|

|

|

|

|||||

|

|

|

Not all of the market’s current mega-cap stocks have logged the same degree of gains of late.

Even some of the "Magnificent Seven" stocks have lagged their peers.

Two of these underestimated laggards are now positioned to dish out the strong performance they haven’t been delivering.

It's no secret that a handful of technology stocks have overperformed the overall market for a while now. This small group of tickers has even been given a flattering name to reflect this performance: the "Magnificent Seven." Led by Nvidia and Apple, with a strong showing from Alphabet, Magnificent Seven stocks gained an average of nearly 700% between 2015 and the end of 2024, with even more gains being tacked on in 2025. That's huge.

And yet, as much as these stocks have collectively rallied -- and as overvalued as some of them arguably are now -- a couple of them still have room and reason to continue climbing, perhaps even outperforming the other five. Here's a closer look.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Many investors may be surprised to learn that Facebook parent Meta Platforms (NASDAQ: META) is the second-worst-performing Magnificent Seven name for the 10-year stretch in question, right ahead of Tesla. Given a little thought, though, it actually makes sense. The market's been waiting for consumers to grow weary of social media's typical toxicity, and has been pricing this headwind in.

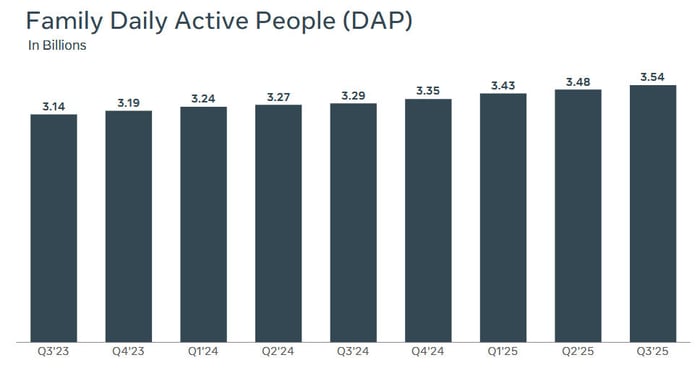

It never happened, though. The number of people utilizing at least one of Meta's platforms (Facebook, Instagram, WhatsApp, and Messenger) every single day continues to grow, reaching a record of 3.54 billion per day during the third quarter of this year.

Image source: Meta Platforms' Q3-2025 earnings presentation.

This isn't unproductive user growth, either. They're seeing and clicking on advertisements as much as any of the company's platforms' users ever have. Meta's average revenue per user (or ARPU) reached a record of $14.46 in Q3, up nearly 18% year over year. It may be spending more money than it ever has. But the company's getting a great return on its investment -- its profit margin rates aren't really any different for the company now than they've been in its past.

Give credit to artificial intelligence, mostly. Meta isn't just offering AI tools to its apps' users. It's using artificial intelligence to improve its own products and services. For instance, its AI-powered content-recommendation technology prompted users to spend 5% more time on Facebook last quarter, and 10% more time on Threads.

This is still just the beginning. As CEO Mark Zuckerberg explained during the Q3 earnings conference call, the company is already preparing for so-called superintelligence that will fine-tune its platforms' revenue-bearing content recommendations. It's also looking forward to more and better tools for businesses that want to engage with consumers through Meta's messaging apps.

The thing is, platforms like Facebook and WhatsApp are already ideally suited to make business-oriented use of such a tool. Its users are already highly engaged. Adding business-building forms of engagement wouldn't be a big leap for brands.

Analysts are optimistic anyway. Despite the stock's relatively weaker performance, the vast majority of the analyst community still considers Meta stock a strong buy, with a consensus price target of $838.79 that is 25% above the ticker's present price.

The other Magnificent Seven name still worth stepping into here is Amazon (NASDAQ: AMZN), although not necessarily just for the reason you might think.

No discussion of the e-commerce giant can ignore the fact that its cloud computing arm -- Amazon Web Services -- is this company's big moneymaker even if it's not its biggest business. Although AWS only accounts for 18% of the organization's revenue, it produces 60% of its operating income. And given Mordor Intelligence's prediction that the ongoing proliferation of AI is going to spur average annual growth of 21% for the global cloud computing industry through 2030, AWS's overall net impact on this company's bottom line is set to grow as well, by a lot.

There's also a less-seen, underappreciated dynamic in place here that's bolstering Amazon's long-term growth prospects. That's a rethinking of what its online shopping platform is, and how all the web traffic it generates can be monetized. While Amazon.com and all of its overseas variations are still selling merchandise (the company's own inventory, as well as third-party sellers' goods), it's having tremendous success as an advertising medium. Over the course of the past four reported quarters, Amazon has collected more than $64 billion worth of high-margin ad revenue from its sellers looking to feature their goods at the shopping website. That's more than its entire online shopping arm produces in operating income in a single year.

There's more where that came from, too. An outlook from Forrester Research suggests the worldwide retail media market is poised to grow from $184 billion this year to $312 billion per year by 2030.

Amazon stock hasn't been a poor performer of late, to be clear. But it's undeniably underperformed its peers since early this year, mostly due to tariff-related concerns and worries about broad economic malaise. We can now see those concerns weren't quite the problem they were expected to become, but the stock hasn't fully shrugged it off yet. That translates into a buying opportunity for interested investors.

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $540,587!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,118,210!*

Now, it’s worth noting Stock Advisor’s total average return is 991% — a market-crushing outperformance compared to 195% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of December 8, 2025

James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Nvidia, and Tesla. The Motley Fool has a disclosure policy.

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite