|

|

|

|

|||||

|

|

|

Over the last six months, McCormick’s shares have sunk to $65.43, producing a disappointing 10.8% loss - a stark contrast to the S&P 500’s 14.1% gain. This may have investors wondering how to approach the situation.

Is now the time to buy McCormick, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Even with the cheaper entry price, we're swiping left on McCormick for now. Here are three reasons why MKC doesn't excite us and a stock we'd rather own.

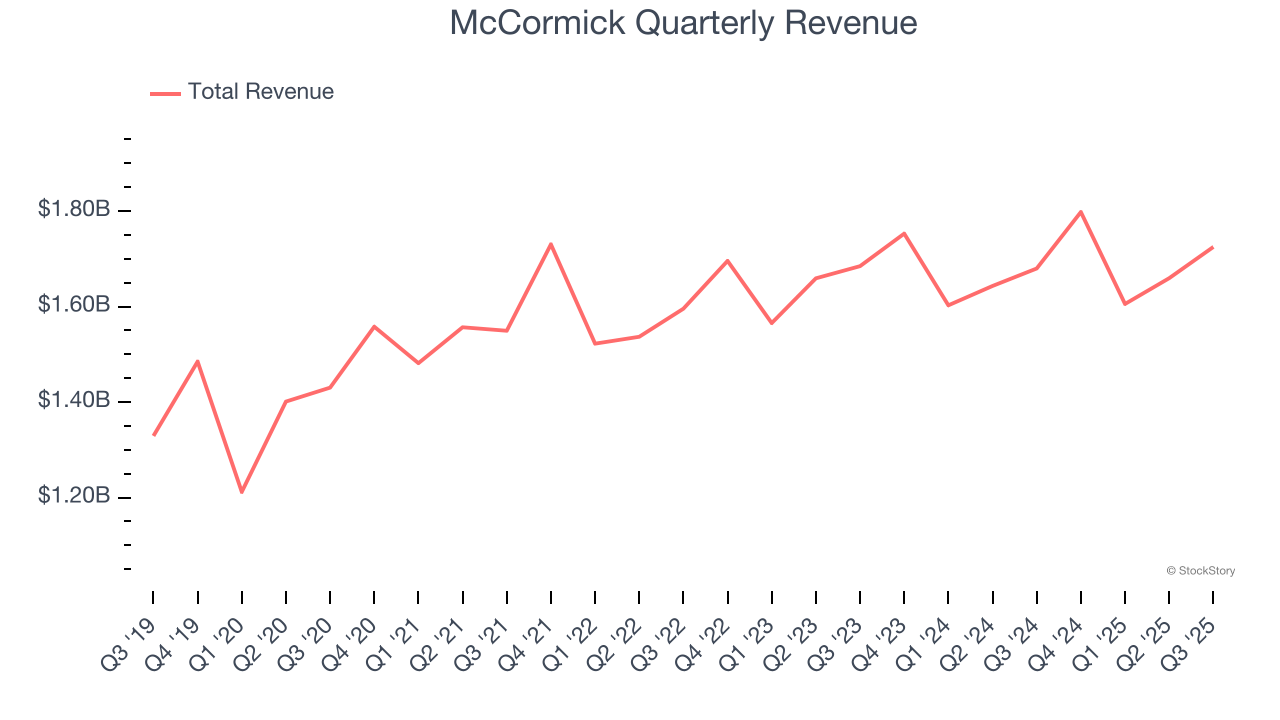

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, McCormick’s 2.1% annualized revenue growth over the last three years was sluggish. This was below our standards.

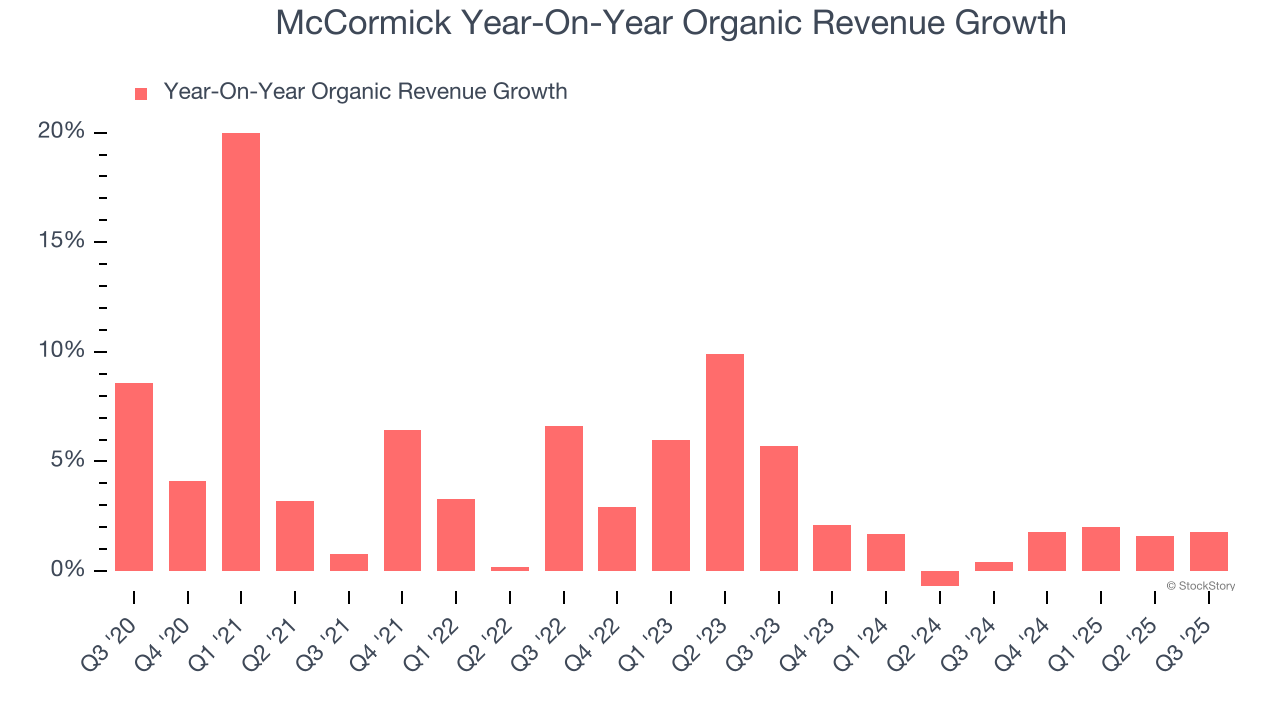

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for McCormick’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 1.3%.

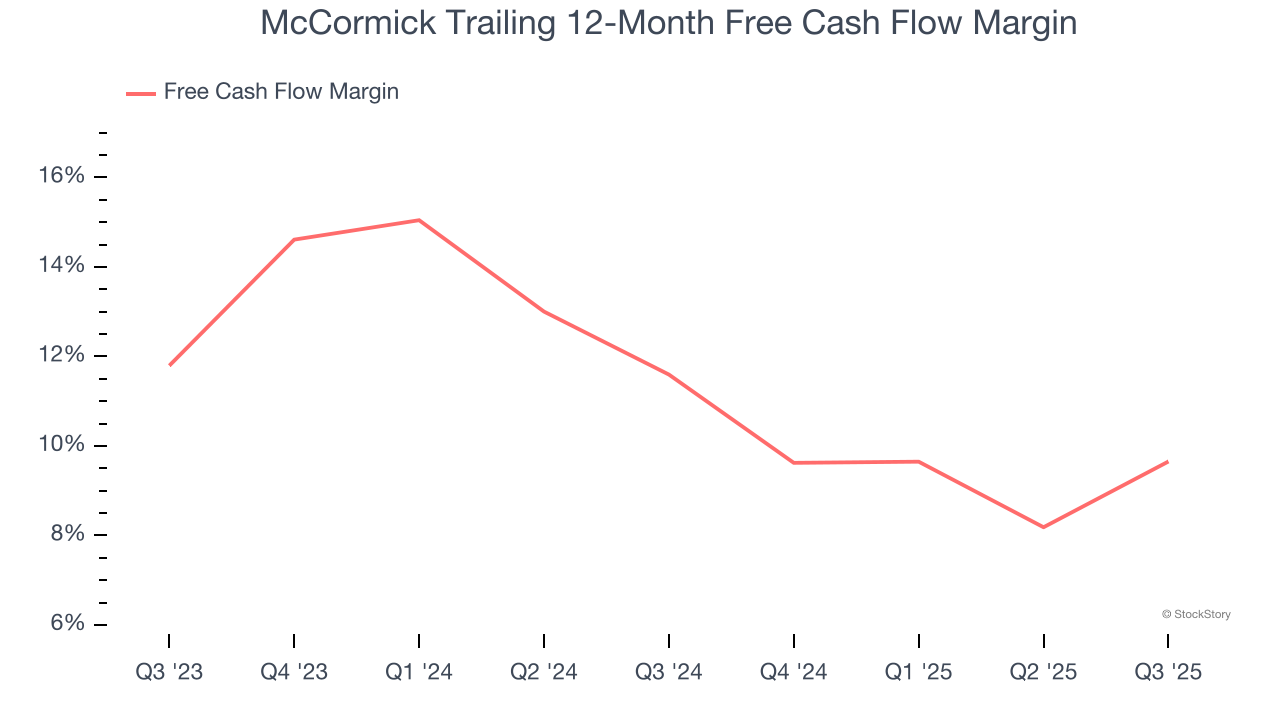

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, McCormick’s margin dropped by 1.9 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. McCormick’s free cash flow margin for the trailing 12 months was 9.7%.

McCormick isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 21.3× forward P/E (or $65.43 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at a top digital advertising platform riding the creator economy.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 11 hours | |

| 12 hours | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Spice Maker McCormick's Rise from a Baltimore Cellar to a Global Food Power

MKC -6.11%

The Wall Street Journal

|

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Stocks to Watch Tuesday: McCormick, Unilever, Marvell, Centessa, Apellis

MKC -6.11%

The Wall Street Journal

|

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite