||||

|

|

|

MercadoLibre has been a huge winner over its history.

The company has built a formidable set of competitive advantages.

The stock has fallen due to a competitive threat, setting up a good buying opportunity.

MercadoLibre (NASDAQ: MELI) doesn't get as much attention as some of its U.S.-based e-commerce counterparts, but the Latin American e-commerce operator has been a big winner for investors over the years.

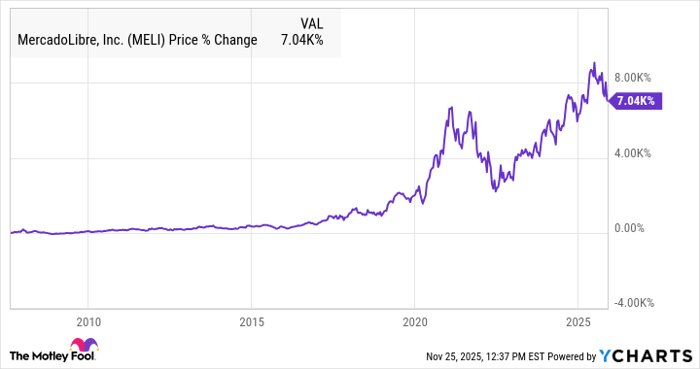

Since its 2007 initial public offering (IPO), the stock is up 7,000%, and it's been a winner over virtually any time frame during its history, as you can see from the chart below:

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Recently, however, MercadoLibre has pulled back due to concerns about increasing risk in its fintech division and signs that Amazon is ramping up competition in Latin America.

As a result, MercadoLibre stock is down 22% from its recent peak, giving investors an excellent opportunity to buy this historical winner. In fact, if you're looking to invest $2,000, MercadoLibre looks like a great fit, as its share price is currently hovering just above that level. Here's why it's a good use for that $2,000 right now.

Image source: MercadoLibre.

Founded in 1999 by Stanford business student Marcos Galperin, MercadoLibre got an early start on e-commerce in Latin America. It has been building on its base ever since, adding complementary businesses. These include Mercado Pago, which handles both online and offline payments, including through point-of-sale devices used by over a million merchants; Mercado Envios, its logistics division, which helps deliver 80% of orders within 48 hours; Mercado Crédito, its fast-growing credit arm, with a portfolio of more than $9 billion; and Mercado Fondo, its asset management division. Its e-commerce platform also includes both first-party direct sales and a third-party marketplace, giving it a reach similar to Amazon's.

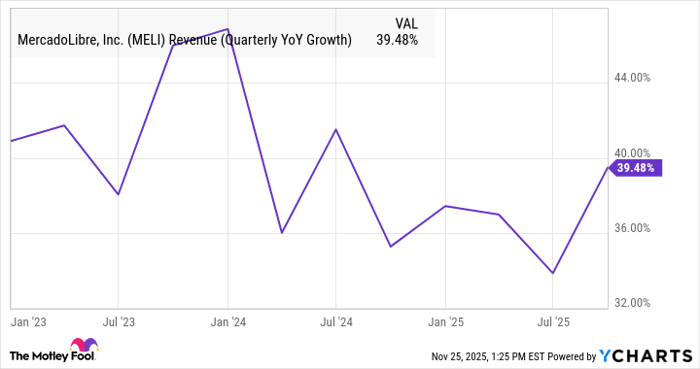

MercadoLibre's revenue jumped 39% in the third quarter to $7.4 billion, continuing a long streak of near-40% revenue growth, as the chart below shows. In fact, that was its 27th consecutive quarter of at least 30% year-over-year revenue growth.

MELI Revenue (Quarterly YoY Growth) data by YCharts.

MercadoLibre's focus on Latin America gives it a longer growth runway compared to developed markets like the U.S., as e-commerce is still relatively underpenetrated in Latin America. The same is true for the digital payments and fintech businesses.

MercadoLibre is primarily focused on Brazil (which provides half of its revenue), Mexico, and Argentina. It continues to grow in those markets while expanding in secondary markets in Latin America, like Chile.

Management observed in its recent report that e-commerce penetration has the potential to double in the coming years. The company is rolling out new strategies to drive growth in that area, including expanding free shipping by lowering the minimum order size to qualify, and expanding its merchant base.

Amazon has made some noise in the region by acquiring a stake in Colombian delivery company Rappi in September, through a $25 million convertible note. MercadoLibre stock fell on reports that Amazon was aiming to make another push into the Brazilian market, in addition to competition from PDD Holdings' Temu and Sea Limited's Shopee.

However, MercadoLibre has faced competition before, including from all of the above providers. It has several competitive advantages that should help maintain its leadership status. One is a Prime-like membership program, Meli+, which offers fast shipping, access to streaming services, and a cash-back program at vendors like McDonald's and Petrobras when customers pay with a Mercado Pago credit card.

In other words, it will be hard for any competitor, even Amazon, to break MercadoLibre's grip on the Brazilian market.

Overall, MercadoLibre offers an excellent track record of growth, a long runway for expansion, and an impressive set of competitive advantages.

Investors are understandably jittery about the rapid expansion of MercadoLibre's credit business as its portfolio rose 83% to $11 billion in the third quarter. But management said its underwriting models have gotten more accurate. And its net interest margin after losses remains solid at 21%, though it was down year over year in part to higher funding costs in Argentina. First payment defaults in Brazil also reached an all-time low even as it issued a record number of credit cards in the country.

Long-term shareholders know that MercadoLibre has a history of pullbacks much like the current one. In fact, the stock has fallen 22% or more nine times before in its history before going on to set another all-time high. That should give investors confidence that the e-commerce stock can bounce back from this sell-off as well.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 24, 2025

Jeremy Bowman has positions in Amazon and MercadoLibre. The Motley Fool has positions in and recommends Amazon, MercadoLibre, and Sea Limited. The Motley Fool has a disclosure policy.

| Mar-31 | |

| Mar-31 | |

| Mar-25 | |

| Mar-17 | |

| Mar-16 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-10 | |

| Mar-08 | |

| Mar-08 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite