|

|

|

|

|||||

|

|

|

Tempus AI TEM is transitioning from a heavy-investment growth stage toward improved operating leverage and a more scalable mix of revenue. This is possible as the company integrates genomics, multimodal real-world data and clinical AI into a unified system.

Rivals of Tempus like Hims & Hers Health HIMS and Veeva Systems VEEV are also demonstrating strong performance and strategic growth moves.

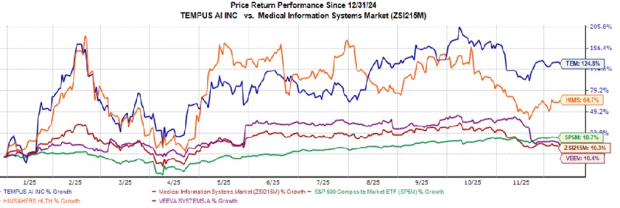

Year to date, TEM stock has climbed 124.8%, surpassing the broader industry’s 10.3% gain. The S&P 500 benchmark index has gained 10.7% during this period. The company has also outperformed other players in the health infotech field, including HIMS, which rose 64.7%, and VEEV, which gained 10.4% during the same period.

Expanding Genomics Testing Base: Tempus saw strong year-over-year revenues and test-volume growth in its Genomics segment throughout 2025. Management highlighted that the growth was broad-based, covering solid tumor testing, liquid biopsy and pediatrics and rare disease assays. Ambry genetics, the hereditary business, also played a major role by adding meaningful hereditary test-volume growth and helping TEM gain market share. These rising test volumes drove near-term top-line growth and continually expanded the company’s proprietary clinical and molecular dataset.

High-margin Data & Services (Insights): Over the first three quarters of 2025, the Data & Services business has emerged as a high-margin and scalable revenue stream beyond traditional genomic testing, driven primarily by the expansion of its Insights data-licensing business. Each quarter delivered solid gains with Insights repeatedly outpacing the broader segment. Tempus expanded its collaboration with Northwestern Medicine to integrate David, Tempus’ generative AI clinical co-pilot, into the EHR platform to streamline and transform clinical workflows.

Tempus Next also expanded into breast cancer, offering real-time insights to help clinicians close guideline-based care gaps, underscoring continued innovation across the Data and Services segment.

Expanding Beyond Oncology: Tempus is building and deploying anticritical intelligence (AI) algorithms and diagnostic software that run on its multimodal data. These algorithms span beyond oncology, including digital pathology, radiology, cardiology, and neuropsych. In line with this, it began a collaboration with Northwestern University’s Abrams Center to use its Lens platform for accelerating Alzheimer’s research.

Also, the company secured two FDA 510(k) clearances — one for the updated Tempus Pixel cardiac imaging platform and another for its ECG-Low EF software, which uses AI to help identify patients with potentially low ejection fraction. Additionally, Tempus acquired Paige to grow its dataset and establish a strong footprint in digital pathology through an industry-leading technology portfolio.

Competitive Advantage: Tempus strengthened its competitive position by entering multi-year strategic collaborations with AstraZeneca and Pathos to build the world’s largest multimodal foundation model in oncology. Through this, Tempus gets access to more than 300 petabytes of multimodal, outcome-linked data to train large-scale models.

This dataset, spanning molecular, clinical, imaging and pathology information, gives it a significant advantage. It also makes Tempus a more valuable partner for pharmaceutical companies and health systems that rely on comprehensive, high-quality datasets for research, development, and clinical decision support.

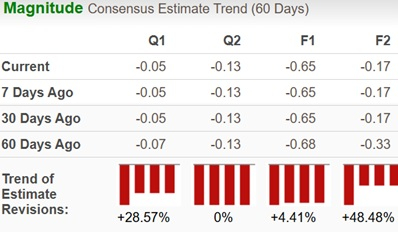

For full-year 2025, Tempus is expected to generate revenue growth of 82.2%. On the profitability front, earnings per share are expected to remain negative, but improve 58.9% year over year. Over the past 30 days, Tempus’ loss per share estimate for 2025 has remained unchanged at 65 cents.

Image Source: Zacks Investment Research

Reimbursement Issue: Although Tempus has developed and published several advanced AI-driven diagnostic algorithms, the absence of reimbursement frameworks for such tools within the U.S. healthcare system poses a significant structural hurdle. Due to this, the company’s AI business looks promising but unlikely to generate large revenues in the near term until payers adopt consistent reimbursement policies.

At the same time, Tempus’ average reimbursement was approximately $1,600 per test in the third quarter, well below parity with peers. Management believes that continued FDA approvals and the shift of tests into ADLT status should help improve reimbursement over time.

Tempus stock is not so cheap, as suggested by the Value Score of F.

TEM is currently trading at a 12-month forward price-to-sales (P/S) of 8.76X, which is higher than the industry average of 5.77X.

Image Source: Zacks Investment Research

Tempus AI is entering a pivotal phase in its evolution, driven by growing test volumes, high-margin data services and expanding clinical AI capabilities. While reimbursement remains a key hurdle, its deep multimodal dataset and strategic partnerships position the company well to capitalize on long-term opportunities in precision medicine.

With TEM shares already trading at elevated levels, we advise those who already have this Zacks Rank #3 (Hold) stock in their portfolios to maintain their position, while others may wait for a more favorable entry point. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 47 min | |

| 48 min | |

| 1 hour | |

| 1 hour | |

| 7 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Hims Topples As Obesity Kingpin Hits A Snag On Weighty Second-Quarter Loss

HIMS HIMS -6.55%

Investor's Business Daily

|

| Aug-10 | |

| Aug-10 |

Hims & Hers Health Boosts Revenue Target, Swings to Second-Quarter Loss

HIMS HIMS -6.55%

The Wall Street Journal

|

| Aug-10 | |

| Aug-10 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite