|

|

|

|

|||||

|

|

|

Nvidia supplies the world's best data center chips for processing artificial intelligence (AI) workloads.

The company is experiencing more demand than it can possibly supply, which is fueling financial results.

The stock trades at an attractive valuation, which could set the stage for a price of $300 or more in 2026.

Nvidia's (NASDAQ: NVDA) graphics processing units (GPUs) for data centers are the gold standard for developing artificial intelligence (AI) models. Demand continues to exceed supply for these chips, as the world's largest tech giants battle for supremacy in the emerging AI industry.

By 2030, Nvidia CEO Jensen Huang estimates data center operators will be spending up to $4 trillion annually on infrastructure to meet demand from AI developers, and a sizable chunk of that money will go toward GPUs.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Nvidia stock has soared more than tenfold since the beginning of 2023, which is when the AI boom started gathering momentum, but it's still trading at a very attractive valuation. The stock is priced at $181 as I write this, but here's why I predict it will breeze past $300 in 2026.

Image source: Nvidia.

GPUs are designed for parallel processing, meaning they can handle multiple tasks simultaneously which makes them ideal for data-intensive AI workloads. Nvidia's GPU architectures (the latest of which is called Blackwell Ultra) are optimized specifically for AI, and it currently leads the industry in terms of performance.

Blackwell Ultra-based GB300 GPUs produce up to 50 times more processing power in certain configurations compared to Nvidia's original Hopper-based H100 chips from 2022, which highlights how far the company has come in just three years.

The H100 was perfect for one-shot large language models (LLMs) like OpenAI's GPT-3 and Alphabet's Gemini 1 from a few years ago, but each new generation of AI model requires more computing capacity. In fact, Nvidia CEO Jensen Huang says the latest reasoning models -- like GPT-5.1 and Gemini 3 -- consume up to 1,000 times more tokens (words and symbols), so even Blackwell Ultra GPUs aren't necessarily enough.

But Nvidia plans to take an enormous leap forward in 2026 by launching its new Rubin architecture. It's expected to be around 3.3 times more powerful than Blackwell Ultra, which implies a staggering 165 times performance increase over Hopper. Nvidia is already experiencing more demand than it can possibly supply for its current chips, and Rubin will probably accentuate that imbalance, giving the company incredible pricing power.

According to management's guidance, Nvidia is on track to generate a record $212 billion in total revenue during its current fiscal 2026 year (which ends on Jan. 31, 2026). Almost 90% of that revenue will come from the data center segment alone, which highlights the importance of GPU sales.

Wall Street's consensus estimate (provided by Yahoo! Finance) shows that Nvidia's revenue could soar by 48% to $313 billion in fiscal 2027 (which starts in February 2026). Analysts also predict the company's earnings could surge by 59% year over year to $7.46 per share, which could have an extremely positive impact on its stock. I'll discuss this further in a moment.

Nvidia has made a habit of beating its own forecasts and Wall Street's estimates over the last couple of years, because demand for its AI GPUs has consistently been far stronger than expected. With the Rubin architecture in the pipeline, that dynamic is unlikely to change over the next 12 months.

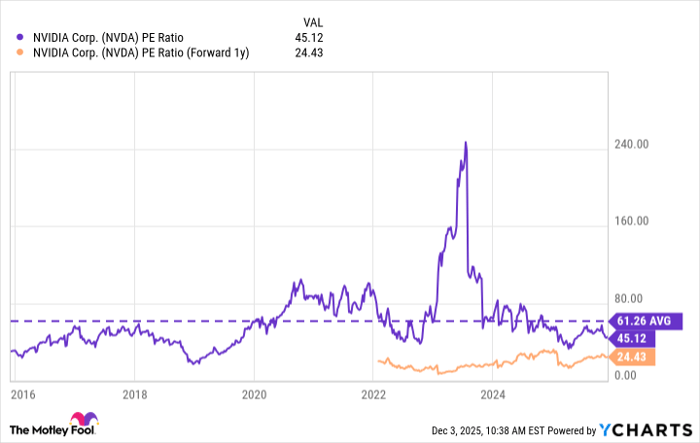

Based on Nvidia's adjusted (non-GAAP) trailing 12-month earnings of $4.05 per share, its stock is trading at a price-to-earnings (P/E) ratio of 45.1. That's a steep discount to its 10-year average of 61.2. If we use Wall Street's fiscal 2027 earnings estimate of $7.46 per share, that places Nvidia stock at an even more attractive forward P/E ratio of 24.4:

NVDA PE Ratio data by YCharts

That means Nvidia stock would have to climb by 84% next year just to maintain its current P/E ratio of 45.1, and it would have to soar by a whopping 151% to trade in line with its 10-year average P/E ratio of 61.2. That would place the stock at somewhere between $334 and $454.

That being said, there are no guarantees in the stock market, especially in industries that move as fast as AI. Nvidia is facing growing competition from other chip makers, and also from tech giants like Alphabet, which are now training their AI models using their own specially designed chips.

This won't be a near-term problem for Nvidia if Huang is right about AI infrastructure spending reaching $4 trillion annually by 2030, because it means demand for data center GPUs is likely to outstrip supply for the next several years.

However, Nvidia investors should keep a close eye on the competitive landscape in the new year, because if the company does experience declining demand, it could struggle to meet Wall Street's revenue and earnings estimates, negatively impacting its stock.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $540,587!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,118,210!*

Now, it’s worth noting Stock Advisor’s total average return is 991% — a market-crushing outperformance compared to 195% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of December 1, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool has a disclosure policy.

| 44 min | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite