|

|

|

|

|||||

|

|

|

McDonald's Corporation MCD is betting big that a comprehensive value reset, centered on revamped Extra Value Meals (EVMs) and a more disciplined national value architecture, can help reverse two years of declining traffic among lower-income U.S. consumers. The company’s latest earnings call revealed a clear strategic theme: value must become both predictable and compelling if it hopes to rebuild guest counts in 2026.

The relaunch of EVMs, featuring nationally advertised $5 and $8 meal price points, marks the most significant effort to repair value perception on the core menu. Leadership acknowledged that EVM pricing had drifted away from what consumers expected, creating a drag on value scores. Franchisees overwhelmingly agreed that change was necessary and McDonald’s is co-investing through early 2026 to ease the near-term margin pressure as traffic rebuilds.

Early results are promising, with improving value scores and growing awareness, but management maintains that momentum will take several quarters to fully materialize. The broader challenge remains macro-driven: rents, food inflation and childcare costs continue to squeeze lower-income consumers, keeping QSR visits in double-digit decline. Until real income pressure eases, recovery in that segment will be slow, even with aggressive value.

Still, McDonald’s enters 2026 better positioned. Stronger value signaling, digital engagement through loyalty and MONOPOLY, and menu innovations like Snack Wraps are supporting higher-income traffic gains while reinforcing brand relevance across cohorts. If inflation moderates and value messaging scales as planned, McDonald’s could see guest counts stabilize, and potentially increase upward during 2026.

The company is not forecasting a quick turnaround, but its disciplined value reset lays the foundation for traffic-led growth when the consumer finally regains footing.

Two major competitors, The Wendy's Company WEN and Restaurant Brands International Inc.’s QSR Burger King, are also tightening their value strategies as the QSR landscape prepares for another year of strained consumer spending in 2026.

Wendy’s continues to lean heavily on its well-known 4 for $4 and Biggie Bag bundles, giving guests clear price certainty and helping the brand stay relevant among value-driven consumers. Its digital ecosystem, boosted by personalized deals, is designed to reinforce frequency much like McDonald’s loyalty-led approach.

Burger King, under parent company Restaurant Brands International, is pushing value as a core pillar of its “Reclaim the Flame” turnaround plan. National offers, sharper bundle pricing and operational improvements are aimed at winning back traffic lost over the past few years.

While both WEN and QSR are stepping up their value playbooks, neither has McDonald’s scale or financial flexibility, making 2026 a competitive proving ground for who executes value most effectively.

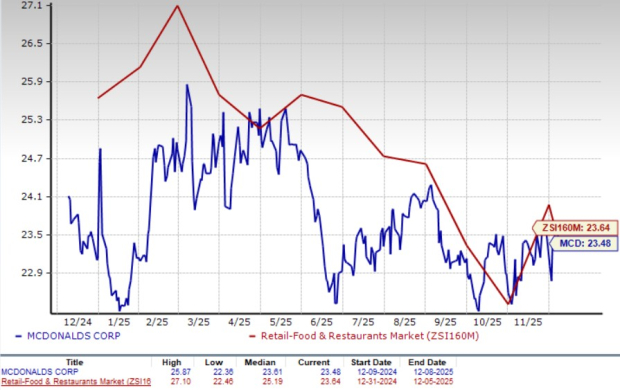

McDonald’s shares have gained 3% in the past year against the industry’s 12.5% decline.

In terms of its forward 12-month price-to-earnings ratio, MCD is trading at 23.48, down from the industry’s 23.64.

Over the past 30 days, the Zacks Consensus Estimate for MCD’s 2025 earnings per share has decreased, as shown in the chart.

MCD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite