|

|

|

|

|||||

|

|

|

Strategy Inc. MSTR is widely known today for its aggressive Bitcoin strategy, but the company's long-term fundamentals are centered on its software and enterprise analytics businesses. Within this segment, subscription services are emerging as the most critical driver of stability and future growth.

However, growth across the software business remains uneven. Declines in product support and other services partially offset subscription gains, indicating that parts of the legacy software portfolio are still under pressure. As a result, while subscriptions are clearly gaining traction, they have not yet transformed the software segment into a major growth engine.

Despite these challenges, the software business continues to deliver strong profitability, with healthy margins supporting profitability. This makes subscription services an important stabilizing force within Strategy’s broader business model, particularly given the volatility associated with Bitcoin-driven earnings.

In the third quarter of 2025, subscription services revenues surged 65.4% year over year to $46.0 million, accounting for roughly 36% of total revenues. This rapid expansion reflects the growing adoption of Strategy’s cloud-based analytics offerings. This shift toward subscriptions is strategically important, as recurring revenues provide greater visibility and stability than one-time license sales.

Looking ahead, the Zacks Consensus Estimate projects modest revenue growth of about 2.1% in 2025 and 4.9% in 2026, suggesting that steady and sustainable expansion in subscription services could gradually enhance the software segment’s contribution to consistent, long-term growth.

Microsoft MSFT and Salesforce CRM offer different types of software, but both rely on strong subscription-based platforms that provide steady recurring revenue through cloud, analytics and enterprise services.

Microsoft’s Power BI remains one of the most serious competitive threats to MicroStrategy, offering an intuitive interface, drag-and-drop analytics and seamless integration across Microsoft 365, Azure, Excel and Dynamics. The company’s free desktop tier and low-cost Pro licenses make it especially attractive for SMBs modernizing analytics. Backed by Microsoft’s vast cloud, productivity and enterprise software ecosystem, Power BI benefits from the company’s diversified performance and deeply integrated SaaS and consumption-based models.

Salesforce competes with MicroStrategy by unifying analytics, CRM and customer-centric workflows through its Tableau-powered ecosystem. It delivers rich, intuitive dashboards that simplify data exploration for business users. Salesforce also excels in managing customer journeys, sales pipelines and service operations, leveraging its CRM foundation to strengthen relationships, boost sales and enhance retention.

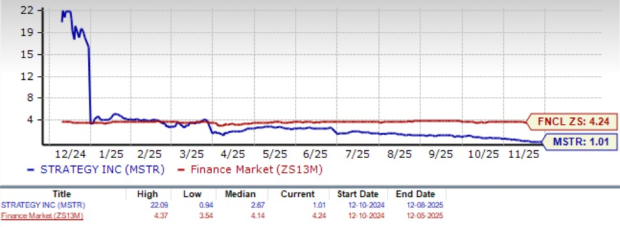

Shares of Strategy have plunged 49.7% in the past year, sharply underperforming the Zacks Finance sector’s 11.7% gain. MSTR also lagged key competitors; Microsoft rose 10.1%, while Salesforce declined 26.1%.

MSTR has a Value Score of F. It is currently trading at a Price/Book ratio of 1.01X compared to the sector’s 4.24X.

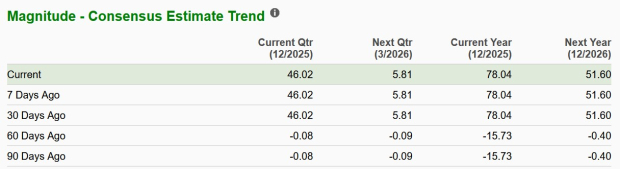

The Zacks Consensus Estimate for MSTR’s 2025 earnings is pegged at $78.04 per share, unchanged over the past 30 days. The estimate also indicates a strong year-over-year recovery from a loss of $6.72 per share.

MSTR stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite